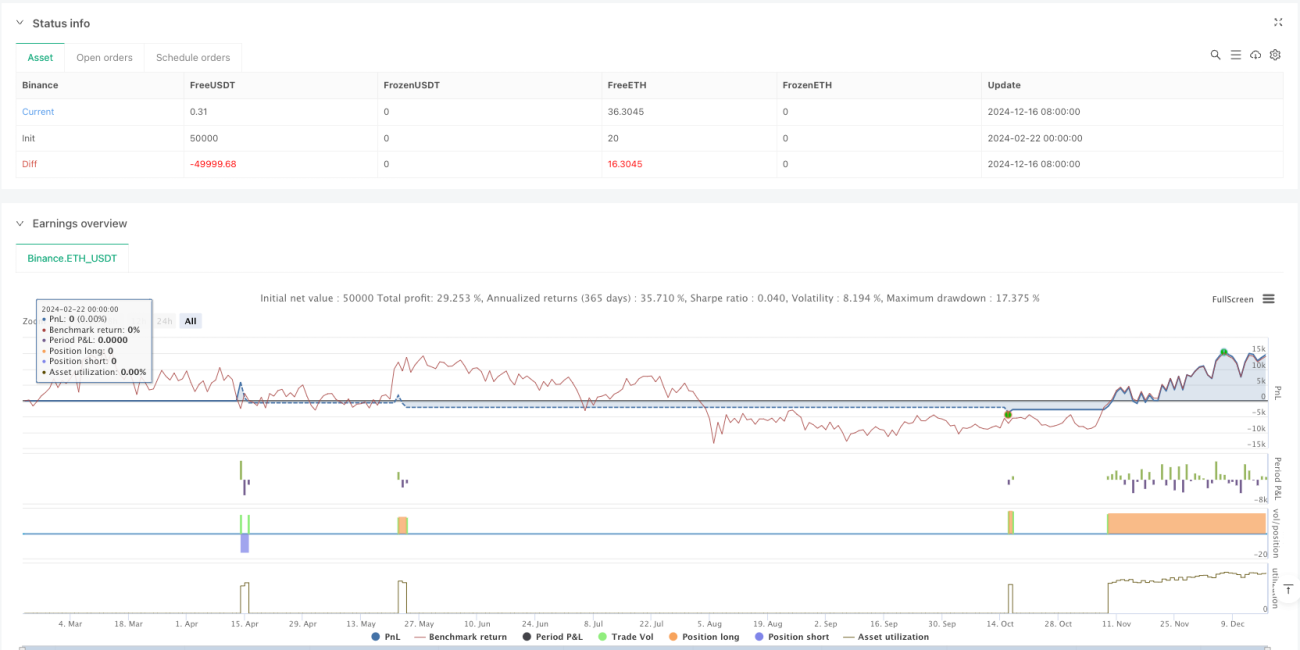

Vue d’ensemble

Cette stratégie de trading quantitatif repose sur un croisement de multiples moyennes mobiles combiné à un filtrage par volume. Elle utilise trois moyennes mobiles de périodes différentes (EMA rapide, EMA lente et SMA de tendance) comme indicateurs principaux, et intègre un filtre de volume pour valider la fiabilité des signaux de trading. La stratégie inclut également des fonctions de stop-loss et de take-profit pour un contrôle efficace des risques.

Principe de la stratégie

La stratégie s’appuie principalement sur les éléments clés suivants :

- Utilisation des moyennes mobiles exponentielles (EMA) sur 9 et 21 périodes pour les croisements, générant des signaux de trading préliminaires.

- Introduction d’une moyenne mobile simple (SMA) sur 50 périodes comme filtre de tendance, garantissant que la direction des transactions reste alignée avec la tendance principale.

- Condition de volume basée sur 1,5 fois le volume moyen sur 20 périodes pour s’assurer d’une activité de trading suffisante.

- Confirmation de la validité des signaux par une amplification du volume lors des cassures de prix.

- Mise en place d’un stop-loss à 1 % et d’un take-profit à 400 % pour optimiser le rapport risque/rendement.

Avantages de la stratégie

- Mécanisme de confirmation multiple : grâce au croisement des moyennes rapide et lente, au filtre de tendance et à la confirmation par volume, la fiabilité des signaux est grandement améliorée.

- Contrôle des risques renforcé : des ratios stop-loss et take-profit judicieux permettent de limiter efficacement le drawdown.

- Bon suivi de tendance : le filtre par moyenne mobile long terme garantit que les transactions sont effectuées dans le sens de la tendance principale.

- Haute qualité des signaux : le filtrage par volume évite les fausses cassures.

- Paramètres flexibles : tous les indicateurs peuvent être optimisés en fonction des caractéristiques des différents marchés.

Risques de la stratégie

- Risque de marché de range : dans un marché latéral, des signaux de trading fréquents peuvent augmenter les coûts de transaction.

- Risque de slippage : en cas de liquidité insuffisante, un slippage important peut survenir.

- Risque de fausse cassure : malgré le filtre de volume, des fausses cassures restent possibles.

- Risque de suroptimisation des paramètres : une optimisation excessive peut conduire au surapprentissage.

- Dépendance aux conditions de marché : la stratégie fonctionne mieux sur les marchés en tendance claire, mais peut être moins performante dans d’autres environnements.

Pistes d’optimisation

- Ajout d’un indicateur de volatilité : intégrer l’ATR pour ajuster dynamiquement le niveau de stop-loss.

- Amélioration du filtre de volume : utiliser un volume relatif plutôt qu’absolu comme condition de filtrage.

- Confirmation de la force de tendance : ajouter des indicateurs comme l’ADX pour valider la vigueur de la tendance.

- Amélioration du mécanisme de take-profit : concevoir un take-profit dynamique pour mieux verrouiller les gains.

- Filtrage temporel : éviter les transactions pendant les périodes de faible volatilité.

Conclusion

Cette stratégie construit un système de trading relativement complet en combinant plusieurs indicateurs techniques. Son principal atout réside dans le mécanisme de confirmation multiple et un contrôle des risques solide. Cependant, elle nécessite une optimisation des paramètres et des ajustements en fonction des conditions réelles du marché. Avec une optimisation et une gestion des risques appropriées, cette stratégie pourrait générer des rendements stables sur les marchés en tendance.

/*backtest

start: 2024-02-22 00:00:00

end: 2024-12-17 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

//@version=5

strategy("Optimized Moving Average Crossover Strategy with Volume Filter", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// Inputs for Moving Averages- 1