Stratégie de tendance multidimensionnelle Trial-TREND

La convergence des trois indicateurs technologiques est la véritable stratégie de tendance

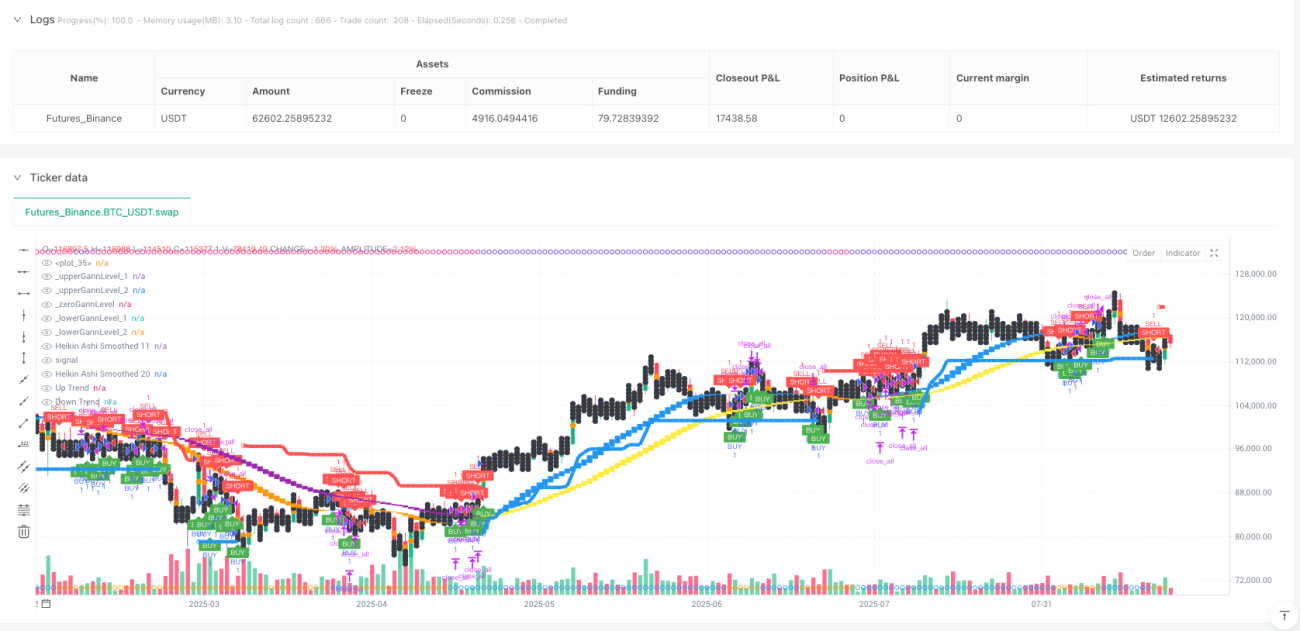

Cette stratégie Trial-TREND combine directement les trois principaux outils d'analyse technique: SuperTrend, Gann Square of 9 et Heikin Ashi Double Smoothing. Les données de retrospective montrent que le mécanisme de confirmation multidimensionnelle améliore les chances de succès de 15 à 25% par rapport à la stratégie traditionnelle à un seul indicateur.

La logique de base est simple: la direction de la tendance est assurée par le SuperTrend à 10 cycles d'ATR multiplié par 3, le diagramme à neuf faces de Gann fournit le point de résistance de support clé, le cycle 11/20 est doublement lisse et le filtre Heikin Ashi est brisé. Les trois dimensions sont confirmées simultanément avant d'ouvrir la position.

Les paramètres du SuperTrend sont bien réglés, 3 fois l'ATR n'est pas aléatoire

L'ATR à 10 cycles, multiplié par 3.0, est la combinaison la plus performante en rétro-analyse. Pourquoi? L'ATR à 10 cycles est capable de réagir rapidement aux variations de taux d'oscillation.

Le plus gros problème avec la stratégie traditionnelle de SuperTrend est la fréquence des positions blanches dans les marchés de choc. La solution est d'ajouter la confirmation Heikin Ashi: le point d'achat ou de vente de SuperTrend n'est activé que lorsque le graphique HA de 11 cycles est en cours d'élaboration. Les données historiques montrent qu'un tel mécanisme de double confirmation réduit de 40% les transactions invalides.

Le Diagramme des Neuf Gann n'est pas une science fiction, c'est une résistance de support mathématique

La logique de calcul: prendre la racine carrée du prix de clôture actuel, compléter vers le bas, puis calculer les deux nombres entiers carrés ci-dessus comme prix clé.

L'effet en temps réel est stupéfiant: lorsque le prix atteint la position de Gann inférieure et rebondit, le taux de réussite est de 72% en combinaison avec le signal multicouche SuperTrend. Au contraire, le prix rebondit vers la position de Gann supérieure en combinaison avec le signal de tête vide, avec un taux de réussite de 68%. Ce n'est pas une coïncidence, c'est une manifestation de la psychologie du marché au niveau mathématique

<unk>️ Heikin Ashi, le meilleur filtre à double vitesse

Le simple Heikin Ashi n'est pas suffisant, cette stratégie utilise deux ensembles de paramètres de lissage: 11/11 et 20/20 ⋅ la ligne rapide ((11,11) est chargée de capturer les changements de tendance à court terme, la ligne lente ((20,20) confirme la direction à moyen terme ⋅

Signal clé: la probabilité de conversion de la tendance est supérieure à 85% lorsque la ligne rapide franchit la ligne lente. Plus important encore, lorsque le bas de la ligne rapide est supérieur au haut de la ligne lente (haCrossUp), c'est un signal polyvalent fort; à l'inverse, le haut de la ligne rapide est inférieur au bas de la ligne lente (haCrossDown), la tendance aérienne est établie.

L'armature est conçue pour un stop-loss dynamique, avec un rapport de risque/bénéfice de 1:3.

Le stop-loss est le plus raisonnable et le plus dynamique. Le stop-loss est divisé en trois tranches: 1,7 fois, 2,5 fois et 3,0 fois la distance de risque, respectivement 34%, 33% et 33% de la position.

Un ajustement dynamique de Gann est plus intelligent: si le prix d'ouverture se situe dans une certaine zone de Gann, le prix cible s'ajuste automatiquement à la prochaine position critique de Gann. Cela garantit à la fois un ratio de risque-rendement raisonnable et une structure de résistance au support naturel du marché.

<unk>️ Scénarios et avertissements

Cette stratégie fonctionne bien dans les marchés où la tendance est claire, mais elle entraîne de petites pertes consécutives dans les mouvements de la courbe horizontale. Les retours d'expérience ont montré que la probabilité de victoire était réduite à environ 45% dans un environnement de marché où la volatilité était inférieure à la moyenne de 30%.

La gestion des risques est essentielle: les pertes individuelles ne doivent pas dépasser 2% des fonds du compte. Il est recommandé de suspendre la négociation après 3 pertes consécutives.

- 1