Aperçu

La stratégie de trading intelligent pondérée par plusieurs indicateurs est un système de trading quantitatif complet qui génère des décisions de trading en intégrant les signaux de plusieurs indicateurs techniques et en leur attribuant différents poids. Cette stratégie combine plusieurs outils d'analyse technique tels que le MACD, le RSI stochastique, l'EMA, la Super Tendance et le croisement de moyennes mobiles, formant ainsi un cadre de trading global. Le système prend non seulement en charge le take-profit multi-niveaux et le stop-loss dynamique, mais peut également ajuster automatiquement les paramètres de trading en fonction des conditions du marché, ce qui lui confère une grande adaptabilité dans différents environnements de marché. Cette stratégie convient particulièrement aux traders de moyen et long terme, et grâce à son système de pondération, elle rend les décisions de trading plus robustes et fiables.

Principe de la stratégie

Le cœur de cette stratégie réside dans son système de signaux pondérés, qui génère des signaux de trading via cinq sous-stratégies distinctes :

-

Stratégie MACD : Utilise le croisement de la ligne MACD et de la ligne de signal pour déterminer la direction de la tendance du marché. Un signal d'achat est généré lorsque la ligne MACD passe au-dessus de la ligne de signal, et un signal de vente lorsqu'elle passe en dessous.

-

Stratégie RSI stochastique : Combine les avantages du RSI et de l'indicateur stochastique pour surveiller les conditions de surachat et de survente du marché. Un signal d'achat est généré lorsque le RSI stochastique est inférieur au seuil de survente défini, et un signal de vente lorsqu'il dépasse le seuil de surachat.

-

Stratégie EMA surachat/survente : Utilise l'EMA pour identifier le degré d'écart du prix par rapport à sa moyenne. Un signal d'achat est généré lorsque le RSI est inférieur au seuil de survente défini, et un signal de vente lorsqu'il dépasse le seuil de surachat.

-

Stratégie Super Tendance : Définit un canal de prix basé sur un multiple de l'ATR et détermine la direction du trading en fonction des changements de tendance. Un signal d'achat est généré lorsque la Super Tendance passe de négative à positive, et un signal de vente lorsqu'elle passe de positive à négative.

-

Stratégie de croisement de moyennes mobiles : Utilise le croisement de deux moyennes mobiles de périodes différentes pour déterminer la tendance du marché. Un signal d'achat est généré lorsque la moyenne mobile court terme passe au-dessus de la moyenne mobile long terme, et un signal de vente lorsqu'elle passe en dessous.

La stratégie calcule les signaux de chaque sous-stratégie via un système de pondération personnalisable, et ne déclenche une transaction que lorsque la somme pondérée dépasse le seuil défini. De plus, la stratégie intègre un mécanisme d'identification des pics et des creux potentiels, permettant d'ajuster les positions en cas de retournement probable du marché.

Ce mécanisme de confirmation multi-niveaux des signaux réduit efficacement les faux signaux et améliore la fiabilité du système de trading, tandis que des paramètres flexibles permettent à la stratégie de s'adapter à différents instruments de trading et périodes de temps.

Avantages de la stratégie

-

Confirmation multiple des signaux : Le calcul pondéré des signaux générés par cinq indicateurs techniques indépendants réduit les erreurs potentielles d'un seul indicateur et améliore la qualité et la fiabilité des signaux de trading.

-

Système de pondération adaptatif : Chaque sous-stratégie peut se voir attribuer des poids différents, permettant au trader d'ajuster l'accent de la stratégie en fonction de sa confiance et des performances historiques de chaque indicateur, ce qui augmente la flexibilité de la stratégie.

-

Gestion des risques complète : La stratégie intègre des mécanismes de contrôle des risques à plusieurs niveaux, y compris le stop-loss, le take-profit multi-niveaux et l'ajustement dynamique du stop-loss, garantissant un contrôle rapide des risques en cas de mouvements défavorables du marché.

-

Identification automatisée des pics et creux potentiels : Grâce à une analyse combinée du RSI, du volume de transactions et de l'évolution des prix, la stratégie peut identifier les sommets et les creux potentiels du marché et clôturer partiellement les positions au moment opportun pour verrouiller les profits ou réduire les pertes.

-

Haut degré de personnalisation : Presque tous les paramètres peuvent être ajustés, y compris les périodes de calcul des indicateurs, les valeurs de pondération, les pourcentages de take-profit et de stop-loss, etc., permettant au trader d'optimiser la stratégie en fonction de son style personnel et des différentes conditions du marché.

-

Mécanisme de retard intégré : Pour éviter d'entrer trop tôt dans une transaction ou de trader sur la base de signaux de bruit, la stratégie utilise un mécanisme de confirmation différée, garantissant que seuls des signaux persistants déclenchent des transactions, réduisant ainsi l'impact des fluctuations à court terme.

-

Fonction de filtrage temporel : La stratégie permet de définir les dates de début et de fin du trading, permettant au trader de tester les performances sur des périodes spécifiques à l'aide de données historiques, ou d'éviter les périodes de volatilité anormale connues.

Risques de la stratégie

-

Risque de suroptimisation des paramètres : En raison du grand nombre de paramètres, il existe un risque de surajustement aux données historiques, ce qui peut entraîner de mauvaises performances en trading réel. La solution consiste à effectuer des tests sur plusieurs périodes de temps et instruments, en utilisant des réglages de paramètres relativement robustes, en évitant une optimisation excessive pour des données historiques spécifiques.

-

Risque de changement des conditions de marché : Les performances de la stratégie peuvent différer entre un marché en tendance et un marché de range, et un changement soudain des conditions du marché peut réduire son efficacité. La solution consiste à introduire un mécanisme d'identification de l'environnement de marché, en ajustant les paramètres ou en suspendant le trading en fonction de l'état du marché.

-

Risque de conflit de signaux : L'utilisation simultanée de plusieurs indicateurs peut produire des signaux contradictoires, entraînant une confusion dans les décisions. La solution consiste à définir des poids appropriés pour chaque indicateur, en mettant l'accent sur les indicateurs les plus fiables et en veillant à ce que le seuil de signal soit raisonnable pour réduire la probabilité de conflits.

-

Risque de mauvaise gestion de capital : Bien que la stratégie inclue un mécanisme de stop-loss, une gestion de capital inappropriée peut encore entraîner un épuisement rapide des fonds. La solution consiste à contrôler strictement le pourcentage de capital alloué à chaque transaction, en veillant à ce que le risque maximal par transaction reste dans des limites acceptables.

-

Risque de défaillance technique : Les systèmes de trading automatisés peuvent rencontrer des problèmes techniques tels que des interruptions de réseau ou des retards de données. La solution consiste à mettre en place un mécanisme d'intervention manuelle, à surveiller régulièrement l'état de fonctionnement du système et à traiter rapidement les anomalies.

Directions d'optimisation de la stratégie

-

Ajout d'un filtre d'environnement de marché : Développer un indicateur capable d'identifier si le marché est en tendance ou en range, et ajuster dynamiquement les poids des sous-stratégies en fonction de l'état du marché. Renforcer les stratégies de suivi de tendance en marché de tendance et renforcer les stratégies oscillantes en marché de range.

-

Introduction de l'optimisation par apprentissage automatique : Utiliser des techniques d'apprentissage automatique pour ajuster automatiquement les paramètres et les poids de chaque indicateur, permettant à la stratégie d'apprendre et de s'adapter en continu en fonction des données de marché les plus récentes, améliorant ainsi sa capacité d'adaptation dynamique.

-

Ajout de l'analyse du volume de transactions : Utiliser les changements de volume comme signal de confirmation supplémentaire, n'exécuter les transactions qu'avec un support de volume conforme aux attentes, augmentant ainsi la crédibilité des signaux.

-

Optimisation de l'algorithme d'identification des pics et creux potentiels : Améliorer la logique actuelle d'identification des pics et creux en ajoutant davantage de facteurs de confirmation, tels que les formations de prix, la confirmation multi-périodes, etc., afin d'améliorer la précision de l'identification.

-

Ajout d'indicateurs de sentiment : Intégrer des indicateurs de sentiment du marché, tels que l'indice de peur (VIX), le ratio put/call, etc., pour ajuster la stratégie ou suspendre le trading en cas de sentiment extrême, évitant ainsi de trop trader pendant les périodes de forte volatilité.

-

Développement d'un mécanisme de take-profit et stop-loss dynamique : Ajuster automatiquement les niveaux de take-profit et stop-loss en fonction de la volatilité du marché. Élargir la plage de stop-loss en période de forte volatilité et la resserrer en période de faible volatilité, rendant la gestion des risques plus flexible et efficace.

-

Optimisation des périodes de temps : Ajouter une fonction d'analyse multi-périodes, exigeant que des périodes de temps supérieures et inférieures confirment simultanément les signaux, réduisant ainsi les faux dépassements et les faux signaux.

Résumé

La stratégie de trading intelligent pondérée par plusieurs indicateurs construit un système de trading complet et flexible en intégrant plusieurs outils d'analyse technique et en leur attribuant différents poids. Cette stratégie bénéficie non seulement d'une confirmation multiple des signaux, d'un système de pondération adaptatif et d'une gestion complète des risques, mais également d'un mécanisme automatisé d'identification des pics et creux potentiels, lui conférant une forte adaptabilité dans des environnements de marché complexes et changeants.

Bien qu'il existe des risques potentiels tels que la suroptimisation des paramètres, les changements de conditions de marché et les conflits de signaux, ceux-ci peuvent être efficacement contrôlés grâce à un réglage raisonnable des paramètres, une identification de l'environnement de marché et une gestion stricte du capital. Les futures directions d'optimisation incluent l'ajout d'un filtre d'environnement de marché, l'introduction de techniques d'apprentissage automatique, le renforcement de l'analyse du volume de transactions et l'optimisation de l'algorithme d'identification des pics et creux. Ces améliorations renforceront encore la stabilité et la rentabilité de la stratégie.

Pour les investisseurs cherchant une méthode de trading systématique, cette stratégie offre un cadre intéressant à considérer. Elle permet non seulement de réduire l'influence des émotions sur les décisions de trading, mais aussi d'optimiser en continu les performances de trading grâce à une approche basée sur les données. Lors de la mise en œuvre de cette stratégie, il est recommandé de commencer avec des paramètres conservateurs, de les ajuster progressivement et de surveiller attentivement les performances, afin de trouver la configuration la mieux adaptée à sa tolérance au risque personnelle et aux conditions du marché.

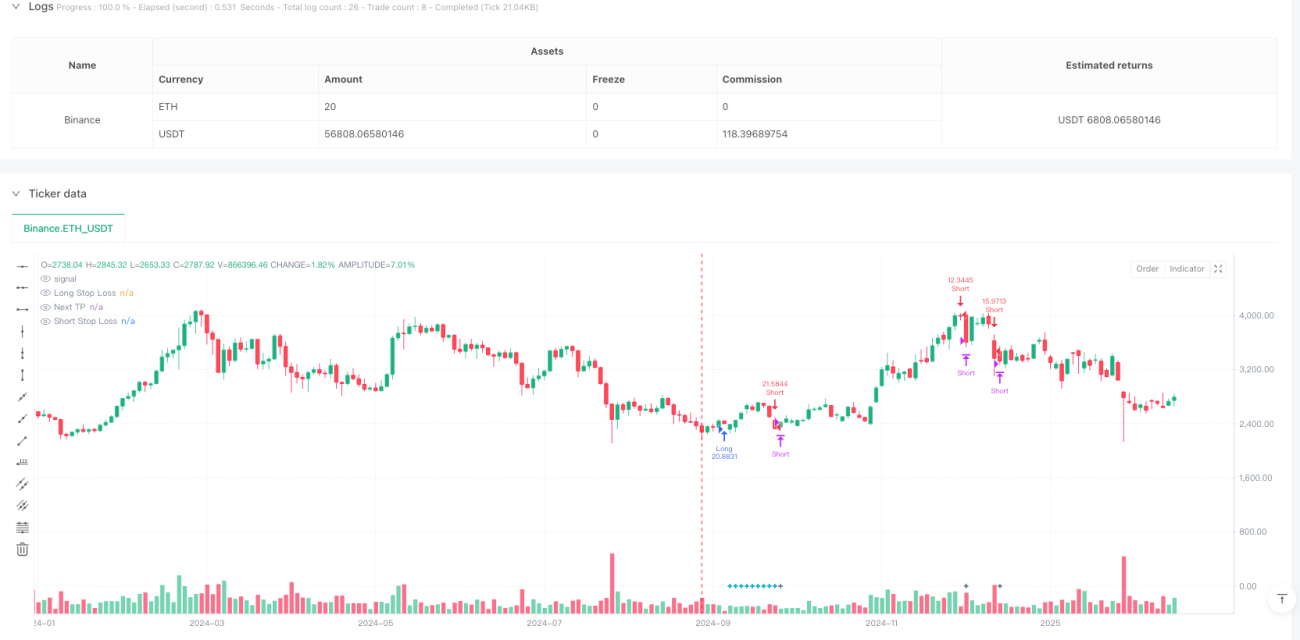

/*backtest

start: 2024-09-08 00:00:00

end: 2025-02-23 08:00:00

period: 2d

basePeriod: 2d

exchanges: [{"eid":"Binance","currency":"ETH_USDT"}]

*/

// **********************************************************************************************************************************************************************************************************************************************************************

// Last update: 08/03/2022

// *************************************************************************************************************************************************************************************************************************************************************************

//@version=5- 1