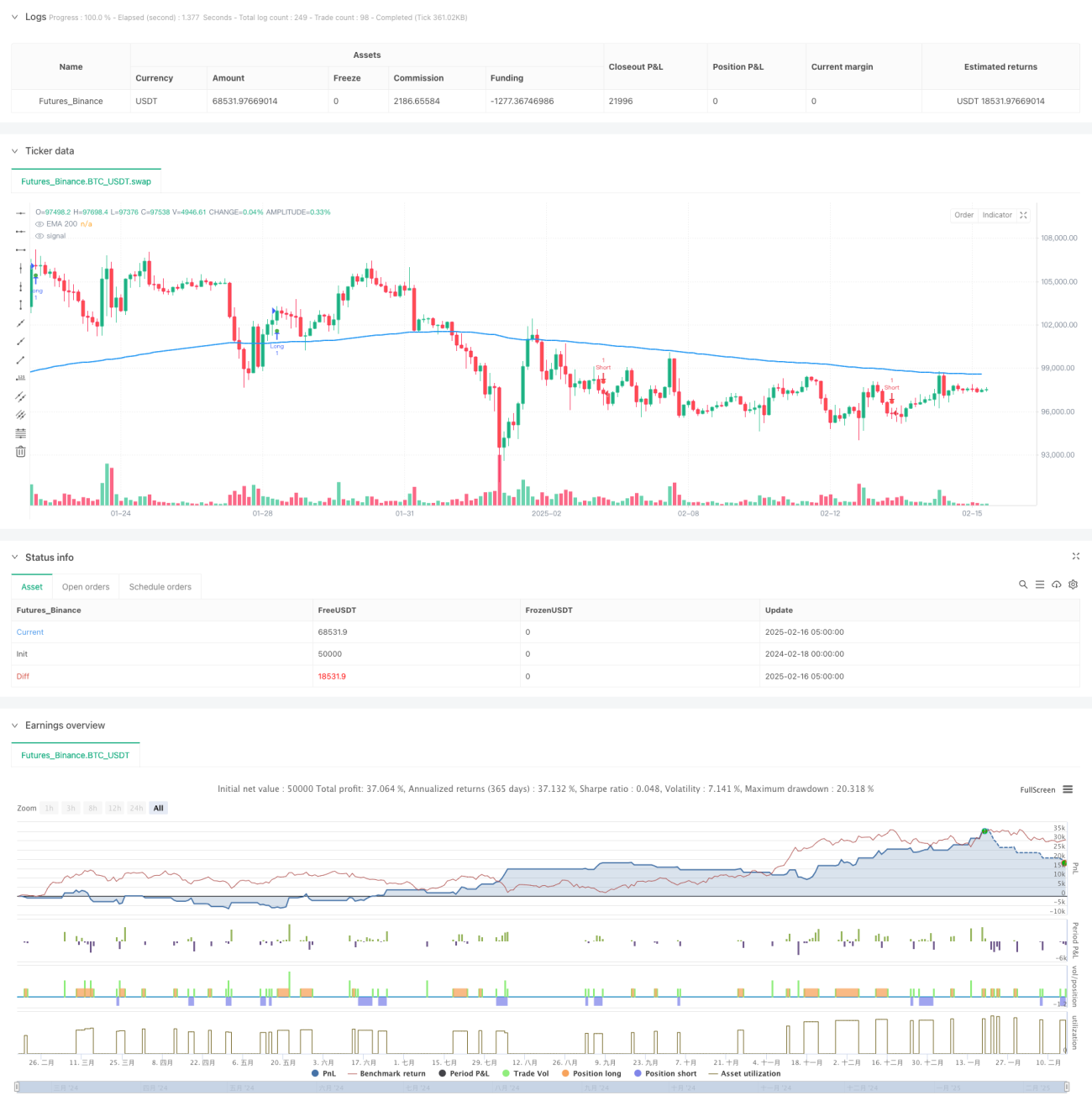

Aperçu

Cette stratégie est un système de trading complet basé sur de multiples indicateurs techniques, combinant des indicateurs de momentum, de tendance et de volatilité, afin de capter les opportunités de mouvements à court terme sur le marché. Elle identifie les opportunités de trading via les signaux de croisement du MACD, la confirmation de tendance par l’EMA, les conditions de surachat/survente du RSI et le filtrage de force de tendance par l’ADX, et utilise un stop-loss et take-profit dynamiques basés sur l’ATR pour gérer le risque.

Principe de la stratégie

La logique centrale de la stratégie repose sur les éléments clés suivants :

- L’indicateur MACD capture les changements de momentum, les croisements entre la ligne rapide et la ligne lente déterminent les points d’entrée.

- L’EMA sur 200 périodes confirme la direction générale de la tendance : un prix au-dessus de la moyenne mobile indique une tendance haussière, et inversement pour une tendance baissière.

- Le RSI confirme le momentum du prix : un RSI > 50 favorise les positions longues, un RSI < 50 favorise les positions courtes.

- L’ADX filtre les tendances faibles : on n’entre en position que lorsque l’ADX dépasse un seuil défini.

- L’ATR sert à calculer dynamiquement les niveaux de stop-loss et de take-profit, en s’adaptant à la volatilité du marché.

Avantages de la stratégie

- Validation croisée par plusieurs indicateurs, augmentant la fiabilité des signaux.

- Système de gestion dynamique des risques, ajustant automatiquement le stop-loss et le take-profit en fonction de la volatilité du marché.

- Grande adaptabilité, possibilité d’ajuster les paramètres selon les conditions de marché.

- Mécanisme complet de confirmation de tendance, réduisant le risque de faux dépassements.

- Logique d’entrée et de sortie systématique, limitant les jugements subjectifs.

Risques de la stratégie

- La multiplicité des indicateurs peut entraîner un retard des signaux.

- Les périodes courtes sont sensibles au bruit du marché.

- L’optimisation des paramètres peut conduire à un surapprentissage.

- Les transactions à haute fréquence peuvent générer des coûts de transaction élevés.

- En cas de forte volatilité, les stop-loss peuvent être déclenchés fréquemment.

Axes d’optimisation de la stratégie

- Intégrer le volume comme confirmation supplémentaire.

- Optimiser le seuil de l’ADX pour améliorer l’efficacité du filtrage de tendance.

- Ajouter un filtre temporel pour éviter les périodes de faible liquidité.

- Développer un système de paramètres adaptatifs pour améliorer la stabilité de la stratégie.

- Ajouter un filtre de volatilité du marché pour s’adapter à différents environnements.

Conclusion

Cette stratégie construit un système de trading complet en combinant plusieurs indicateurs techniques. Bien qu’elle présente un certain retard et des défis d’optimisation des paramètres, elle montre une bonne adaptabilité et fiabilité grâce à une gestion des risques adéquate et une amélioration continue. Il est recommandé aux traders de réaliser des backtests approfondis et une optimisation des paramètres avant une utilisation en conditions réelles.

- 1