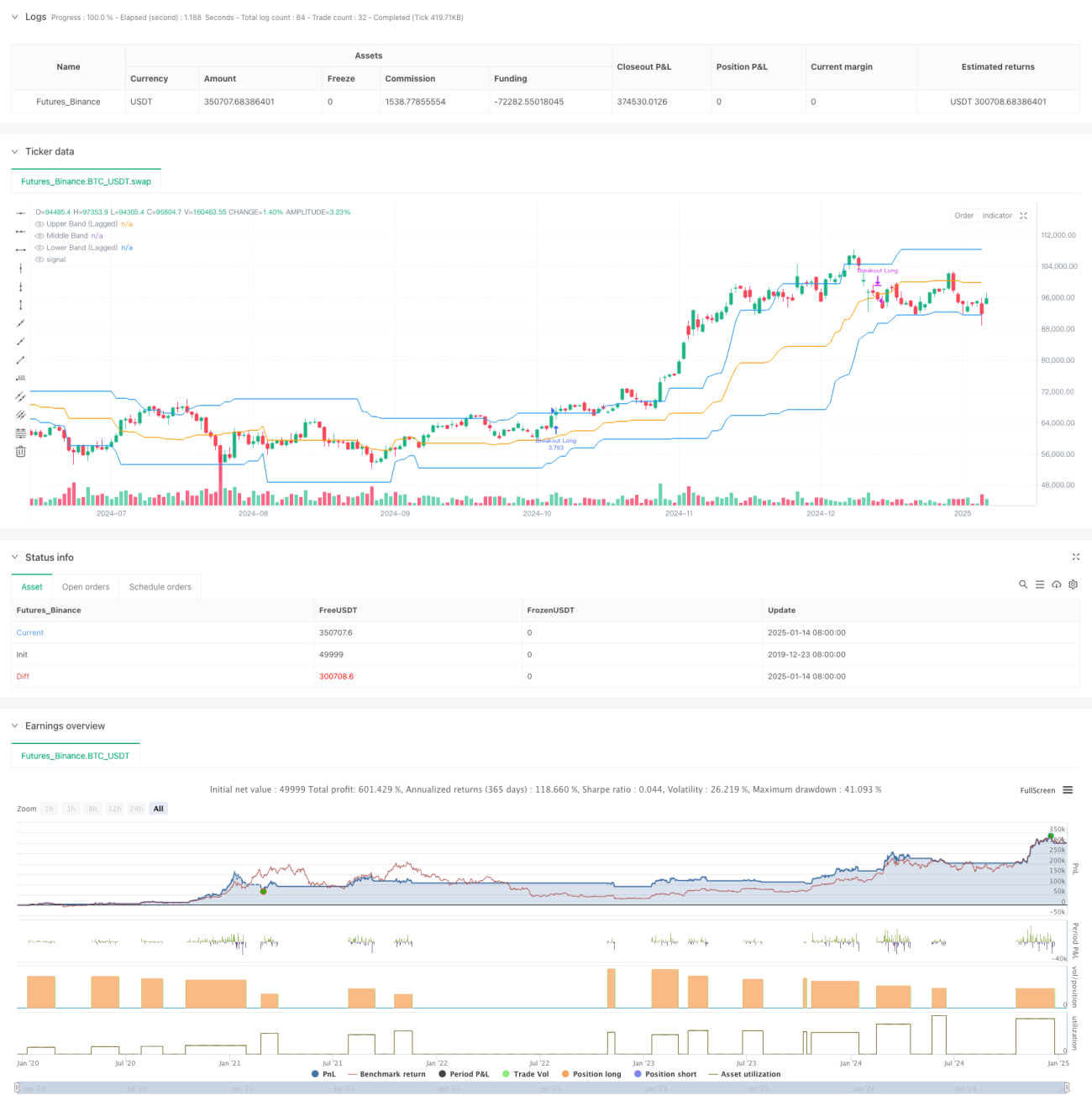

Aperçu

Il s'agit d'une stratégie de trading de rupture dynamique basée sur le canal de Donchian, combinant deux conditions clés : la rupture de prix et la confirmation de volume. La stratégie capture les tendances haussières en observant si le prix franchit une fourchette de prix prédéfinie et en exigeant un soutien du volume. Elle utilise un paramètre de décalage pour améliorer la stabilité du canal et propose des options de sortie flexibles.

Principe de la stratégie

La logique centrale de la stratégie comprend les éléments clés suivants :

- Utilisation d'un canal de Donchian décalé comme indicateur technique principal, construisant les bandes supérieure, médiane et inférieure à partir des plus hauts et plus bas des 27 dernières périodes.

- Les conditions d'entrée doivent être remplies simultanément :

- Le prix de clôture franchit la bande supérieure du canal de Donchian.

- Le volume actuel est supérieur à 1,4 fois le volume moyen des 27 dernières périodes.

- Conditions de sortie flexibles et optionnelles :

- Possibilité de sortie lorsque le prix casse la bande supérieure, la bande médiane ou la bande inférieure.

- Par défaut, la bande médiane est utilisée comme signal de sortie.

- Un paramètre de décalage de 10 périodes améliore la stabilité du canal et réduit les fausses ruptures.

Avantages de la stratégie

- Mécanisme de confirmation multiple : la combinaison de la rupture de prix et de la confirmation de volume réduit considérablement le risque de faux signaux.

- Adaptabilité : grâce à une conception paramétrique, la stratégie peut s'adapter à différents environnements de marché.

- Contrôle des risques complet : plusieurs options de sortie permettent un ajustement en fonction de différentes tolérances au risque.

- Exécution claire : les conditions d'entrée et de sortie sont nettes, sans ambiguïté.

- Facilité de mise en œuvre : la logique de la stratégie est simple et directe, adaptée à une exécution en temps réel.

Risques de la stratégie

- Risque de volatilité du marché : dans les marchés en range, des signaux de rupture fréquents et faux peuvent se produire.

- Risque de slippage : le volume est souvent élevé au moment de la rupture, ce qui peut entraîner un slippage important.

- Risque de retournement de tendance : en cas de retournement soudain du marché, la sortie peut ne pas être assez rapide.

- Sensibilité aux paramètres : l'efficacité de la stratégie est sensible au réglage des paramètres, nécessitant une optimisation minutieuse.

Axes d'optimisation de la stratégie

- Ajout d'un filtre de tendance : intégrer des indicateurs de tendance supplémentaires, comme un système de moyennes mobiles.

- Optimisation de l'indicateur de volume : utiliser des méthodes d'analyse de volume plus complexes, comme l'OBV ou l'indicateur de flux monétaire.

- Amélioration du stop-loss : ajouter un stop-loss suiveur ou un stop-loss fixe.

- Ajout d'un filtre temporel : filtrer les périodes intraday pour éviter les transactions pendant les créneaux horaires très volatils (ouverture et fermeture).

- Introduction de l'adaptation à la volatilité : ajuster automatiquement les paramètres en fonction de la volatilité du marché pour améliorer l'adaptabilité.

Résumé

Il s'agit d'une stratégie de suivi de tendance bien conçue et logiquement claire. En combinant la rupture de prix et la confirmation de volume, la stratégie garantit une fiabilité tout en conservant une bonne flexibilité. Sa conception paramétrique lui confère une bonne adaptabilité, mais elle nécessite également que l'investisseur l'optimise en fonction des conditions spécifiques du marché. Dans l'ensemble, c'est un cadre stratégique qui mérite d'être optimisé et mis en pratique.

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-15 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT","balance":49999}]

*/

//@version=6

strategy("Breakout Strategy", overlay=true, calc_on_every_tick=false, initial_capital=10000, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.1, pyramiding=1, fill_orders_on_standard_ohlc=true)

- 1