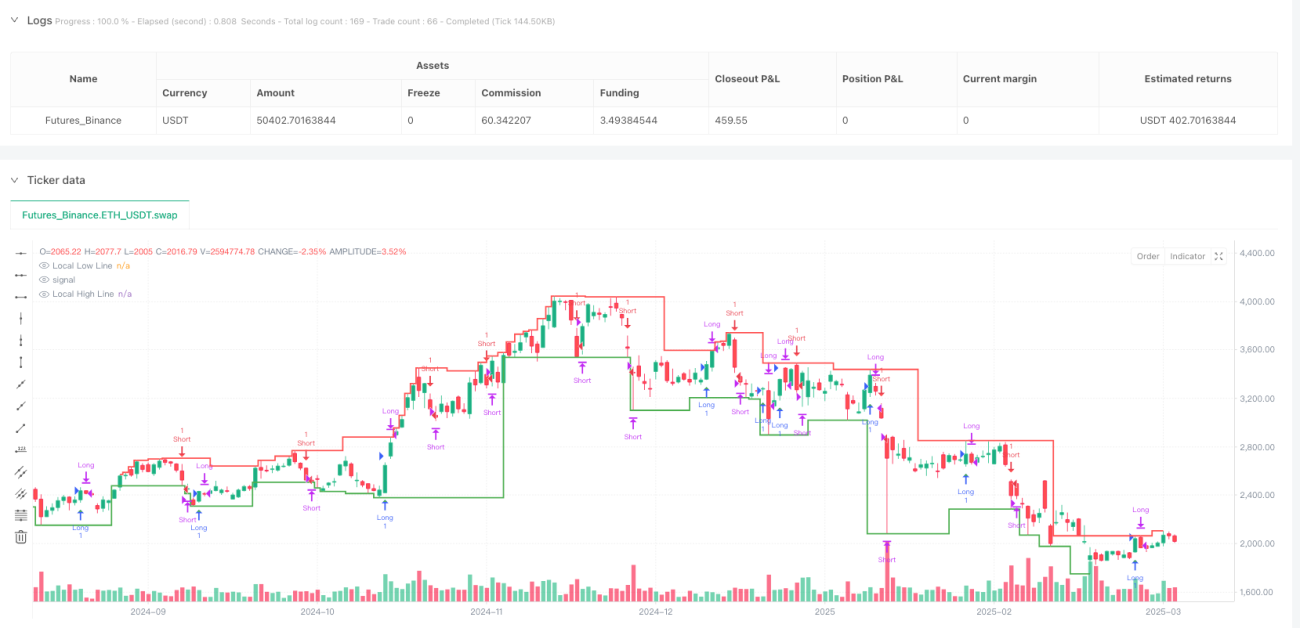

Aperçu

Cette stratégie de trading innovante combine l'analyse des zones de liquidité et la dynamique de la structure du marché interne afin d'identifier des points d'entrée à haute probabilité. En suivant les interactions entre le prix et les niveaux clés du marché, et en utilisant les renversements du marché interne comme déclencheurs, elle offre aux traders une méthode d'entrée flexible et précise sur le marché.

Principe de la stratégie

La logique centrale de la stratégie repose sur deux composants clés : l'identification des zones de liquidité et le renversement du marché interne. Les zones de liquidité sont déterminées dynamiquement en analysant les plus hauts et plus bas locaux, tandis que le renversement du marché interne se base sur le franchissement par le prix des niveaux haussiers ou baissiers précédents pour juger le changement de direction du marché.

La stratégie présente les caractéristiques principales suivantes :

- Logique de renversement du marché interne : ne dépend pas des figures de chandeliers traditionnelles, mais se base sur le franchissement de niveaux clés par le prix.

- Suivi des zones de liquidité : identifie dynamiquement les zones de liquidité clés pour éviter de trader dans des conditions de marché faibles.

- Flexibilité des modes : propose trois modes de trading : « Les deux », « Haussier uniquement » et « Baissier uniquement ».

- Gestion des risques : permet de personnaliser les niveaux de stop loss et de take profit.

- Contrôle de la période temporelle : permet de contrôler précisément les créneaux de trading.

Avantages de la stratégie

- Adaptabilité dynamique : la stratégie réagit rapidement aux changements de structure du marché.

- Entrée précise : en combinant zones de liquidité et renversement du marché interne, elle améliore la précision d'entrée.

- Risque maîtrisé : intègre des mécanismes de stop loss et de take profit.

- Grande flexibilité : permet de choisir le mode de trading selon les conditions du marché.

- Analyse multidimensionnelle : prend en compte simultanément le comportement des prix, la liquidité et la structure du marché.

Risques de la stratégie

- Une volatilité excessive du marché peut déclencher le stop loss.

- Dans un marché en range, des signaux fréquents peuvent augmenter les coûts de transaction.

- Un paramétrage inapproprié peut affecter les performances de la stratégie.

- Les résultats des backtests peuvent différer du trading réel.

Axes d'optimisation de la stratégie

- Introduire des algorithmes d'apprentissage automatique pour une optimisation adaptative des paramètres.

- Ajouter davantage de filtres, tels que le volume des transactions ou des indicateurs de volatilité.

- Développer un mécanisme de validation multi-timeframes.

- Optimiser les algorithmes de stop loss et de take profit en prenant en compte l'ajustement dynamique de la volatilité du marché.

Résumé

Il s'agit d'une stratégie de trading innovante qui fusionne l'analyse de la liquidité et la dynamique de la structure du marché. Grâce à une logique flexible de renversement du marché interne et un suivi précis des zones de liquidité, elle offre aux traders un outil de trading puissant. Sa clé réside dans son adaptabilité et sa capacité d'analyse multidimensionnelle, lui permettant de maintenir une efficacité d'exécution élevée dans différentes conditions de marché.

- 1