Stratégie de trading avec prise de bénéfices dynamique à plusieurs niveaux basée sur les Bandes de Bollinger et le filtre de quantile de volume

Aperçu

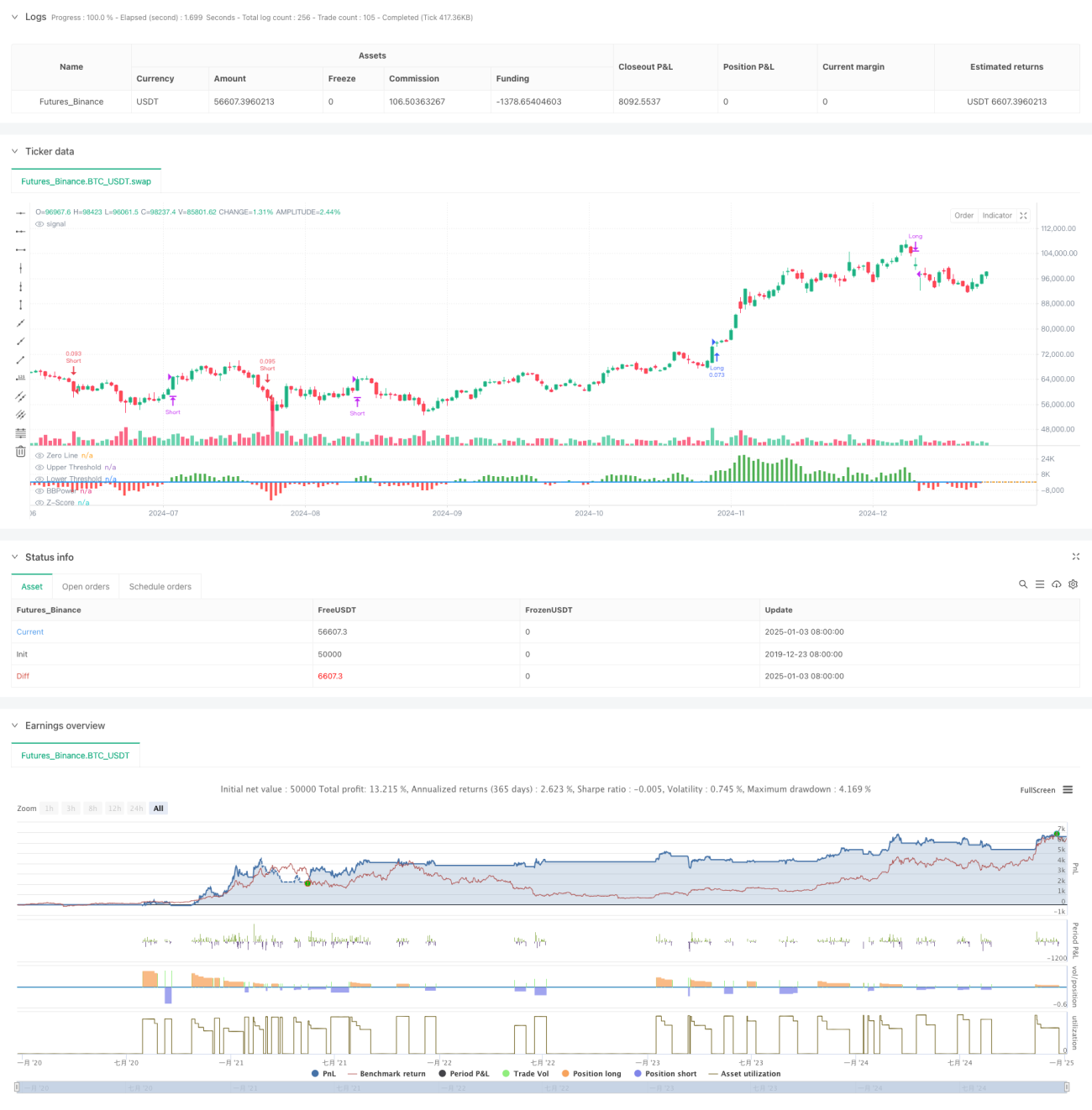

Cette stratégie est un système de trading quantitatif combinant l'indicateur Bull Bear Power (BBP) et un système de prise de profit dynamique à plusieurs niveaux basé sur les quantiles de volume. En analysant des données multidimensionnelles telles que le prix, le volume et la dynamique, elle construit un système de trading adaptable et à risque contrôlé. La logique centrale utilise la valeur Z-Score normalisée de l'indicateur BBP comme condition de déclenchement des signaux de trading, tout en combinant l'analyse des quantiles de volume pour ajuster dynamiquement les niveaux de prise de profit, permettant ainsi une maîtrise précise des différents états de volatilité du marché.

Principe de la stratégie

Le calcul central de la stratégie comprend les éléments clés suivants :

- Calcul de l'indicateur BBP : Mesure la force relative du marché en calculant la somme de la différence entre le plus haut et l'EMA (force haussière) et la différence entre le plus bas et l'EMA (force baissière).

- Normalisation Z-Score : Standardise la valeur BBP pour évaluer l'écart du niveau de force actuel du marché par rapport à la moyenne.

- Analyse du volume : Calcule le multiple du volume actuel par rapport à sa moyenne mobile pour évaluer l'activité du marché.

- Analyse des quantiles : Calcule les quantiles historiques du prix et du volume pour positionner la distribution de probabilité des états du marché.

- Prise de profit dynamique : Ajuste dynamiquement la distance de prise de profit en fonction d'un score composite basé sur l'ATR, le quantile de volume et le quantile de prix.

Avantages de la stratégie

- Analyse multidimensionnelle : Prend en compte la dynamique des prix, le volume et la position du marché pour une perspective plus complète.

- Forte adaptabilité : Grâce au mécanisme de prise de profit dynamique, elle s'adapte à différents environnements de marché.

- Diversification du risque : Utilise une stratégie de prise de profit à plusieurs niveaux pour libérer les bénéfices à différents niveaux de prix.

- Avantage probabiliste : Offre un avantage statistique significatif grâce au Z-Score et à l'analyse des quantiles.

- Extensibilité : Le cadre de la stratégie est facilement extensible pour ajouter de nouvelles dimensions d'analyse selon les besoins.

Risques de la stratégie

- Sensibilité aux paramètres : La stratégie comprend plusieurs paramètres qui doivent être optimisés en fonction des différents environnements de marché.

- Dépendance à l'environnement de marché : Peut donner des résultats médiocres en période de forte volatilité ou de changement de tendance.

- Slippage d'exécution : Les ordres de prise de profit à plusieurs niveaux peuvent subir un slippage, affectant les gains réels.

- Complexité de calcul : Le calcul en temps réel de plusieurs indicateurs peut entraîner une charge système.

- Risque de faux signaux : Peut générer des signaux erronés sur des marchés latéraux.

Directions d'optimisation

- Paramètres adaptatifs : Introduire des méthodes d'apprentissage automatique pour une optimisation automatique des paramètres.

- Anticipation du marché : Ajouter un module de classification de l'environnement de marché pour identifier à l'avance les conditions défavorables.

- Optimisation du stop-loss : Introduire un mécanisme de stop-loss dynamique pour améliorer la précision du contrôle des risques.

- Filtrage des signaux : Ajouter un filtre de force de tendance pour réduire les faux signaux.

- Gestion des positions : Optimiser l'algorithme d'allocation des positions pour améliorer l'efficacité de l'utilisation des fonds.

Résumé

Cette stratégie combine l'indicateur BBP traditionnel avec des méthodes d'analyse quantitative modernes pour construire un système de trading solide sur le plan théorique et pratique. Grâce au mécanisme de prise de profit à plusieurs niveaux et d'ajustement dynamique, elle équilibre bien les gains et les risques. Bien qu'il existe une certaine difficulté d'optimisation des paramètres, l'extensibilité du cadre de la stratégie offre une marge suffisante pour des améliorations ultérieures. En pratique, il est recommandé aux traders d'effectuer des ajustements ciblés en fonction des caractéristiques spécifiques du marché et de leur propre tolérance au risque.

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-04 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © PresentTrading

// The BBP Strategy with Volume-Percentile TP by PresentTrading emerges as a sophisticated approach that integrates multiple analytical layers to enhance trading precision and profitability. - 1