Stratégie quantitative de divergence dynamique du RSI

Aperçu

La stratégie quantitative de divergence à double pivot RSI est une approche avancée qui identifie les opportunités de retournement potentielles en détectant les divergences haussières et baissières classiques entre l'action des prix et l'indice de force relative (RSI). Cette stratégie utilise un algorithme automatisé de détection des points pivots, combiné à deux méthodes différentes de gestion du stop-loss et du take-profit, et ouvre automatiquement des positions lors de la confirmation des signaux de divergence. Le cœur de la stratégie réside dans la validation mathématique précise des divergences entre les prix et l'indicateur RSI, ainsi que dans un mécanisme de gestion dynamique des risques garantissant que chaque transaction respecte un ratio risque/récompense prédéfini.

Principe de la stratégie

- Module de calcul du RSI : utilise la méthode de lissage de Wilder pour calculer le RSI sur 14 périodes (ajustable) avec le prix de clôture comme source d'entrée par défaut (configurable).

- Détection des points pivots :

- Utilise une fenêtre glissante de 5 périodes (ajustable) à gauche et à droite pour détecter les hauts et bas locaux de l'indicateur RSI.

- Garantit, via la fonction

ta.barssince, un intervalle de 5 à 60 chandeliers (plage ajustable) entre les points pivots.

- Logique de confirmation de divergence :

- Divergence haussière : le prix atteint un nouveau plus bas tandis que le RSI forme un plus bas plus élevé.

- Divergence baissière : le prix atteint un nouveau plus haut tandis que le RSI forme un plus haut plus bas.

- Système d'exécution des transactions :

- Mécanisme de stop-loss à double mode : basé sur le point de swing des 20 dernières périodes (ajustable) ou sur l'amplitude de volatilité ATR.

- Calcul dynamique du take-profit : basé sur le montant du risque multiplié par le ratio risque/récompense prédéfini (par défaut 2:1).

- Système de visualisation : marque tous les signaux de divergence valides sur le graphique et affiche en temps réel les niveaux de stop-loss (rouge) et de take-profit (vert) pour la position en cours.

Analyse des avantages

- Mécanisme de validation multidimensionnelle : exige que les prix et le RSI satisfassent simultanément une configuration spécifique, avec un intervalle de temps compris dans une plage prédéfinie, réduisant ainsi considérablement la probabilité de faux signaux.

- Gestion adaptative des risques :

- Le mode points de swing convient aux marchés en tendance, capturant efficacement les mouvements de vagues.

- Le mode ATR convient aux marchés en range, ajustant automatiquement l'amplitude du stop-loss en fonction de la volatilité.

- Paramètres hautement configurables : tous les paramètres clés (période RSI, plage de détection des pivots, ratio risque/récompense, etc.) peuvent être ajustés en fonction des caractéristiques du marché.

- Gestion scientifique du capital : utilise par défaut une allocation de 10 % par position, évitant une exposition excessive au risque sur une seule transaction.

- Retour visuel en temps réel : grâce aux marquages sur le graphique et aux lignes dynamiques de stop-loss/take-profit, fournit un support de décision de trading intuitif.

Analyse des risques

- Risque de retard : le RSI étant un indicateur retardé, il peut générer des signaux différés lors de mouvements unilatéraux violents. Solution : combiner avec un filtre de tendance ou réduire la période du RSI.

- Risque de marché en range : peut produire une série de faux signaux en l'absence de tendance claire. Solution : activer le mode ATR avec un multiplicateur plus élevé, ou ajouter un filtre de volatilité.

- Risque de surapprentissage des paramètres : certaines combinaisons de paramètres peuvent bien fonctionner sur les données historiques mais échouer en trading réel. Solution : effectuer des tests de résistance sur plusieurs périodes et instruments.

- Risque de conditions extrêmes : les gaps de prix peuvent entraîner l'échec du stop-loss. Solution : éviter de trader avant/après les événements économiques majeurs, ou utiliser des options de couverture.

- Dépendance à l'égard de l'unité de temps : les performances varient considérablement selon les unités de temps. Solution : effectuer un backtesting approfondi et une optimisation sur l'unité de temps cible.

Axes d'optimisation

- Validation par indicateurs composites : ajouter le MACD ou le volume comme confirmation secondaire pour améliorer la qualité des signaux.

- Ajustement dynamique des paramètres : adapter automatiquement la période RSI et le multiplicateur ATR en fonction de la volatilité du marché.

- Optimisation par apprentissage automatique : utiliser des algorithmes génétiques pour optimiser les combinaisons de paramètres clés.

- Analyse multi-unités de temps : intégrer un filtre de direction de tendance provenant d'une unité de temps supérieure.

- Gestion dynamique de la taille des positions : ajuster la taille des positions en fonction de la volatilité pour équilibrer le risque.

- Filtre d'événements : intégrer les données du calendrier économique pour éviter de trader avant/après la publication de données importantes.

Résumé

La stratégie quantitative de divergence à double pivot RSI propose une approche structurée du trading de retournement grâce à une identification systématique des divergences et une gestion rigoureuse des risques. Sa valeur fondamentale réside dans la traduction des concepts d'analyse technique traditionnelle en règles de trading quantifiables, et dans l'adaptation aux différentes conditions de marché via un mécanisme de stop-loss à double mode. Pour que la stratégie performe, trois éléments clés sont nécessaires : une optimisation appropriée des paramètres, un contrôle strict des risques et une discipline d'exécution cohérente. Cette stratégie convient particulièrement aux environnements de marché présentant une certaine volatilité mais sans tendance extrême, et constitue un excellent modèle pour les traders intermédiaires souhaitant passer au trading quantitatif.

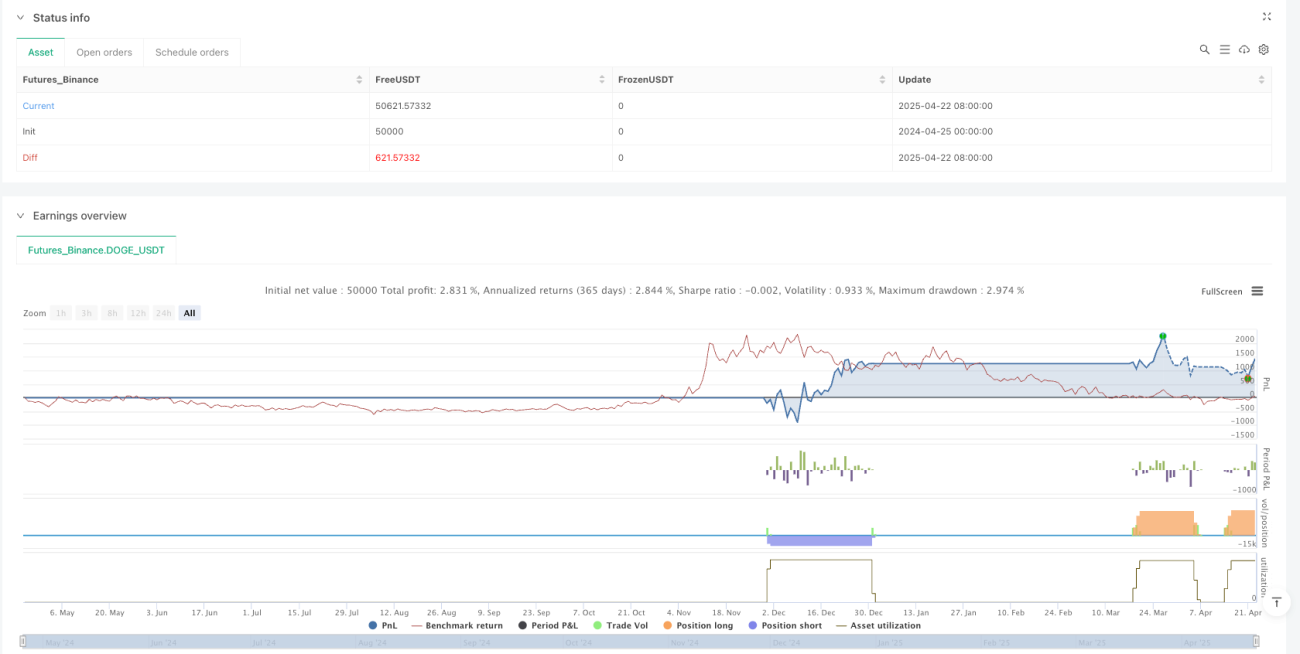

/*backtest

start: 2024-04-25 00:00:00

end: 2025-04-23 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"DOGE_USDT"}]

*/

//@version=6

strategy("RSI Divergence Strategy - AliferCrypto", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// === RSI Settings ===- 1