Stratégie de trading quantitatif multi-temporel basée sur le RSI lissé par EMA et le stop-loss/take-profit dynamique par ATR

Aperçu

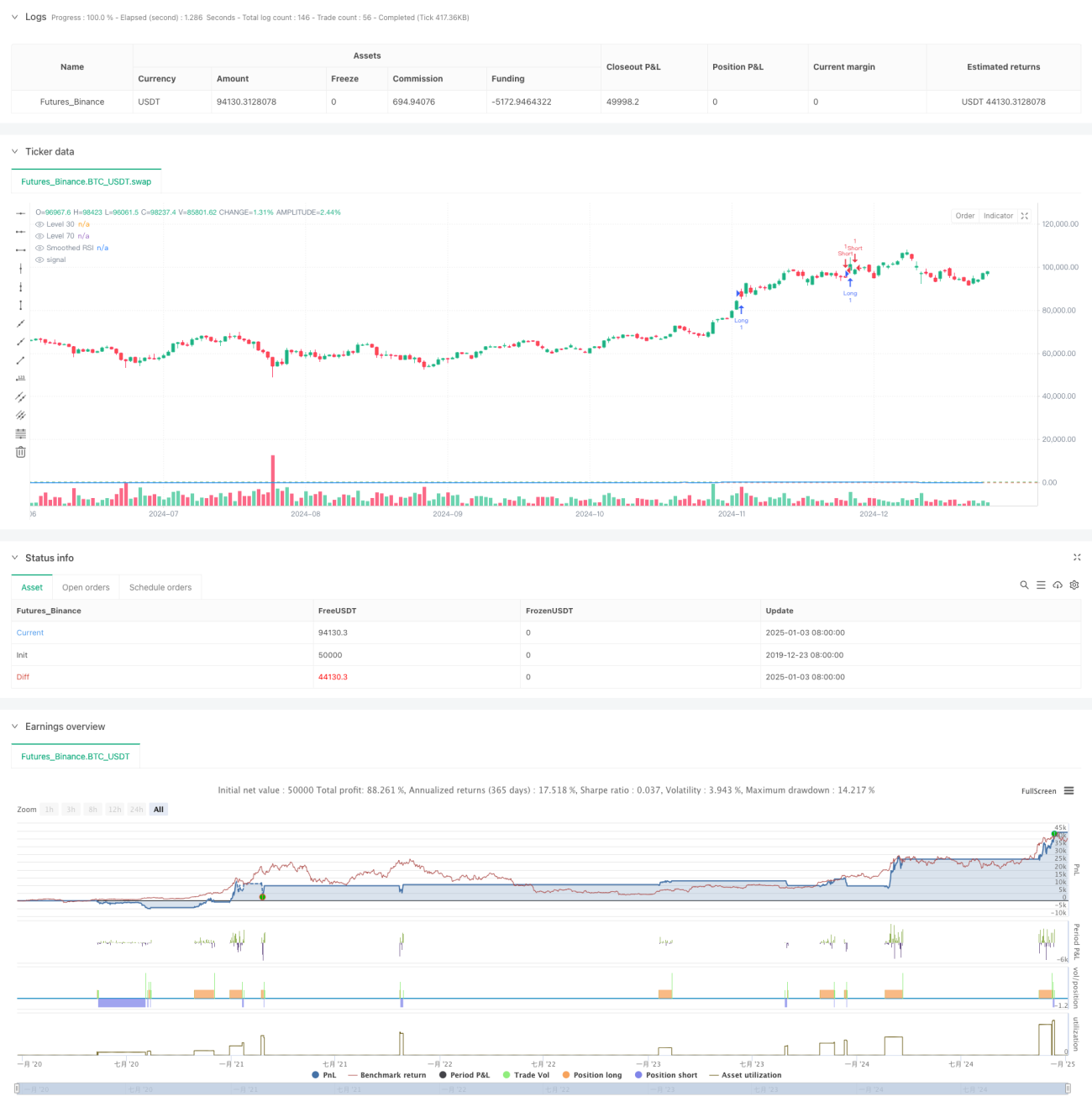

Cette stratégie est un système de trading quantitatif complet basé sur l'indice de force relative (RSI), la moyenne mobile exponentielle (EMA) et l'indicateur de volatilité réelle moyenne (ATR). La stratégie utilise l'EMA pour lisser le RSI, génère des signaux de trading lors des franchissements de seuils critiques du RSI, et utilise l'ATR pour définir dynamiquement les niveaux de stop-loss et de take-profit, assurant un contrôle efficace des risques. Par ailleurs, la stratégie intègre un compteur et un enregistrement des signaux de trading, facilitant le backtest et l'optimisation pour le trader.

Principe de la stratégie

La logique centrale de la stratégie comprend les éléments clés suivants :

- Utilisation d'un RSI sur 14 périodes pour évaluer les conditions de surachat et de survente du marché.

- Lissage du RSI via une EMA afin de réduire les faux signaux.

- Génération de signaux de trading lorsque le RSI franchit les seuils de 70 et 30 respectivement.

- Utilisation de l'ATR pour calculer dynamiquement les niveaux de stop-loss et de take-profit, offrant une plus grande flexibilité dans la gestion des risques.

- Mise en place d'un tableau de comptage des signaux de trading pour enregistrer les informations de prix de chaque trade.

Avantages de la stratégie

- Fort lissage des signaux : le lissage du RSI par l'EMA réduit efficacement les interférences des faux signaux de rupture.

- Gestion des risques complète : un schéma de stop-loss dynamique basé sur l'ATR s'adapte automatiquement à la volatilité du marché.

- Mécanisme de trading bidirectionnel : prend en charge les trades longs et courts pour exploiter pleinement les opportunités du marché.

- Paramètres ajustables : les paramètres clés sont entièrement personnalisables, permettant une optimisation selon les caractéristiques du marché.

- Suivi visuel : les signaux de trading sont enregistrés dans un tableau pour faciliter le suivi et l'analyse de backtest.

Risques de la stratégie

- Risque de faux signal RSI : même après lissage EMA, le RSI peut encore produire de fausses ruptures.

- Stop-loss inadapté de l'ATR : en cas de forte volatilité du marché, un mauvais réglage du multiple de l'ATR peut entraîner un stop-loss trop large ou trop serré.

- Risque d'optimisation excessive : une optimisation excessive des paramètres peut conduire à un surapprentissage de la stratégie.

- Dépendance aux conditions du marché : les performances peuvent différer significativement entre les marchés en tendance et ceux en range.

Directions d'optimisation de la stratégie

- Introduction d'une analyse multi-périodes : combiner des signaux RSI de plus longue période pour confirmer les trades.

- Optimisation du mécanisme de stop-loss : envisager d'ajuster dynamiquement le multiple de l'ATR en fonction des niveaux de support et de résistance.

- Ajout d'un jugement des conditions de marché : intégrer un indicateur de tendance pour ajuster les paramètres selon les environnements de marché.

- Amélioration du filtrage des signaux : envisager d'ajouter des indicateurs auxiliaires comme le volume pour filtrer les fausses ruptures.

- Introduction de la gestion de position : ajuster dynamiquement la taille des positions en fonction de la force du signal et de la volatilité du marché.

Résumé

Cette stratégie construit un système de trading quantitatif complet en combinant trois indicateurs techniques classiques : RSI, EMA et ATR. Elle démontre une forte praticabilité dans la génération de signaux, le contrôle des risques et l'exécution des trades. Avec une optimisation et une amélioration continues, la stratégie a le potentiel d'obtenir des performances stables dans le trading en temps réel. Cependant, les utilisateurs doivent être conscients de l'impact des conditions de marché sur les performances de la stratégie, définir correctement les paramètres et garantir une gestion rigoureuse des risques.

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-04 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("RSI Trading Strategy with EMA and ATR Stop Loss/Take Profit", overlay=true)

length = input.int(14, minval=1, title="RSI Length")

src = input(close, title="Source")- 1