Stratégie de retournement de tendance à double momentum basée sur le RSI et le Stochastique RSI

Aperçu

Il s'agit d'une stratégie de trading de retournement de tendance combinant le Relative Strength Index (RSI) et le Stochastic RSI. Cette stratégie capture les points de retournement potentiels en identifiant les conditions de surachat et de survente du marché ainsi que les changements de momentum, afin d'effectuer des transactions. Le cœur de la stratégie utilise le RSI comme indicateur de momentum de base, puis calcule le Stochastic RSI sur cette base pour confirmer davantage la direction du changement de momentum des prix.

Principe de la stratégie

La logique principale de la stratégie comprend les étapes clés suivantes :

- Calculer d'abord la valeur RSI du prix de clôture pour juger de l'état global de surachat/survente.

- Calculer les lignes %K et %D du Stochastic RSI à partir de la valeur RSI.

- Lorsque le RSI se trouve dans la zone de survente (par défaut inférieur à 30) et que la ligne %K du Stochastic RSI croise la ligne %D de bas en haut, un signal d'achat (long) est déclenché.

- Lorsque le RSI se trouve dans la zone de surachat (par défaut supérieur à 70) et que la ligne %K du Stochastic RSI croise la ligne %D de haut en bas, un signal de vente (short) est déclenché.

- Lorsque les conditions RSI opposées se produisent ou que le Stochastic RSI croise en sens inverse, la position est fermée.

Avantages de la stratégie

- Mécanisme de double confirmation – En combinant le RSI et le Stochastic RSI, il permet de réduire efficacement les risques liés aux faux signaux de cassure.

- Paramètres personnalisables – Les paramètres clés tels que la période RSI et les seuils de surachat/survente peuvent être ajustés en fonction des différentes conditions de marché.

- Visualisation dynamique – La stratégie fournit des graphiques en temps réel du RSI et du Stochastic RSI, facilitant le suivi pour le trader.

- Gestion des risques intégrée – Comprend des mécanismes complets de stop-loss et de take-profit.

- Flexibilité – Peut être appliquée sur différentes périodes et dans divers environnements de marché.

Risques de la stratégie

- Risque lié aux marchés oscillants – Dans un marché latéral, des signaux faux fréquents peuvent se produire.

- Risque de retard – En raison de l'utilisation de multiples lissages de moyennes mobiles, les signaux peuvent présenter un certain décalage.

- Sensibilité aux paramètres – Des réglages différents des paramètres peuvent conduire à des résultats de trading sensiblement différents.

- Dépendance à l'environnement de marché – Dans des marchés fortement tendanciels, la stratégie peut manquer certaines opportunités.

- Risque de gestion du capital – Une allocation de position appropriée est nécessaire pour contrôler le risque.

Pistes d'optimisation de la stratégie

- Ajouter un filtre de tendance – On peut ajouter une moyenne mobile à long terme comme filtre de tendance, en n'ouvrant des positions que dans le sens de la tendance.

- Optimiser le mécanisme de stop-loss – On peut introduire un stop-loss dynamique, comme un trailing stop ou un stop-loss basé sur l'ATR.

- Intégrer un indicateur de volume – L'analyse du volume peut améliorer la fiabilité des signaux.

- Ajouter un filtre temporel – On peut éviter les périodes de publication d'actualités importantes ou les créneaux de faible liquidité.

- Développer des paramètres adaptatifs – Ajuster automatiquement les paramètres de la stratégie en fonction de la volatilité du marché.

Résumé

Il s'agit d'une stratégie complète combinant momentum et retournement de tendance, utilisant la synergie du RSI et du Stochastic RSI pour identifier les opportunités de trading potentielles. La stratégie est bien conçue, avec une bonne ajustabilité et adaptabilité. Cependant, dans la pratique, il convient de prêter attention à la sélection de l'environnement de marché et au contrôle des risques. Il est recommandé de procéder à des backtests approfondis et à une optimisation des paramètres avant de passer en trading réel.

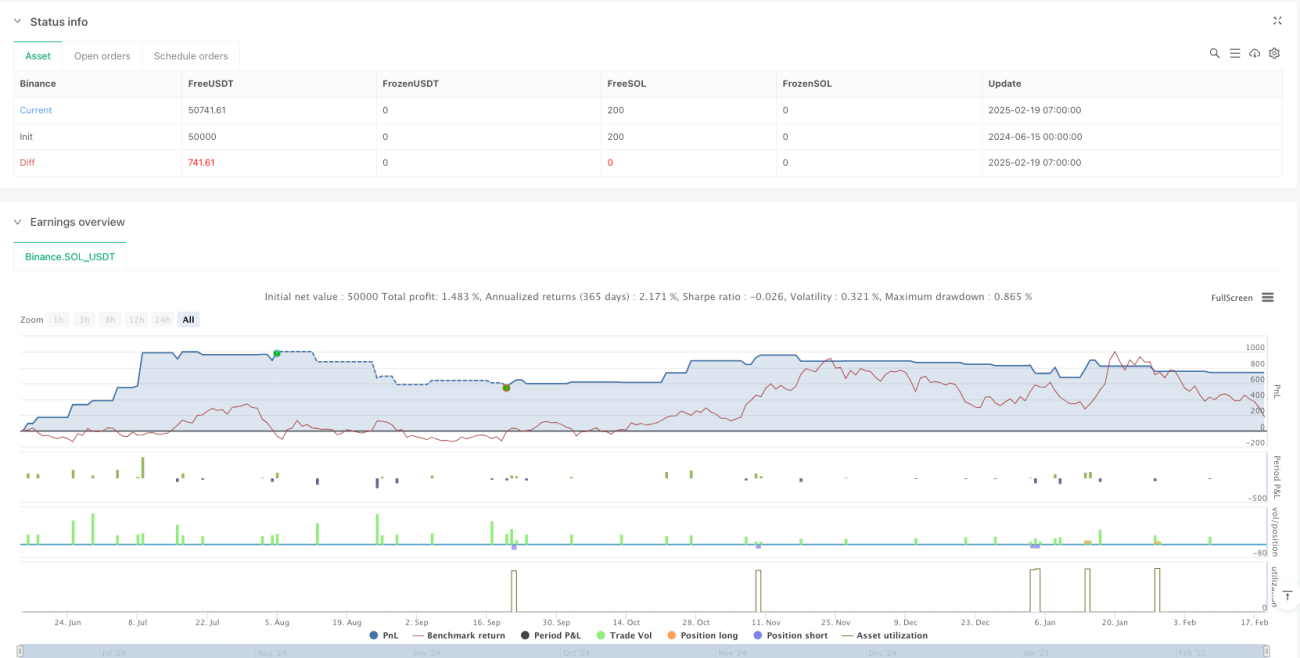

/*backtest

start: 2024-06-15 00:00:00

end: 2025-02-19 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Binance","currency":"SOL_USDT"}]

*/

//@version=5

strategy("RSI + Stochastic RSI Strategy", overlay=true, initial_capital=100000, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// INPUTS- 1