Aperçu

Cette stratégie est un système de trading quantitatif qui combine un canal gaussien (Gaussian Channel) et un indice de force relative stochastique (Stochastic RSI). La stratégie capture les opportunités de retournement de tendance en surveillant le croisement du prix avec le canal gaussien ainsi que l'évolution du Stochastic RSI. Le canal gaussien est construit à partir d'une moyenne mobile et d'un écart-type, reflétant dynamiquement la plage de volatilité du marché, tandis que le Stochastic RSI fournit un signal de confirmation du côté de la dynamique.

Principe de la stratégie

La logique centrale de la stratégie comprend les éléments clés suivants :

- Construction du canal gaussien : utilisation d'une moyenne mobile exponentielle (EMA) sur 20 périodes comme axe central du canal. Les bornes supérieure et inférieure du canal sont obtenues en ajoutant ou soustrayant 2 fois l'écart-type à cet axe.

- Calcul du Stochastic RSI : d'abord, calcul du RSI sur 14 périodes, puis application de la formule stochastique sur 14 périodes à la valeur du RSI, enfin lissage sur 3 périodes du résultat pour obtenir les lignes K et D.

- Génération des signaux de trading : lorsque le prix franchit la borne supérieure du canal gaussien et que la ligne K du Stochastic RSI dépasse la ligne D à la hausse, un signal d'achat est généré ; lorsque le prix casse en dessous de la borne supérieure du canal gaussien, la position est fermée.

Avantages de la stratégie

- Haute fiabilité des signaux : la combinaison d'indicateurs de tendance et de dynamique permet de réduire efficacement les faux signaux.

- Contrôle des risques solide : grâce à la nature dynamique du canal gaussien, la stratégie ajuste automatiquement la zone de transaction en fonction de la volatilité du marché.

- Forte adaptabilité : via une conception paramétrable, la stratégie peut s'adapter à différents environnements de marché et instruments de trading.

- Haute efficacité d'exécution : la logique de la stratégie est claire et simple, avec un faible volume de calcul, adaptée au trading en temps réel.

Risques de la stratégie

- Risque de retard : le calcul de la moyenne mobile et de l'écart-type présente un certain décalage, ce qui peut entraîner un retard dans le timing d'entrée.

- Risque de faux dépassement : dans un marché sans tendance (range), des signaux de faux dépassements peuvent survenir fréquemment.

- Sensibilité aux paramètres : l'efficacité de la stratégie est relativement sensible au réglage des paramètres ; différents environnements de marché peuvent nécessiter un ajustement des paramètres.

- Dépendance à l'environnement de marché : dans les marchés latéraux sans tendance claire, la performance de la stratégie peut être médiocre.

Directions d'optimisation de la stratégie

- Optimisation du filtrage des signaux : ajout d'indicateurs auxiliaires tels que le volume ou la volatilité pour filtrer les signaux de trading.

- Ajustement dynamique des paramètres : introduction d'un mécanisme adaptatif pour ajuster dynamiquement les paramètres du canal et du Stochastic RSI en fonction de l'état du marché.

- Amélioration du mécanisme de stop-loss : ajout d'un stop-loss suiveur ou d'un stop-loss dynamique basé sur la volatilité.

- Optimisation de la gestion de position : ajustement dynamique de la taille de la position en fonction de la force du signal et de la volatilité du marché.

Résumé

Cette stratégie construit un système de trading quantitatif à la logique complète et au risque contrôlable en combinant des indicateurs de suivi de tendance et de dynamique issus de l'analyse technique. Bien qu'elle présente certains risques inhérents, grâce à une optimisation et une amélioration continues, la stratégie peut potentiellement maintenir des performances stables dans différents environnements de marché. Sa conception modulaire offre également une bonne base pour les optimisations et extensions futures.

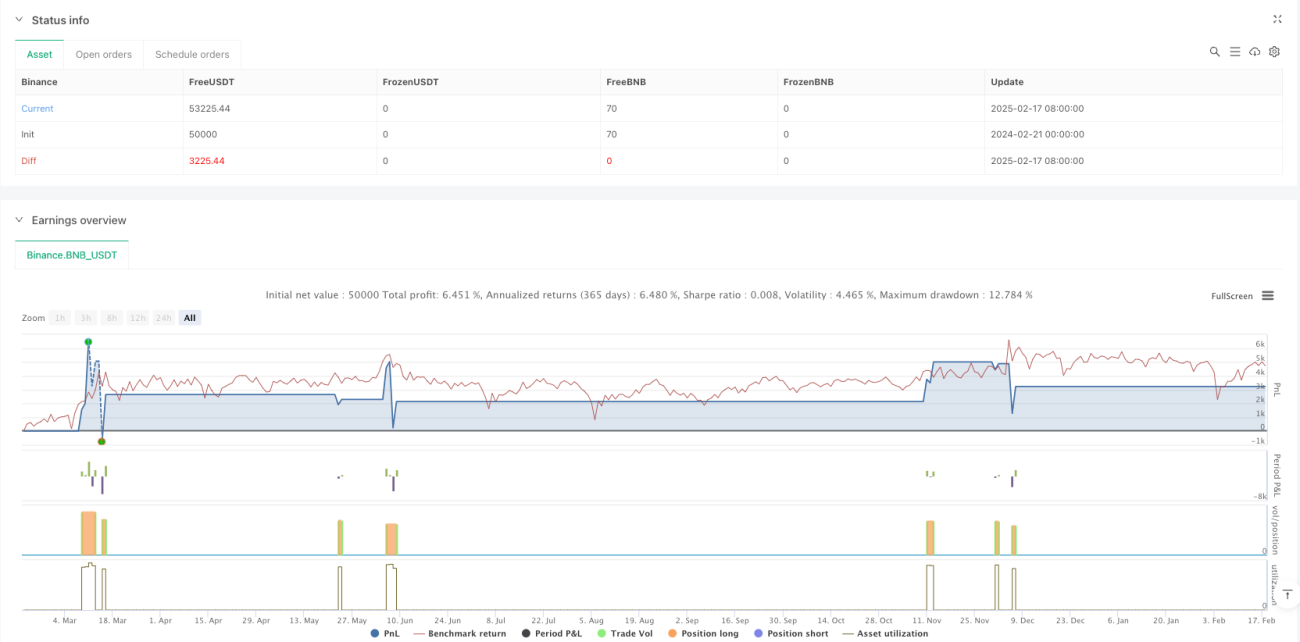

/*backtest

start: 2024-02-21 00:00:00

end: 2025-02-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Binance","currency":"BNB_USDT"}]

*/

//@version=5

strategy("SAJJAD JAMSHIDI Channel with Stochastic RSI Strategy", overlay=true, commission_type=strategy.commission.percent, commission_value=0.1, slippage=0, default_qty_type=strategy.percent_of_equity, default_qty_value=100, process_orders_on_close=true)

// Gaussian Channel Inputs- 1