Aperçu

La stratégie de trading quantitatif basée sur la rupture de la fourchette d’ouverture à deux périodes avec stop suiveur est un système de trading par cassure exploitant la fourchette de prix formée pendant les 15 premières minutes suivant les ouvertures des sessions de Londres et de New York. En capturant l’élan initial des prix au début de ces deux grandes places financières, la stratégie entre dans une position longue ou courte lorsque le prix franchit le haut ou le bas de la fourchette des 15 premières minutes. Son élément central est un mécanisme de stop suiveur qui protège les profits tout en permettant à ceux-ci de croître. La stratégie propose également un filtre optionnel basé sur une moyenne mobile pour améliorer la qualité des transactions.

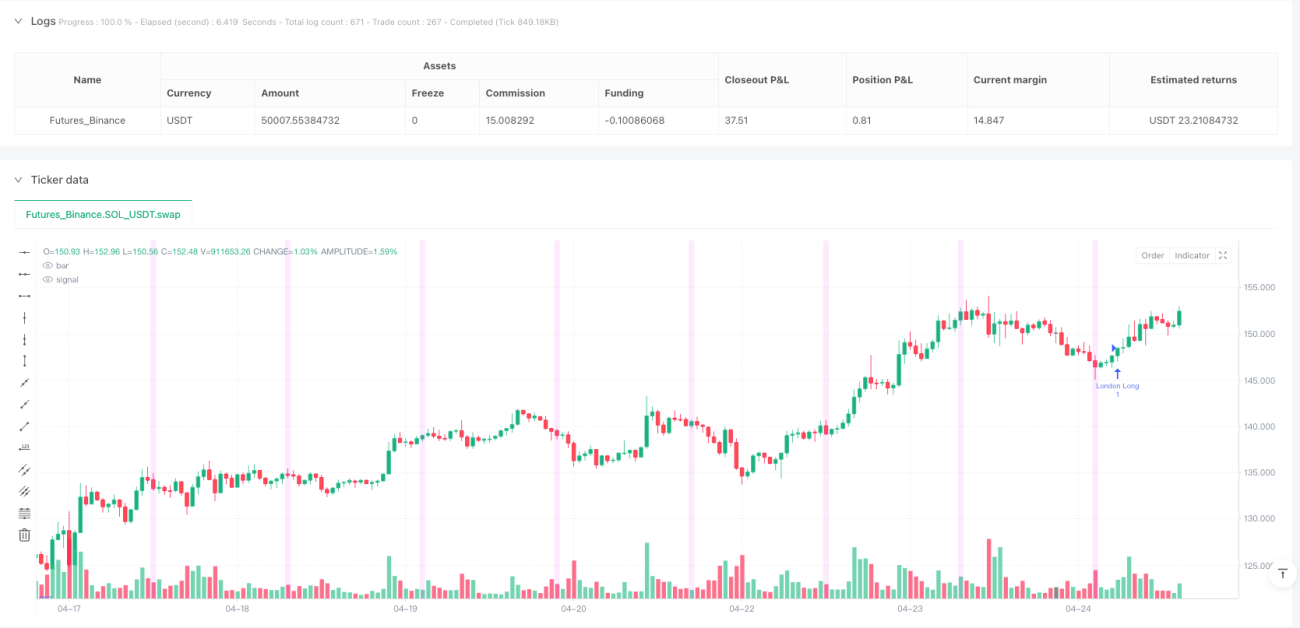

Principes de la stratégie

Le fonctionnement de la stratégie s’articule autour de deux fenêtres temporelles clés : l’ouverture du marché de Londres (3h00-3h15, heure de New York) et l’ouverture du marché de New York (9h30-9h45, heure de New York). Le processus est le suivant :

- Enregistrer respectivement le plus haut et le plus bas des 15 premières minutes des sessions de Londres et de New York, formant ainsi une « fourchette de prix ».

- Une fois la fourchette formée, la stratégie vérifie que sa taille répond à un minimum requis (par défaut 2 points).

- Si le prix franchit à la hausse le haut de la fourchette, et que la condition de filtre EMA (si activée) est satisfaite, ouvrir une position longue.

- Si le prix franchit à la baisse le bas de la fourchette, et que la condition de filtre EMA (si activée) est satisfaite, ouvrir une position courte.

- Le stop loss est placé à une distance égale à la hauteur de la fourchette au-delà de la limite opposée à la direction de la cassure.

- Le take profit cible un rapport risque/rendement (par défaut 2,0) multiplié par la hauteur de la fourchette.

- Un stop suiveur est également défini, par défaut de 8 ticks, et s’ajuste à mesure que le prix évolue favorablement.

La logique clé consiste à capter les cassures directionnelles en début de session, qui annoncent souvent une tendance ultérieure. Grâce au stop suiveur, la stratégie protège les gains tout en laisser courir les transactions gagnantes.

Avantages de la stratégie

Après une analyse approfondie, la stratégie présente les avantages suivants :

- Opportunités sur deux périodes : En surveillant les ouvertures de Londres et de New York, elle capte la volatilité des deux principales sessions, multipliant les occasions.

- Stop suiveur : Contrairement à un take profit fixe, le stop suiveur protège les profits tout en permettant aux positions gagnantes de continuer à évoluer, améliorant ainsi le gain moyen.

- Contrôle des risques robuste : Le stop loss dynamique basé sur la volatilité (taille de la fourchette) adapte la gestion du risque aux conditions du marché.

- Grande personnalisation : L’utilisateur peut ajuster le rapport risque/rendement, la taille minimale de la fourchette, les ticks du stop suiveur et l’activation du filtre EMA, pour s’adapter à différents instruments et profils de risque.

- Filtre par indicateur technique : Le filtre EMA optionnel sur 5 minutes aide à éviter les trades à contre-tendance, améliorant la qualité des signaux.

- Une seule transaction par période : Un drapeau intégré limite les entrées à un trade maximum par session, évitant les frais et les risques liés aux transactions excessives.

Risques de la stratégie

Bien que bien conçue, la stratégie comporte les risques potentiels suivants :

- Fausses cassures : Le prix peut franchir brièvement la fourchette puis revenir, déclenchant un stop. Pour atténuer ce risque, on pourrait ajouter une confirmation, par exemple exiger que le prix reste au-delà du seuil pendant un certain temps ou atteigne un certain dépassement avant d’ouvrir.

- Gestion de la taille des positions : La stratégie utilise par défaut un nombre fixe de contrats, ce qui peut ne pas convenir à tous les capitaux. Il est conseillé d’ajuster la taille en fonction du capital et de la tolérance au risque.

- Risque de suroptimisation des paramètres : Une optimisation excessive peut conduire à un overfitting, avec des performances médiocres dans des conditions futures. Il faut tester la robustesse des paramètres.

- Dépendance aux conditions de marché : Dans un marché sans tendance ou range, la stratégie peut générer de nombreux stops. On pourrait ajouter un filtre de conditions de marché.

- Problème de fuseau horaire : Le code utilise le fuseau horaire de New York. Il faut s’assurer qu’il correspond à celui de la plateforme de trading, sous peine de décalage des signaux.

- Impact des jours fériés : Les jours spéciaux et fériés peuvent affecter les performances ; la stratégie n’inclut pas de filtre pour les exclure.

Pistes d’optimisation

Sur la base de l’analyse, voici quelques pistes d’amélioration :

- Ajouter une confirmation : Intégrer des conditions supplémentaires après la cassure (volume, nombre de bougies restant dans la direction) pour réduire les pertes sur fausses cassures.

- Gestion dynamique des positions : Ajuster la taille en fonction de la volatilité et du capital pour optimiser le rapport risque/rendement.

- Filtre de conditions de marché : Introduire un indicateur de volatilité ou de force de tendance pour suspendre les trades dans des environnements défavorables aux cassures.

- Confirmation multi-timeframe : Utiliser une tendance de plus longue durée pour ne trader que dans le sens de cette tendance.

- Optimisation du point d’entrée : Entrer sur un retrait vers un niveau de support/résistance clé plutôt que directement à la cassure, pour obtenir un meilleur prix.

- Filtre temporel : Analyser les performances historiques par jour de la semaine et heure, pour éviter les périodes peu profitables.

- Analyse de corrélation multi-instruments : Éviter de détenir simultanément plusieurs positions fortement corrélées.

Résumé

La stratégie de trading quantitatif basée sur la rupture de la fourchette d’ouverture à deux périodes avec stop suiveur est un système de cassure conçu pour les ouvertures des sessions de Londres et de New York. En capturant l’élan directionnel en début de session et en utilisant un stop suiveur, elle maximise le potentiel de profit tout en contrôlant le risque. Bien qu’elle soit exposée aux fausses cassures et à la dépendance aux conditions de marché, une paramétrisation judicieuse et des filtres supplémentaires peuvent améliorer sa stabilité et sa rentabilité. Cette stratégie convient particulièrement aux marchés liquides et volatils. Les traders doivent l’adapter à leur tolérance au risque et à leurs objectifs.

/*backtest

start: 2024-04-27 00:00:00

end: 2025-04-25 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"SOL_USDT"}]

*/

//@version=6

strategy("ORB-LD-NY-Trail Strategy", overlay=true,

default_qty_type=strategy.fixed, default_qty_value=1,

calc_on_order_fills=true, calc_on_every_tick=true)- 1