Stratégie de trading de suivi de tendance et de retournement basée sur de multiples niveaux d'équilibre des prix

Aperçu de la stratégie

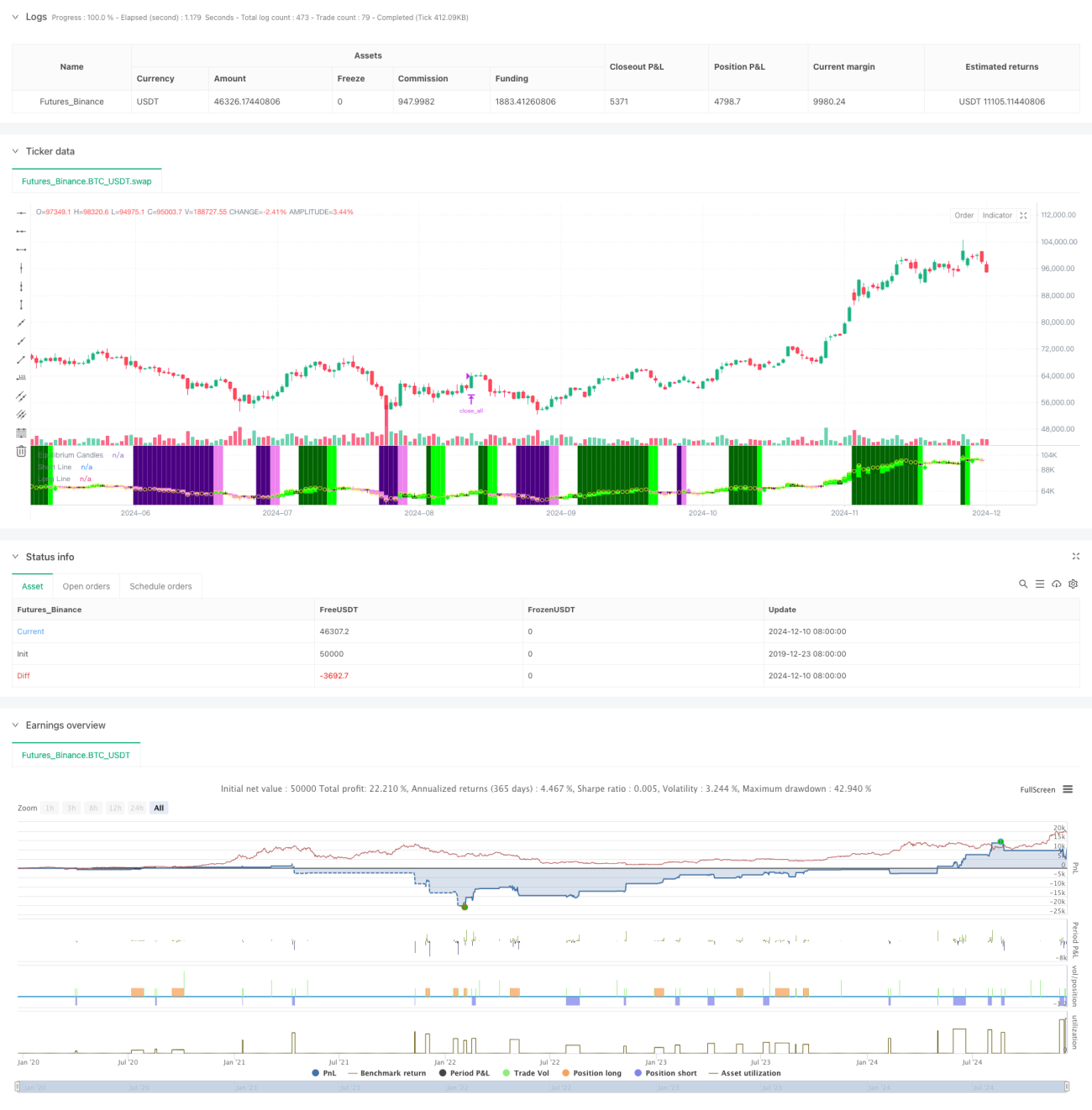

Cette stratégie est un système de trading basé sur le suivi de tendance et le retournement, utilisant un point d'équilibre des prix. Elle calcule le prix d'équilibre comme la moyenne du plus haut et du plus bas des X dernières bougies, puis détermine la direction de la tendance en fonction de la position du prix de clôture par rapport à ce prix d'équilibre. Lorsque le prix reste continuellement d'un côté de l'équilibre pendant un nombre défini de bougies, le système considère la tendance comme établie. Au premier repli (franchissement du prix d'équilibre), il cherche une opportunité d'entrée. La stratégie peut être configurée en mode suivi de tendance ou trading de retournement.

Principe de la stratégie

- Calcul du prix d'équilibre : il s'agit du point médian entre le plus haut et le plus bas des X dernières bougies, identique à la méthode de calcul de la ligne de base Ichimoku.

- Identification de tendance : lorsque le prix reste du même côté du prix d'équilibre pendant X bougies consécutives (7 par défaut), la tendance est considérée comme établie.

- Signal d'entrée : le premier repli après l'établissement de la tendance (le prix franchissant le prix d'équilibre) déclenche le signal d'entrée.

- Stop loss et take profit : utilisation du quantile à 60 % de l'ATR pour ajuster dynamiquement les distances de stop loss et de take profit, offrant une flexibilité dans la gestion des risques.

- Protection contre les mouvements violents : lorsque le prix s'écarte du prix d'équilibre au-delà d'un multiple d'ATR défini, le système ferme automatiquement la position pour éviter un drawdown important.

Avantages de la stratégie

- Adaptabilité : possibilité de basculer entre le suivi de tendance et le trading de retournement en fonction des caractéristiques du marché.

- Gestion des risques complète : stop loss dynamique basé sur l'ATR et mécanisme de protection contre les mouvements violents.

- Signaux clairs : les signaux de trading sont nets, sans dépendre d'une combinaison complexe d'indicateurs techniques.

- Bonne visualisation : utilisation de bougies colorées et d'un fond d'écran pour une représentation intuitive de l'état du marché.

- Compatible avec l'automatisation : peut être facilement intégré à des plateformes de trading comme MT5 pour une exécution automatisée.

Risques de la stratégie

- Risque en marché rangeant : peut générer de fréquents faux signaux en phase de consolidation.

- Impact du slippage : en cas de forte volatilité, le slippage peut être important.

- Sensibilité aux paramètres : les paramètres clés (période d'équilibre, cycle de détection de tendance) doivent être soigneusement optimisés pour chaque marché.

- Risque de transition de marché : la période de transition entre marché en tendance et marché rangeant peut entraîner un drawdown important.

Directions d'optimisation

- Identification de l'environnement de marché : ajouter un module pour détecter les conditions de marché et ajuster dynamiquement les paramètres de la stratégie.

- Filtrage des signaux : envisager d'ajouter des indicateurs auxiliaires comme le volume ou la volatilité pour filtrer les faux signaux.

- Gestion de la taille des positions : intégrer des mécanismes plus sophistiqués, comme un ajustement dynamique basé sur la volatilité.

- Multiples périodes de temps : combiner les signaux de plusieurs horizons temporels pour améliorer la précision des trades.

- Optimisation des coûts de transaction : ajuster le timing d'entrée et de sortie en fonction des caractéristiques de coût des différents instruments.

Résumé

Il s'agit d'un système de trading de tendance bien conçu, offrant une logique claire basée sur le concept de prix d'équilibre. Son principal atout réside dans sa flexibilité : il peut être utilisé à la fois pour le suivi de tendance et le trading de retournement, tout en intégrant un mécanisme de gestion des risques complet. Bien qu'il puisse rencontrer des difficultés dans certaines conditions de marché, avec une optimisation continue et des ajustements judicieux, cette stratégie est susceptible de maintenir des performances stables dans divers environnements de marché.

- 1