Aperçu

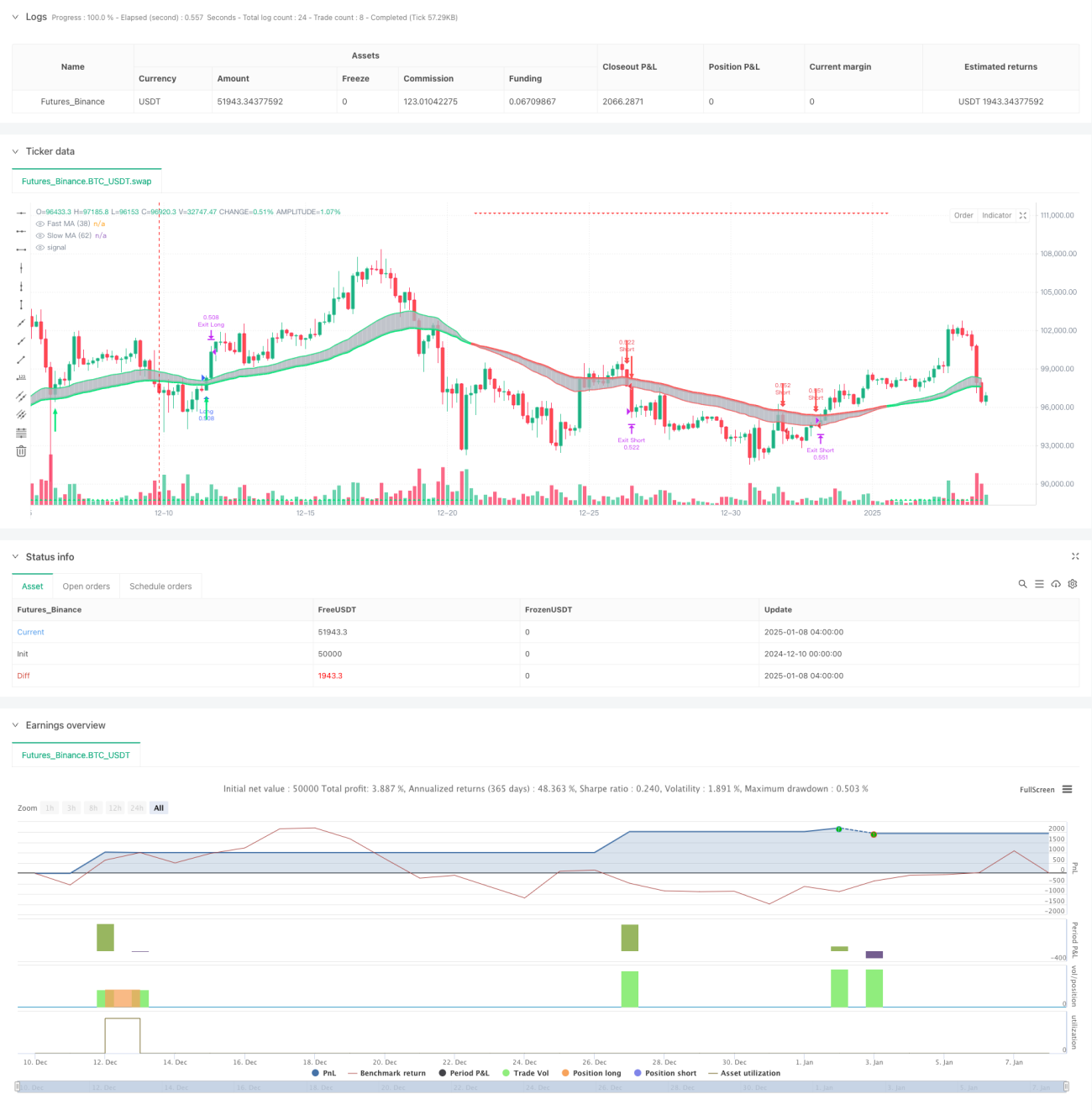

Cette stratégie est un système de trading de suivi de tendance basé sur un système à deux moyennes mobiles et un stop-loss dynamique basé sur l'ATR. Elle utilise les moyennes mobiles exponentielles (EMA) sur 38 et 62 périodes pour identifier la tendance du marché, les croisements du prix avec l'EMA rapide pour déterminer les signaux d'entrée, et intègre l'indicateur ATR pour une gestion dynamique du stop-loss. La stratégie propose deux modes de trading, agressif et conservateur, pour s'adapter aux différentes tolérances au risque des traders.

Principe de la stratégie

La logique centrale de la stratégie repose sur les éléments clés suivants :

- Détermination de la tendance : Identification de la tendance actuelle du marché via la position relative des EMA sur 38 et 62 périodes. Lorsque l'EMA rapide est au-dessus de l'EMA lente, la tendance est haussière ; dans le cas contraire, elle est baissière.

- Signal d'entrée : En tendance haussière, un signal long est généré lorsque le prix franchit par le bas l'EMA rapide ; en tendance baissière, un signal short est généré lorsque le prix casse par le haut l'EMA rapide.

- Gestion des risques : Utilisation d'un stop-loss dynamique basé sur l'ATR, ajusté au fur et à mesure que le prix évolue favorablement, protégeant ainsi les gains déjà acquis sans sortir prématurément. Parallèlement, des stop-loss et objectifs de profit fixes en pourcentage sont également définis.

Avantages de la stratégie

- Excellente performance de suivi de tendance : Le système à deux moyennes mobiles permet de capturer efficacement les tendances à moyen et long terme, évitant les transactions fréquentes sur les marchés en range.

- Gestion des risques complète : La combinaison de stop-loss fixes et dynamiques permet à la fois de limiter le risque maximal et de protéger les profits.

- Grande adaptabilité : Propose deux modes de trading (agressif et conservateur) pouvant être ajustés en fonction des conditions de marché et de l'appétence au risque individuelle.

- Feedback visuel clair : Les bougies de différentes couleurs et les flèches indiquent visuellement l'état du marché et les signaux de trading.

Risques de la stratégie

- Risque de retournement de tendance : Des stop-loss consécutifs peuvent survenir aux points de retournement. Il est conseillé de trader uniquement lorsque la tendance est claire.

- Risque de slippage : En cas de forte volatilité, le prix d'exécution réel peut s'écarter considérablement du prix du signal. Il convient d'élargir légèrement les plages de stop-loss.

- Sensibilité aux paramètres : Le choix des périodes de moyennes mobiles et du multiple ATR influence fortement les performances. Une optimisation en fonction des différentes conditions de marché est nécessaire.

Pistes d'optimisation de la stratégie

- Ajout d'un filtre de force de tendance : Introduire un indicateur de force de tendance tel que l'ADX, et n'entrer en position que lorsque la tendance est claire.

- Optimisation du mécanisme de stop-loss : Ajuster dynamiquement le multiple ATR en fonction de la volatilité, rendant le stop-loss plus adaptatif.

- Intégration de la confirmation par le volume : Lors de l'apparition d'un signal d'entrée, combiner l'analyse du volume pour améliorer la fiabilité du signal.

- Classification des environnements de marché : Ajuster dynamiquement les paramètres de la stratégie en fonction de différents environnements (tendance/range).

Résumé

Cette stratégie construit un système complet de trading de suivi de tendance en combinant le système classique à deux moyennes mobiles avec une technique moderne de stop-loss dynamique. Ses atouts résident dans une gestion des risques complète et une grande adaptabilité, mais le trader doit encore optimiser les paramètres et gérer les risques en fonction des conditions spécifiques du marché. Grâce aux pistes d'optimisation suggérées, la stabilité et la rentabilité de la stratégie pourraient être encore améliorées.

- 1