Stratégie avancée de suivi de tendance et de stop suivi adaptatif

Aperçu

Il s'agit d'une stratégie de suivi de tendance basée sur l'indicateur Supertrend, combinée à un mécanisme de stop suivi adaptatif. La stratégie identifie principalement la direction de la tendance du marché à l'aide de l'indicateur Supertrend, et utilise un stop suivi dynamique pour gérer les risques et optimiser le moment de sortie. La stratégie prend en charge plusieurs types de stops, notamment le stop en pourcentage, le stop basé sur l'ATR et le stop à points fixes, offrant une flexibilité d'adaptation aux différentes conditions de marché.

Principe de la stratégie

La logique centrale de la stratégie repose sur les éléments clés suivants :

- Utilisation de l'indicateur Supertrend comme principal outil d'identification de tendance, combiné à l'ATR (Average True Range) pour mesurer la volatilité du marché.

- Les signaux d'entrée sont déclenchés par un changement de direction du Supertrend, prenant en charge les positions longues, courtes ou les deux.

- Le mécanisme de stop loss utilise un stop suivi adaptatif qui ajuste automatiquement le niveau de stop en fonction de la volatilité du marché.

- Le système de gestion des transactions comprend la gestion de la taille des positions (par défaut 15 % du compte) et un mécanisme de filtrage temporel.

Avantages de la stratégie

- Forte capacité de capture de tendance : L'indicateur Supertrend permet d'identifier efficacement les tendances principales, réduisant les erreurs de jugement.

- Contrôle des risques complet : Utilisation de divers mécanismes de stop loss adaptés à différentes conditions de marché.

- Grande flexibilité : Prise en charge de plusieurs directions de trading et configurations de stop loss.

- Forte adaptabilité : Le stop suivi s'ajuste automatiquement en fonction de la volatilité du marché, améliorant la capacité d'adaptation de la stratégie.

- Système de backtest complet : Fonctionnalité de filtrage temporel intégrée pour faciliter l'analyse des performances historiques.

Risques de la stratégie

- Risque de retournement de tendance : Des signaux erronés peuvent apparaître sur les marchés très volatils.

- Risque de glissement : L'exécution du stop suivi peut être affectée par la liquidité du marché.

- Sensibilité aux paramètres : Les réglages des facteurs du Supertrend et de la période ATR ont un impact significatif sur les performances de la stratégie.

- Dépendance aux conditions de marché : Sur les marchés sans tendance, des transactions fréquentes peuvent entraîner une augmentation des coûts.

Pistes d'optimisation

- Optimisation du filtrage des signaux : Ajout d'indicateurs techniques supplémentaires pour filtrer les faux signaux.

- Optimisation de la gestion des positions : Ajustement dynamique de la taille des positions en fonction de la volatilité du marché.

- Renforcement du mécanisme de stop loss : Conception de logiques de stop plus complexes combinées au prix de revient moyen.

- Optimisation du moment d'entrée : Ajout d'analyses de structure de prix pour améliorer la précision des entrées.

- Amélioration du système de backtest : Ajout de davantage de métriques statistiques pour évaluer les performances de la stratégie.

Résumé

Il s'agit d'une stratégie de suivi de tendance bien conçue et à risque contrôlé. En combinant l'indicateur Supertrend avec un mécanisme de stop loss flexible, la stratégie permet de maintenir une rentabilité élevée tout en contrôlant efficacement les risques. Très configurable, elle convient à différents environnements de marché, mais nécessite une optimisation approfondie des paramètres et une validation par backtest. À l'avenir, l'ajout d'outils d'analyse technique supplémentaires et de mesures de contrôle des risques pourrait encore améliorer la stabilité et la rentabilité de la stratégie.

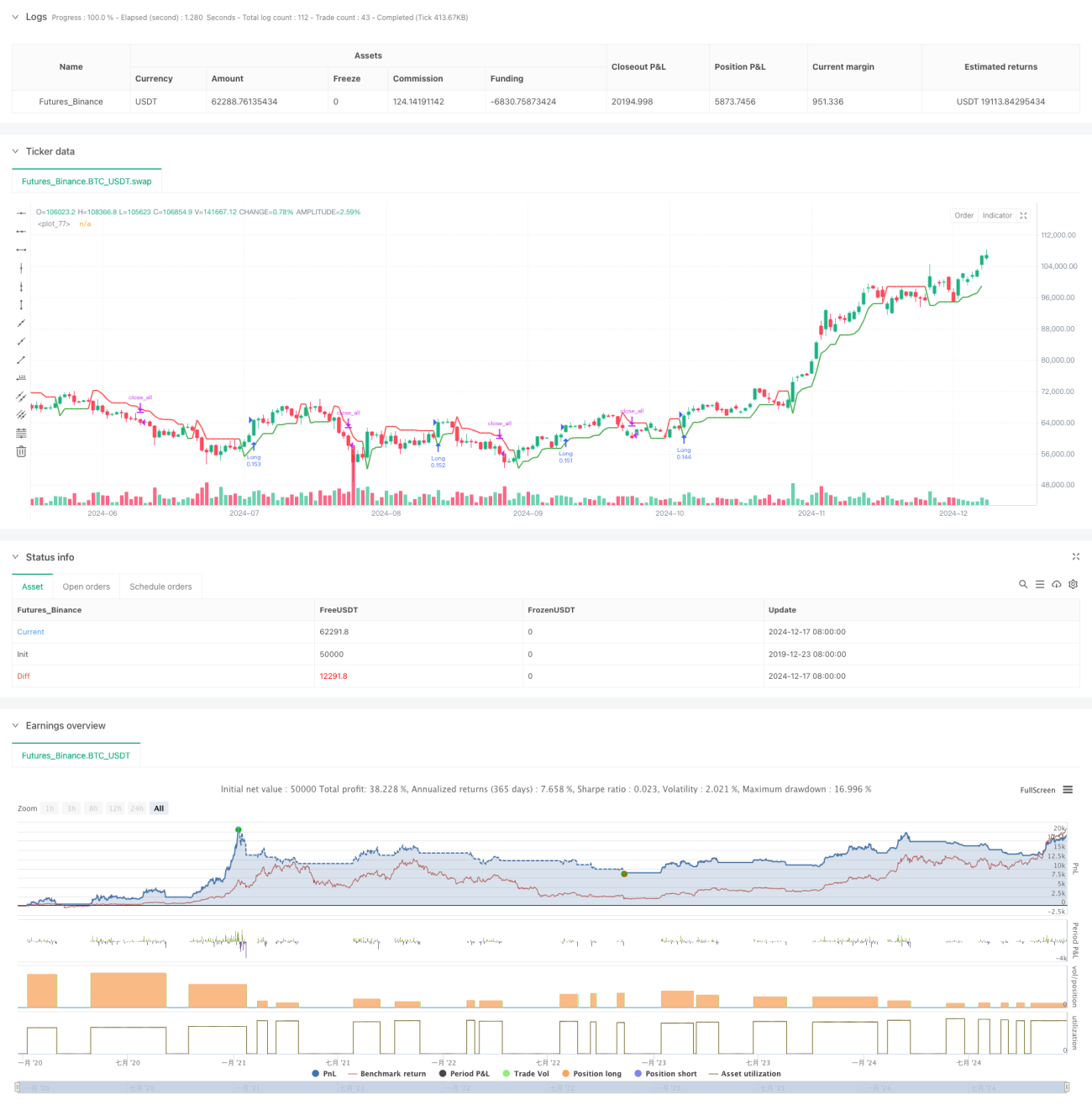

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("Supertrend Strategy with Adjustable Trailing Stop [Bips]", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=15)

// Inputs- 1