Système de trading de tendance combinant le croisement de multiples moyennes mobiles avec les supports et résistances Camarilla

Aperçu

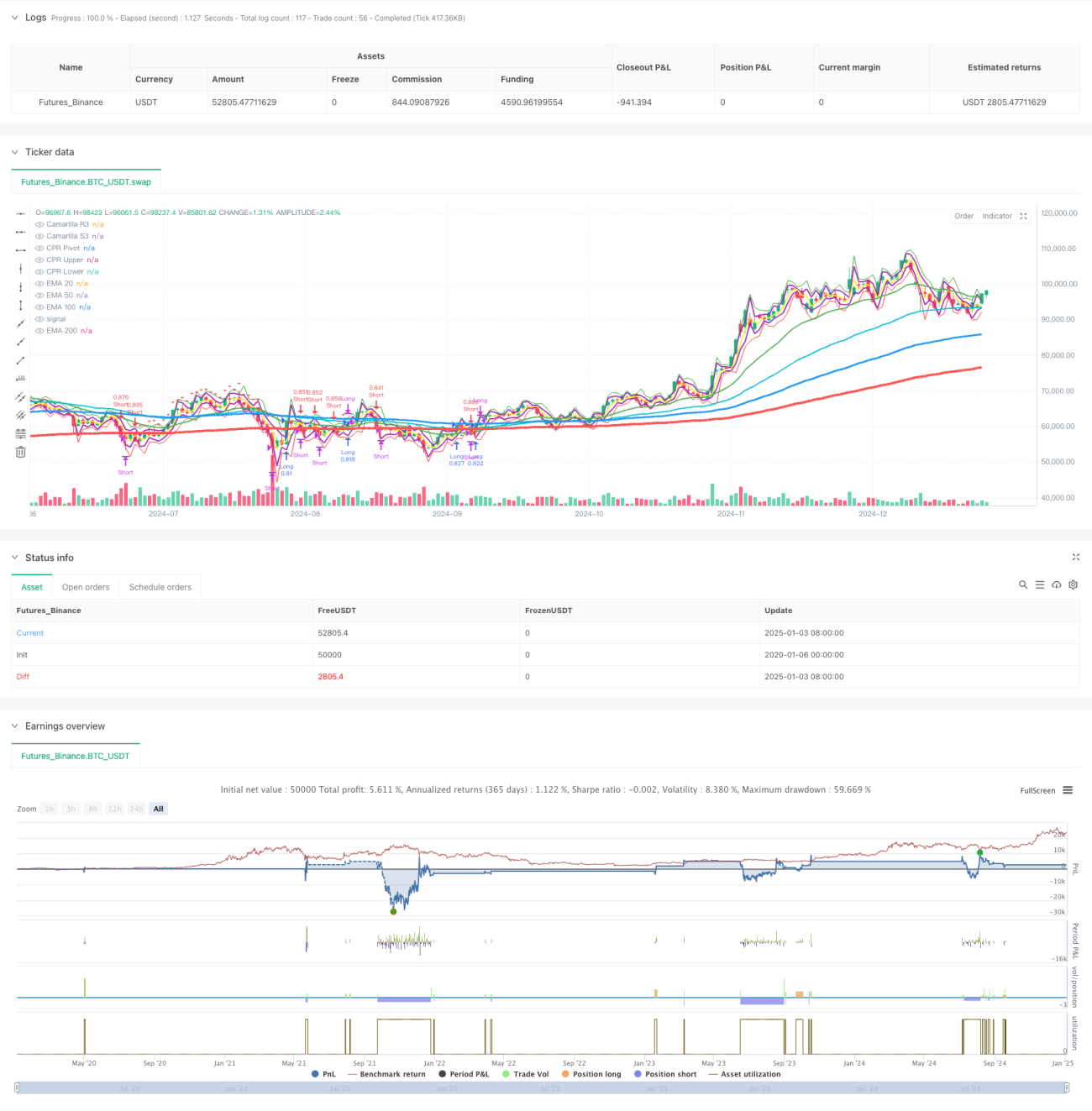

Cette stratégie est un système de trading de suivi de tendance qui combine plusieurs moyennes mobiles exponentielles (EMA), les niveaux de support et résistance Camarilla, et la plage pivot (CPR). Le système identifie les tendances du marché et les opportunités de trading potentielles en analysant la relation entre le prix et plusieurs moyennes mobiles ainsi que des zones de prix importantes. La stratégie applique une gestion stricte du capital et des mesures de contrôle des risques, notamment une taille de position en pourcentage et des mécanismes de sortie diversifiés.

Principe de la stratégie

La stratégie repose principalement sur les composants clés suivants :

- Un système multi-moyennes mobiles (EMA20/50/100/200) pour confirmer la direction et la force de la tendance.

- Les niveaux de support et résistance Camarilla (R3/S3) pour identifier les niveaux de prix clés.

- La plage pivot (CPR) pour déterminer la zone de trading intraday.

- Les signaux d'entrée sont basés sur le croisement du prix avec l'EMA200 et la confirmation de l'EMA20.

- La stratégie de sortie comprend deux modes : points fixes et déplacement en pourcentage.

- Le système de gestion du capital ajuste dynamiquement la taille de la position en fonction de la taille du compte.

Avantages de la stratégie

- La combinaison d'indicateurs techniques multidimensionnels fournit des signaux de trading plus fiables.

- Des mécanismes de sortie flexibles s'adaptent à différents environnements de marché.

- Un système de gestion du capital complet contrôle efficacement le risque.

- Les caractéristiques de suivi de tendance aident à capturer les grandes fluctuations.

- Les composants visuels facilitent la compréhension de la structure du marché par le trader.

Risques de la stratégie

- Des signaux erronés peuvent se produire dans un marché oscillant.

- De multiples indicateurs peuvent entraîner un retard des signaux de trading.

- Des niveaux de sortie fixes peuvent être sous-performants dans des marchés à forte volatilité.

- Un capital important est nécessaire pour supporter les drawdowns.

- Les coûts de transaction peuvent affecter le rendement global de la stratégie.

Axes d'optimisation de la stratégie

- Introduire un indicateur de volatilité pour ajuster dynamiquement les paramètres d'entrée et de sortie.

- Ajouter un module de reconnaissance de l'état du marché pour s'adapter à différents environnements.

- Optimiser le système de gestion du capital en intégrant une gestion dynamique de la position.

- Ajouter un filtre temporel des transactions pour améliorer la qualité des signaux.

- Envisager d'intégrer l'analyse des volumes pour renforcer la fiabilité des signaux.

Résumé

Cette stratégie construit un système de trading complet en intégrant plusieurs outils d'analyse technique classiques. L'avantage du système réside dans l'analyse multidimensionnelle du marché et une gestion stricte des risques, mais il est également nécessaire de prêter attention à son adaptabilité aux différents environnements de marché. Grâce à une optimisation et une amélioration continues, la stratégie devrait améliorer sa rentabilité tout en maintenant sa stabilité.

- 1