Aperçu

Cette stratégie de trading repose sur le principe de réversion à la moyenne des bandes de Bollinger, en réalisant des profits par paliers via plusieurs niveaux de prise de bénéfices. La stratégie entre en position lorsque le prix franchit les bandes de Bollinger puis revient à l'intérieur, et définit cinq niveaux distincts de prise de bénéfices pour réduire progressivement la position. Un stop loss dynamique est également mis en place pour contrôler le risque. La stratégie peut fonctionner pendant des périodes de trading personnalisées et permet d'ajouter des positions.

Principe de la stratégie

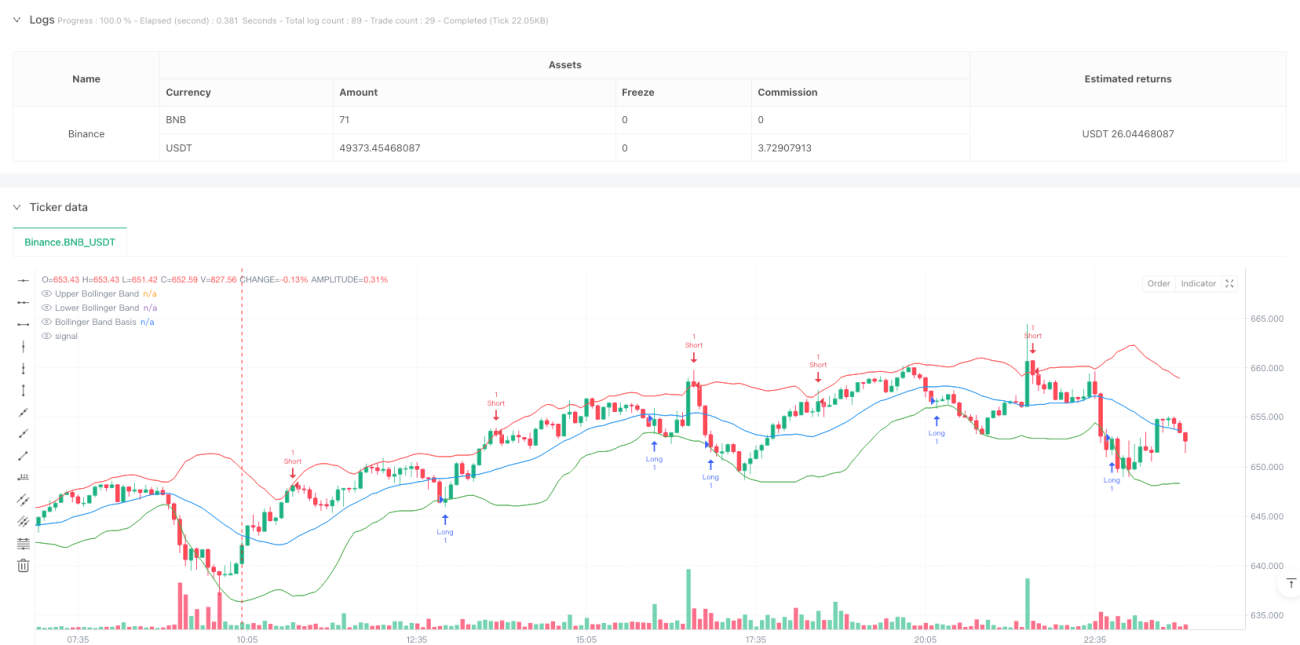

La stratégie utilise l'indicateur des bandes de Bollinger sur 20 périodes, avec un écart-type de 2 comme intervalle de volatilité. Lorsque le prix franchit la bande inférieure par le bas et clôture à l'intérieur, un signal long est déclenché ; lorsque le prix franchit la bande supérieure par le haut et clôture à l'intérieur, un signal short est déclenché. Après l'entrée, la stratégie applique un mécanisme de prise de bénéfices en cinq étapes, avec des niveaux fixés à 0,5 %, 1 %, 1,5 %, 2 % et 2,5 %, chacun clôturant 20 % de la position. Le dernier niveau de prise de bénéfices est positionné sur la bande de Bollinger opposée. Parallèlement, un stop loss de 1 % est défini pour limiter le risque.

Avantages de la stratégie

- Le mécanisme de prise de bénéfices multi-niveaux permet de capter davantage de gains en cas de tendance prolongée, tout en verrouillant une partie des profits.

- Possibilité d'ajouter des positions lorsque la direction du trade est correcte, améliorant ainsi la rentabilité.

- Utilisation des bandes de Bollinger comme niveaux dynamiques de support/résistance, adaptés à la volatilité du marché.

- Personnalisation des périodes de trading pour éviter les interférences en dehors des horaires d'activité.

- Présence d'un stop loss pour maîtriser efficacement le risque.

Risques de la stratégie

- Dans les marchés très volatils, des signaux de faux dépassements peuvent se déclencher fréquemment.

- En cas de tendance rapide, des opportunités de gains plus importants peuvent être manquées.

- Le mécanisme d'ajout de positions peut entraîner des pertes plus importantes lors d'un retournement de marché.

- Les multiples ordres de prise de bénéfices risquent de ne pas être exécutés complètement en raison d'un manque de liquidité.

Il est recommandé d'ajuster les paramètres des bandes de Bollinger ainsi que les ratios de prise de bénéfices et de stop loss pour s'adapter aux différentes conditions de marché.

Axes d'optimisation de la stratégie

- Intégrer des indicateurs de volume comme filtre de signal pour améliorer la fiabilité des dépassements.

- Ajuster dynamiquement les niveaux de prise de bénéfices et de stop loss en fonction de la volatilité.

- Ajouter un filtre de tendance pour éviter de trader à contre-tendance en cas de forte tendance.

- Optimiser la logique d'ajout de positions en fixant une limite maximale de détention.

- Envisager d'ajouter une fonction de stop loss suiveur pour mieux protéger les profits.

Conclusion

Cette stratégie exploite les opportunités de réversion à la moyenne via l'indicateur des bandes de Bollinger, en gérant le risque grâce à une prise de bénéfices multi-niveaux et un stop loss dynamique. Son principal atout réside dans la flexibilité de la gestion de position et du contrôle du risque, mais il convient de l'adapter aux conditions du marché. L'ajout de filtres supplémentaires et l'optimisation des paramètres de prise de bénéfices et de stop loss peuvent encore améliorer sa stabilité et sa rentabilité.

- 1