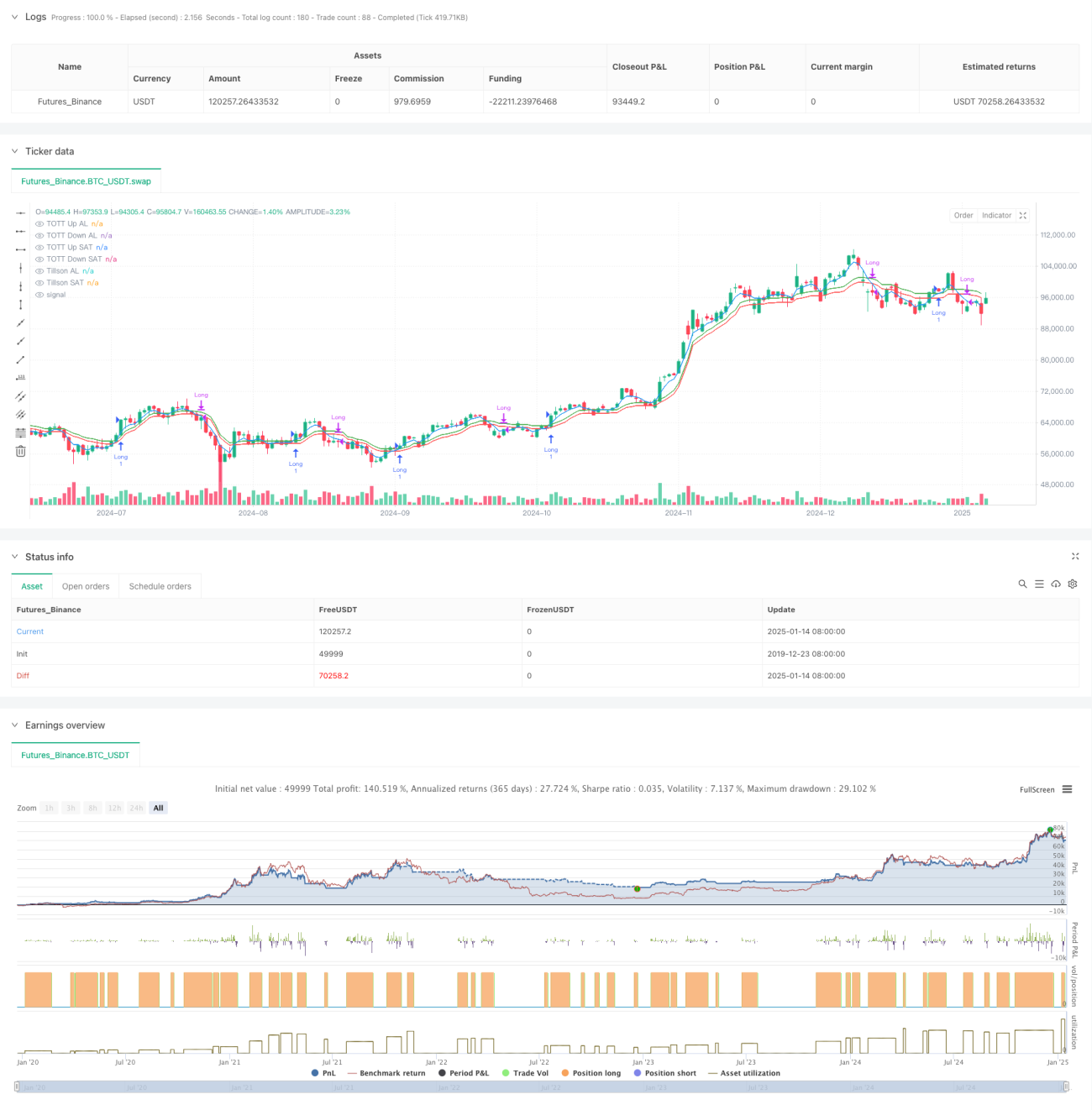

Aperçu

Cette stratégie est un système de suivi de tendance basé sur l'indicateur Tillson T3 et le Tracker de Tendance Double Optimisé (TOTT). Elle optimise la génération de signaux de trading en combinant l'oscillateur de momentum Williams %R. La stratégie utilise des paramètres d'achat et de vente séparés, ce qui permet d'ajuster la sensibilité de manière flexible en fonction des différentes conditions de marché, améliorant ainsi son adaptabilité.

Principe de la stratégie

La stratégie est principalement composée de trois éléments centraux :

- Indicateur Tillson T3 – Il s'agit d'une variante optimisée de la moyenne mobile exponentielle (EMA), qui produit une ligne de tendance plus lisse grâce à un calcul pondéré par plusieurs EMA.

- Tracker de Tendance Double Optimisé (TOTT) – Un outil de suivi de tendance qui s'ajuste de manière adaptative en fonction du comportement des prix et du coefficient de volatilité, calculant respectivement les bandes supérieure et inférieure pour les conditions d'achat et de vente.

- Indicateur Williams %R – Un oscillateur de momentum utilisé pour identifier les conditions de surachat et de survente.

Logique de génération des signaux de trading :

- Condition d'achat : lorsque la ligne T3 franchit la bande supérieure du TOTT et que le Williams %R est supérieur à -20 (survente).

- Condition de vente : lorsque la ligne T3 franchit à la baisse la bande inférieure du TOTT et que le Williams %R est supérieur à -70.

Avantages de la stratégie

- Stabilité élevée des signaux – Grâce au lissage multiple de l'indicateur T3, le risque de faux signaux de rupture est efficacement réduit.

- Bonne adaptabilité – La conception avec paramètres d'achat et de vente séparés permet une optimisation indépendante pour différentes conditions de marché.

- Gestion des risques complète – L'intégration du Williams %R comme confirmation secondaire améliore la fiabilité des transactions.

- Visualisation claire – La stratégie offre un support visuel complet sur les graphiques, facilitant l'analyse et la prise de décision.

Risques de la stratégie

- Retard dans le retournement de tendance – Le lissage multiple de l'indicateur T3 peut entraîner un retard dans les signaux.

- Inadaptée aux marchés latéraux – En période de consolidation horizontale, elle peut générer un excès de signaux de trading.

- Haute sensibilité aux paramètres – Nécessite des ajustements fréquents des paramètres en fonction des différentes conditions de marché.

Recommandations pour la gestion des risques :

- Introduire un mécanisme de stop-loss.

- Fixer des limites sur le volume des transactions.

- Ajouter un filtre de confirmation de tendance.

Directions d'optimisation de la stratégie

- Optimisation dynamique des paramètres – Développer un mécanisme d'ajustement adaptatif des paramètres.

- Ajout de l'identification de l'environnement de marché – Introduire un indicateur de force de tendance.

- Amélioration de la gestion des risques – Ajouter un stop-loss et un take-profit dynamiques.

- Renforcement du filtrage des signaux – Intégrer davantage d'indicateurs techniques pour confirmation.

Résumé

Il s'agit d'une stratégie de suivi de tendance à la structure complète et à la logique claire. En combinant l'indicateur T3 et le TOTT, avec le filtrage du Williams %R, elle démontre d'excellentes performances sur les marchés en tendance. Bien qu'elle présente un certain retard, grâce à l'optimisation des paramètres et à l'amélioration de la gestion des risques, cette stratégie offre une bonne valeur pratique et un potentiel d'extension.

- 1