Stratégie de trading intégrée multidimensionnelle basée sur Nadaraya-Watson

Aperçu

Cette stratégie est un système de trading multidimensionnel basé sur la régression à noyau de Nadaraya-Watson. Elle intègre les informations de quatre dimensions du marché – technique, émotionnelle, supra-sensorielle et intentionnelle – pour former des signaux composites guidant les décisions de trading. La stratégie utilise une méthode d’optimisation des poids, pondérant les signaux des différentes dimensions, et combine des filtres de tendance et de momentum pour améliorer la qualité des signaux. Le système comprend également un module complet de gestion des risques, protégeant le capital via des stop-loss et take-profit.

Principe de la stratégie

Le cœur de la stratégie consiste à lisser les données de marché multidimensionnelles par la méthode de régression à noyau de Nadaraya-Watson. Concrètement :

- La dimension technique utilise le prix de clôture.

- La dimension émotionnelle utilise l’indicateur RSI.

- La dimension supra-sensorielle utilise la volatilité ATR.

- La dimension intentionnelle utilise l’écart du prix par rapport à sa moyenne mobile.

Ces dimensions, après lissage par régression à noyau, sont intégrées avec des poids prédéfinis (technique 0,4, émotion 0,2, supra-sensoriel 0,2, intentionnel 0,2) pour former le signal de trading final. Lorsque le signal intégré croise sa moyenne mobile, en conjonction avec les filtres de tendance et de momentum confirmés, un ordre de trading est émis.

Avantages de la stratégie

- L’analyse multidimensionnelle offre une vision plus complète du marché, évitant les limites d’un seul indicateur.

- La régression à noyau de Nadaraya-Watson réduit efficacement le bruit du marché et fournit des signaux plus lissés.

- Le mécanisme d’optimisation des poids permet d’ajuster l’importance de chaque dimension en fonction des caractéristiques du marché.

- L’ajout de filtres de tendance et de momentum améliore significativement la qualité des signaux.

- Un système de gestion des risques complet assure la sécurité du capital.

Risques de la stratégie

- Une optimisation excessive des paramètres peut conduire à un surajustement.

- De multiples conditions de filtrage peuvent faire manquer certains signaux valables.

- La complexité de calcul de la régression à noyau peut impacter les performances en temps réel.

- Une répartition inappropriée des poids peut affaiblir certains signaux de marché importants.

Les mesures d’atténuation incluent : validation des paramètres sur des données hors échantillon, ajustement dynamique des filtres, optimisation de l’efficacité de calcul, et évaluation/rééquilibrage périodique de la répartition des poids.

Axes d’optimisation de la stratégie

- Introduire un système de poids adaptatif, ajustant dynamiquement les poids de chaque dimension en fonction des conditions de marché.

- Développer des mécanismes de filtrage plus intelligents pour équilibrer qualité et quantité des signaux.

- Optimiser l’implémentation de l’algorithme de Nadaraya-Watson pour améliorer l’efficacité de calcul.

- Ajouter un module d’identification des cycles de marché, utilisant des paramètres différents selon les phases du marché.

- Étendre le système de gestion des risques, en y intégrant des stop-loss dynamiques et des fonctionnalités de gestion de position.

Résumé

Cette stratégie est une approche innovante alliant méthodes mathématiques et sagesse du trading. Grâce à une analyse multidimensionnelle et à des outils mathématiques avancés, la stratégie capture plusieurs niveaux du marché et fournit des signaux de trading relativement fiables. Bien qu’il existe des marges d’optimisation, le cadre global de la stratégie est robuste et présente une valeur pratique.

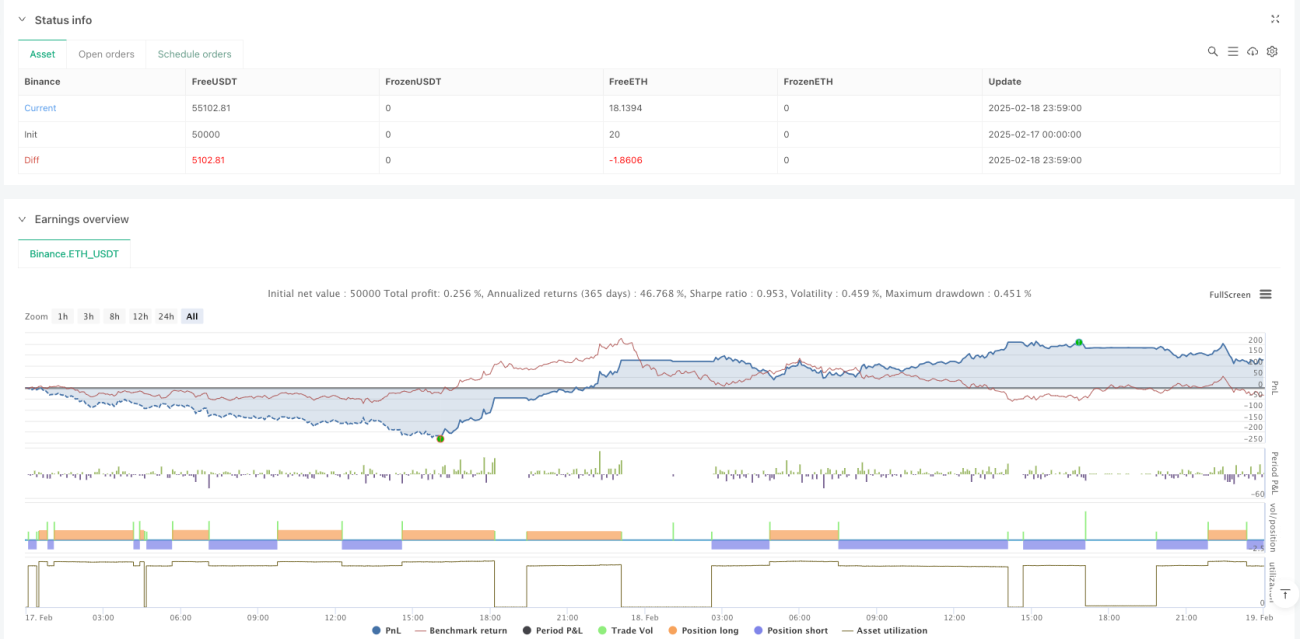

/*backtest

start: 2025-02-17 00:00:00

end: 2025-02-19 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

//@version=5

strategy("Enhanced Multidimensional Integration Strategy with Nadaraya", overlay=true, initial_capital=10000, currency=currency.USD, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

//────────────────────────────────────────────────────────────────────────────- 1