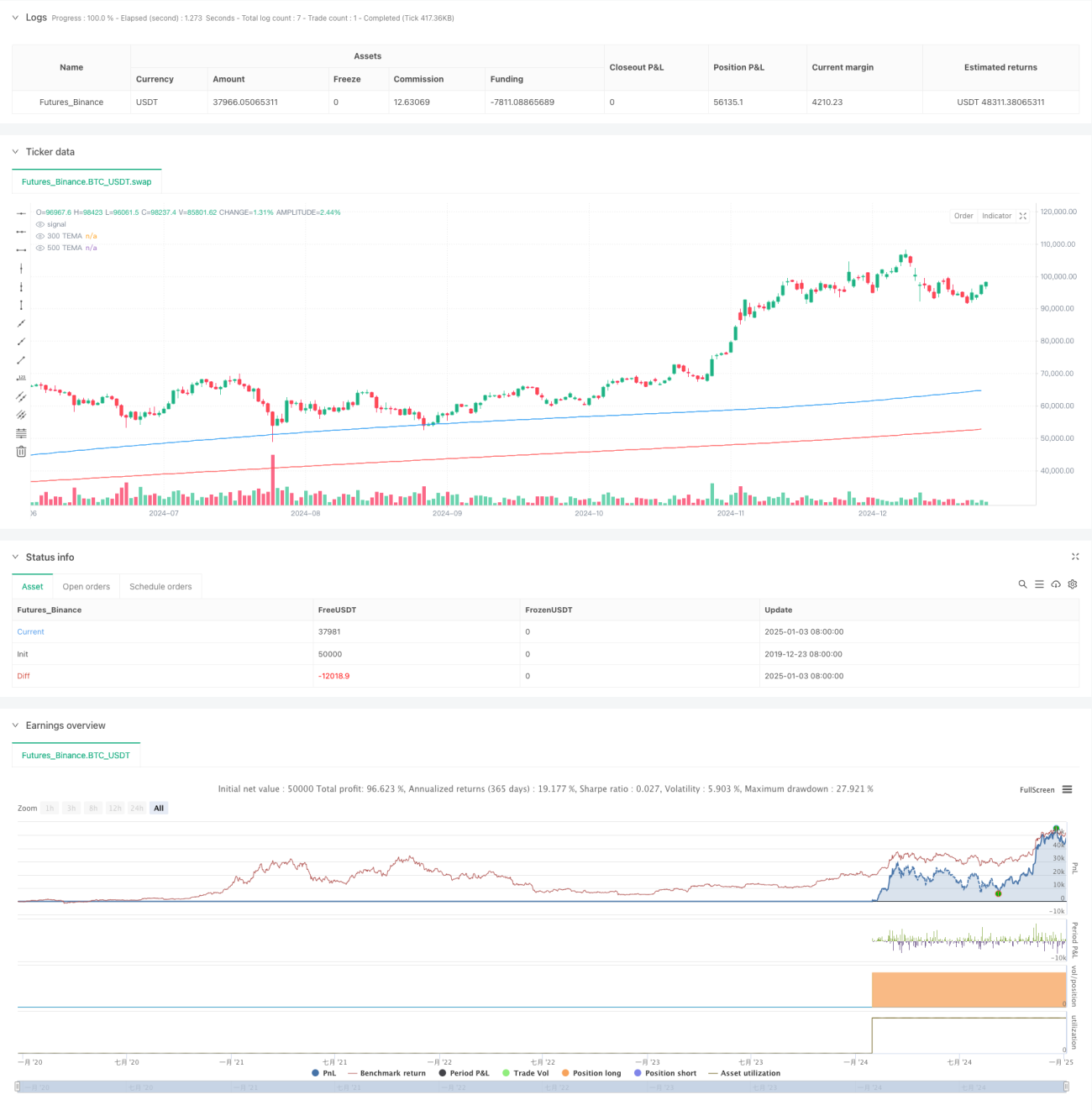

Aperçu

Cette stratégie est un système de trading de suivi de tendance basé sur la moyenne mobile exponentielle triple (TEMA). Elle capture les tendances du marché en comparant les signaux de croisement entre une TEMA courte et une TEMA longue, et gère le risque à l’aide d’un stop-loss basé sur la volatilité. La stratégie s’exécute sur une période de 5 minutes et utilise les indicateurs TEMA sur 300 et 500 périodes pour générer les signaux.

Principe de la stratégie

La logique centrale de la stratégie repose sur les éléments clés suivants :

- Utiliser deux TEMA de périodes différentes (300 et 500) pour identifier la direction de la tendance.

- Lorsque la TEMA courte croise la TEMA longue à la hausse, le système génère un signal d’achat.

- Lorsque la TEMA courte croise la TEMA longue à la baisse, le système génère un signal de vente.

- Utiliser le plus haut et le plus bas sur 10 périodes pour définir le niveau de stop-loss.

- Conserver la position après l’entrée jusqu’à l’apparition d’un signal inverse pour la clôturer.

Avantages de la stratégie

- Stabilité des signaux élevée : l’utilisation de TEMA à long terme permet de filtrer efficacement le bruit du marché et de réduire les faux signaux.

- Contrôle des risques complet : le stop-loss basé sur la volatilité permet de limiter efficacement le risque par transaction.

- Bonne capacité à saisir les tendances : la TEMA réagit plus rapidement aux tendances que les moyennes mobiles traditionnelles.

- Cycle de trading complet : conditions d’entrée, de stop-loss et de prise de bénéfices clairement définies.

- Paramètres hautement ajustables : tous les paramètres clés peuvent être adaptés en fonction des caractéristiques du marché.

Risques de la stratégie

- Risque de marché agité : dans un marché en range, des faux signaux peuvent entraîner des pertes consécutives.

- Risque de slippage : sur une période de 5 minutes, un slippage important peut survenir lors de mouvements violents.

- Risque de gestion du capital : un stop-loss en points fixes peut entraîner des pertes excessives en cas de forte volatilité.

- Retard du signal : l’indicateur TEMA présente un certain retard, ce qui peut faire manquer le point d’entrée optimal.

- Sensibilité des paramètres : les paramètres optimaux varient considérablement selon les conditions de marché.

Axes d’optimisation de la stratégie

- Ajouter une identification de l’environnement de marché : intégrer un indicateur de force de tendance pour utiliser différents paramètres selon les conditions.

- Optimiser la méthode de stop-loss : envisager un stop-loss dynamique basé sur l’ATR pour améliorer son adaptabilité.

- Améliorer la gestion de la taille des positions : ajuster dynamiquement le nombre de lots en fonction de la force de la tendance.

- Ajouter un mécanisme d’alerte : émettre des signaux d’alerte avancés aux niveaux de prix clés.

- Intégrer un indicateur de volume : confirmer la validité des signaux à l’aide du volume.

Conclusion

Cette stratégie est un système complet de suivi de tendance qui capture les tendances par le croisement de la TEMA et gère le risque grâce à un stop-loss dynamique. Sa logique est claire, sa mise en œuvre simple et elle présente une bonne praticabilité. Cependant, en trading réel, il est nécessaire de prêter attention à l’identification des conditions de marché et au contrôle des risques. Il est recommandé d’optimiser les paramètres en fonction des conditions réelles du marché après validation par backtest.

- 1