Système de trading de suivi de tendance avec stop-loss dynamique basé sur l'ATR

Aperçu

Cette stratégie est un système de suivi de tendance basé sur un stop suiveur dynamique utilisant l'ATR (Average True Range). Elle combine une moyenne mobile exponentielle (EMA) comme filtre de tendance, et contrôle la génération de signaux en ajustant un paramètre de sensibilité et la période de l'ATR. Le système prend en charge à la fois les positions longues et courtes, et dispose d'un mécanisme complet de gestion des profits.

Principe de la stratégie

- Utilisation de l'indicateur ATR pour calculer l'amplitude des fluctuations de prix et déterminer la distance du stop suiveur en fonction du coefficient de sensibilité défini (Key Value).

- Détermination de la direction de la tendance du marché via une EMA : une position longue n'est ouverte que lorsque le prix est au-dessus de la moyenne mobile, et une position courte lorsqu'il est en dessous.

- Lorsque le prix franchit la ligne de stop suiveur et correspond à la direction de la tendance, un signal de transaction est déclenché.

- Le système gère les positions par une prise de profit par paliers :

- Lorsque le profit atteint 20 % à 50 %, le stop est relevé au prix de revient (point mort).

- Lorsque le profit atteint 50 % à 80 %, une partie de la position est liquidée et le stop est resserré.

- Lorsque le profit atteint 80 % à 100 %, le stop est encore resserré pour protéger les gains.

- Lorsque le profit dépasse 100 %, la totalité de la position est clôturée pour prendre les bénéfices.

Avantages de la stratégie

- Le stop suiveur dynamique permet de suivre efficacement la tendance, protégeant les profits sans sortir prématurément.

- Le filtre de tendance par EMA réduit efficacement le risque lié aux faux signaux de cassure.

- Le mécanisme de prise de profit par paliers garantit la réalisation des gains tout en laissant suffisamment d'espace pour le développement de la tendance.

- La prise en charge des transactions à la hausse comme à la baisse permet de tirer pleinement parti des opportunités du marché.

- Les paramètres sont hautement ajustables pour s'adapter à différents environnements de marché.

Risques de la stratégie

- Sur un marché volatil sans tendance claire, des transactions fréquentes peuvent entraîner des pertes.

- En début de retournement de tendance, des drawdowns importants peuvent survenir.

- Un réglage inadéquat des paramètres peut affecter les performances de la stratégie.

Recommandations de gestion des risques :

- Utiliser de préférence sur des marchés présentant une tendance nette.

- Choisir les paramètres avec soin, de préférence après optimisation via backtesting.

- Fixer une limite de drawdown maximal.

- Envisager d'ajouter des filtres d'environnement de marché.

Pistes d'optimisation de la stratégie

- Ajouter un mécanisme d'identification de l'environnement de marché pour utiliser des paramètres différents selon les conditions.

- Introduire des indicateurs auxiliaires comme le volume pour renforcer la fiabilité des signaux.

- Optimiser le mécanisme de gestion des profits en ajustant dynamiquement les objectifs de profit en fonction de la volatilité.

- Ajouter un filtre temporel pour éviter de trader pendant les périodes défavorables.

- Envisager d'ajouter un filtre de volatilité pour réduire la fréquence des transactions en cas de fluctuations excessives.

Résumé

Il s'agit d'un système de suivi de tendance bien structuré et logique. En combinant le suivi dynamique de l'ATR et le filtre de tendance de l'EMA, il permet de bien maîtriser les risques tout en capturant les tendances. Le mécanisme de prise de profit par paliers témoigne d'une réflexion mature en matière de trading. La stratégie présente une forte praticabilité et une bonne évolutivité ; avec une optimisation et une amélioration continues, elle est susceptible d'obtenir de meilleurs résultats de trading.

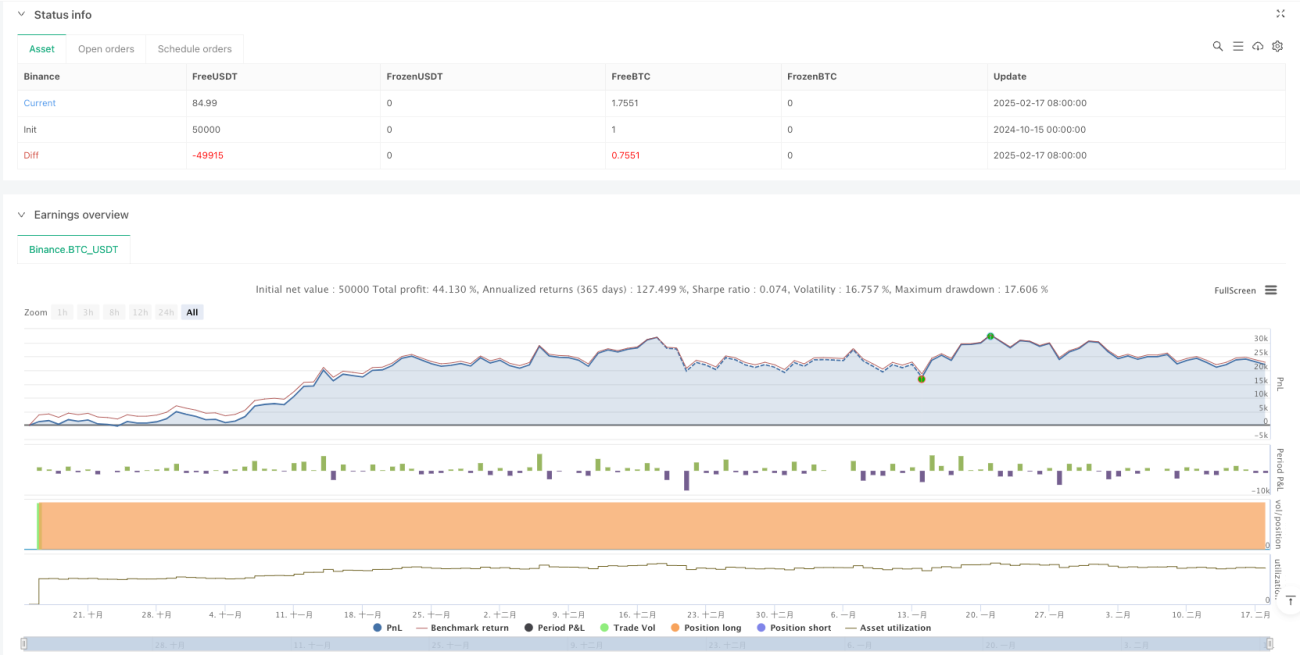

/*backtest

start: 2024-10-15 00:00:00

end: 2025-02-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Enhanced UT Bot with Long & Short Trades", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// Input Parameters- 1