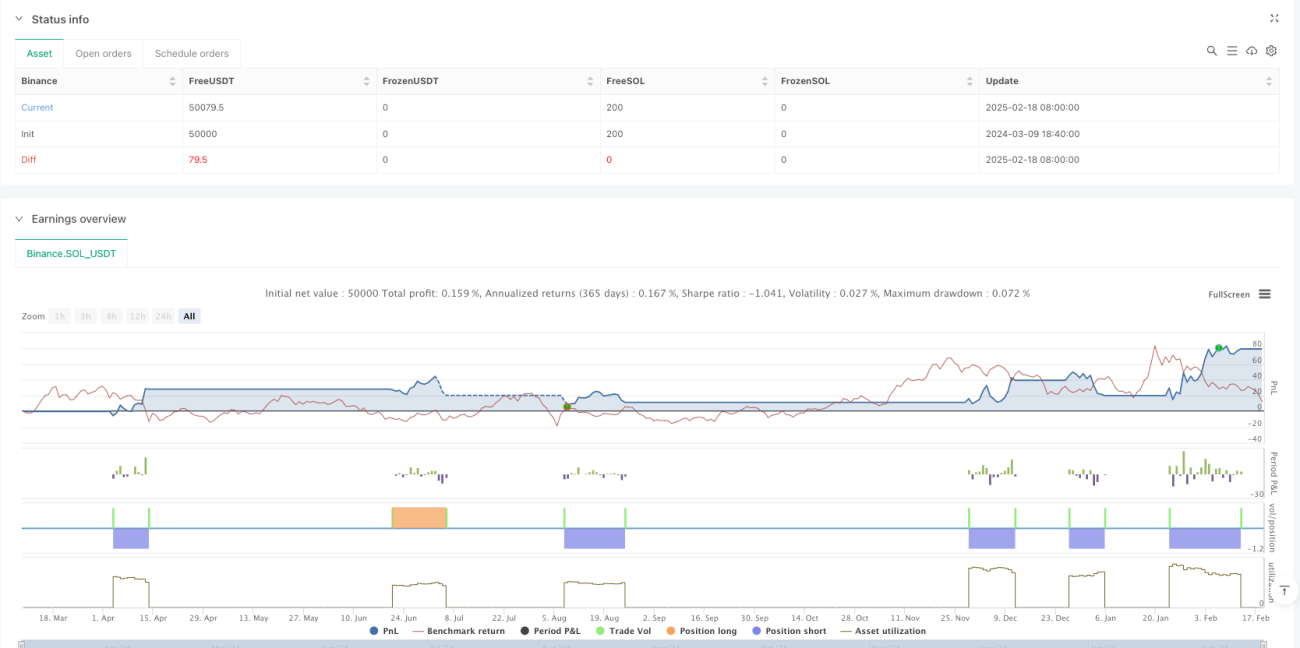

Aperçu

Cette stratégie analyse le sentiment du marché à partir des configurations de chandeliers japonais et quantifie la psychologie du marché à l'aide de trois oscillateurs principaux (oscillateur d'hésitation, oscillateur de peur et oscillateur de cupidité). Elle combine des indicateurs de momentum et de tendance, tout en intégrant la confirmation de volume, pour constituer un système de trading complet. Cette stratégie est destinée aux traders souhaitant identifier des opportunités de trading à haute probabilité grâce à l'analyse du sentiment du marché.

Principe de la stratégie

Le cœur de la stratégie consiste à construire trois oscillateurs de sentiment en analysant différentes configurations de chandeliers :

- Oscillateur d'hésitation – mesure l'incertitude du marché via les configurations de doji et de toupie.

- Oscillateur de peur – suit le sentiment baissier via les étoiles filantes, les pendus et les configurations d'engloutissement baissier.

- Oscillateur de cupidité – détecte le sentiment haussier via les longues bougies blanches, les marteaux, les engloutissements haussiers et les trois soldats blancs.

La moyenne de ces trois oscillateurs constitue l'Indice d'émotion des chandeliers (CEI). Lorsque le CEI franchit différents seuils, des signaux d'achat ou de vente sont déclenchés, avec confirmation par le volume.

Avantages de la stratégie

- Analyse systématique du sentiment – transformation de l'analyse subjective en indicateurs objectifs via la quantification des configurations de chandeliers.

- Gestion des risques complète – inclut des mécanismes tels que la durée maximale de détention, le take-profit/stop-loss et une période de refroidissement.

- Mécanisme de récupération flexible – en cas de perte sur une transaction, la stratégie tente de récupérer en franchissant le seuil d'équilibre.

- Applicabilité multi-marchés – peut être utilisée sur les actions, le forex, les cryptomonnaies, etc.

- Haute fiabilité des signaux – la confirmation par le volume et la validation par de multiples indicateurs techniques améliorent la précision.

Risques de la stratégie

- Sensibilité aux paramètres – les différents seuils nécessitent des tests et une optimisation approfondis.

- Dépendance à l'environnement de marché – peut générer de faux signaux dans un marché en range.

- Risque de glissement – risque d'exécution sur des marchés à faible liquidité.

- Risque de sur-négociation – une période de refroidissement appropriée est nécessaire pour éviter des transactions trop fréquentes.

- Risque systémique – des pertes importantes peuvent survenir lors d'événements majeurs sur les marchés.

Axes d'optimisation de la stratégie

- Seuils dynamiques – ajustement automatique des seuils en fonction de la volatilité du marché.

- Classification de l'état du marché – ajout de mécanismes d'identification des tendances et des phases de range.

- Optimisation par apprentissage automatique – utilisation d'algorithmes de machine learning pour optimiser les combinaisons de paramètres.

- Renforcement de la gestion des risques – intégration de modules de gestion de capital et de dimensionnement des positions.

- Filtrage des signaux – intégration de davantage d'indicateurs techniques pour filtrer les faux signaux.

Conclusion

Il s'agit d'une stratégie innovante alliant analyse technique et trading quantitatif. Grâce à une analyse systématique du sentiment et une gestion stricte des risques, elle offre aux traders des signaux fiables. Bien qu'il existe des marges d'optimisation, le cadre de base de la stratégie est solide et adapté à un développement et à une application en trading réel.

- 1