Stratégie de sortie retardée : l’art d’attendre avant de partir

🎯 Que fait exactement cette stratégie ?

Vous savez quoi ? La plupart des traders ont un défaut : dès qu'ils voient un signal défavorable, ils fuient immédiatement ! 😱 Mais cette stratégie fait exactement le contraire : elle vous dit : « Patience, attends encore un peu ! »

C'est comme dans une relation amoureuse : tu romps dès que l'autre dit un mot de colère ? Trop impulsif ! Cette stratégie attend 3 bougies (ajustables) pour voir si c'est vraiment une rupture, ou juste une réaction émotionnelle.

📊 Logique centrale : ne pas prendre de décisions impulsives

Conditions d'entrée :

- Détection d'un motif de rupture de haut/bas (Higher Low / Lower High)

- Confirmation par la bougie (clôture dans la bonne direction)

- Système de notation multidimensionnel : momentum RSI + confirmation de volume + analyse de volatilité

- Score minimum de 3,0 pour entrer (sur 5,0 maximum)

Point clé ! Le système de notation ici est super intelligent, il prend en compte :

- La force de la bougie (proportion du corps réel)

- Si le volume est en hausse

- Si le RSI se situe dans une zone raisonnable

- Le niveau actuel de volatilité

⏰ La sagesse de la sortie différée

Stratégie traditionnelle : signal d'échec → sortie immédiate

Cette stratégie : signal d'échec → attendre 3 bougies → reconfirmation → sortie rationnelle

Pourquoi différer ?

- Éviter les pièges de faux cassures : le marché fait souvent le mort ; le délai filtre le bruit

- Réduire les transactions fréquentes : diminuer les coûts de commission

- Améliorer le taux de réussite : donner plus de temps à la tendance pour se développer

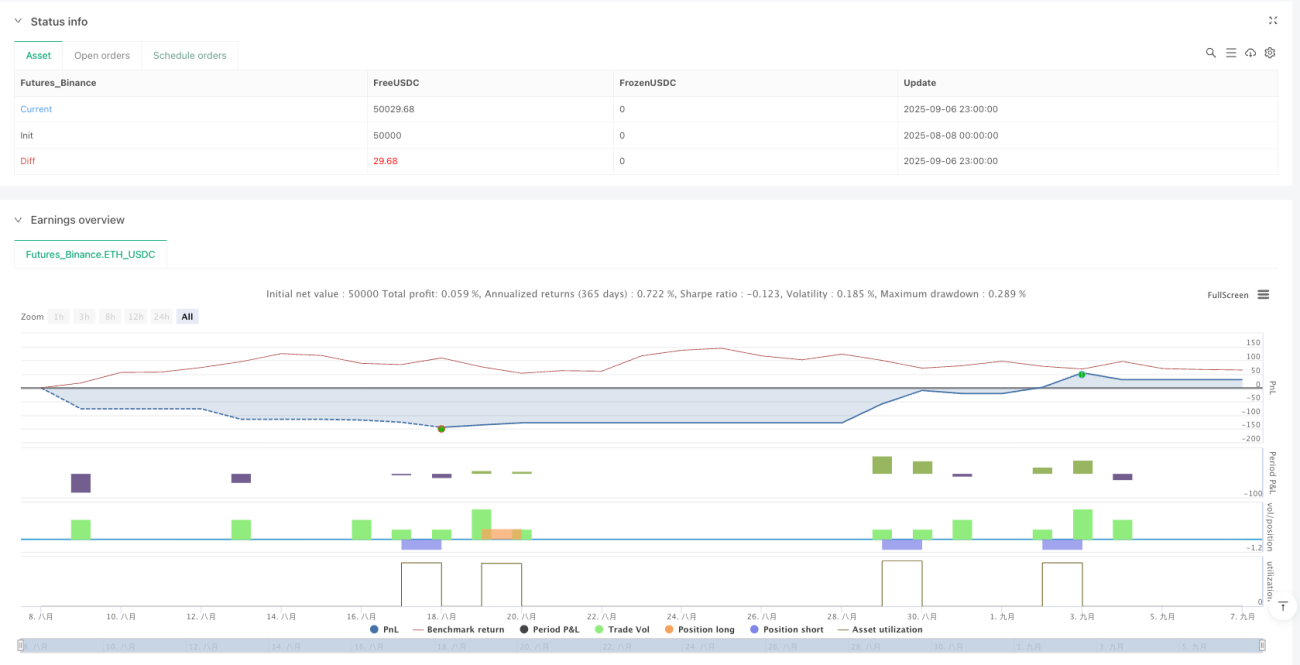

🛡️ Gestion des risques : stricte quand il le faut

Bien que la sortie soit « zen », le contrôle des risques est absolument rigoureux :

- Stop loss : 1,5 fois l'ATR (ajustable)

- Take profit : 2,5 fois l'ATR (ajustable)

- Horaires de trading : uniquement pendant les heures de trading américaines

- Clôture en fin de séance : aucune position conservée overnight

🎨 Conception visuelle : clair et net

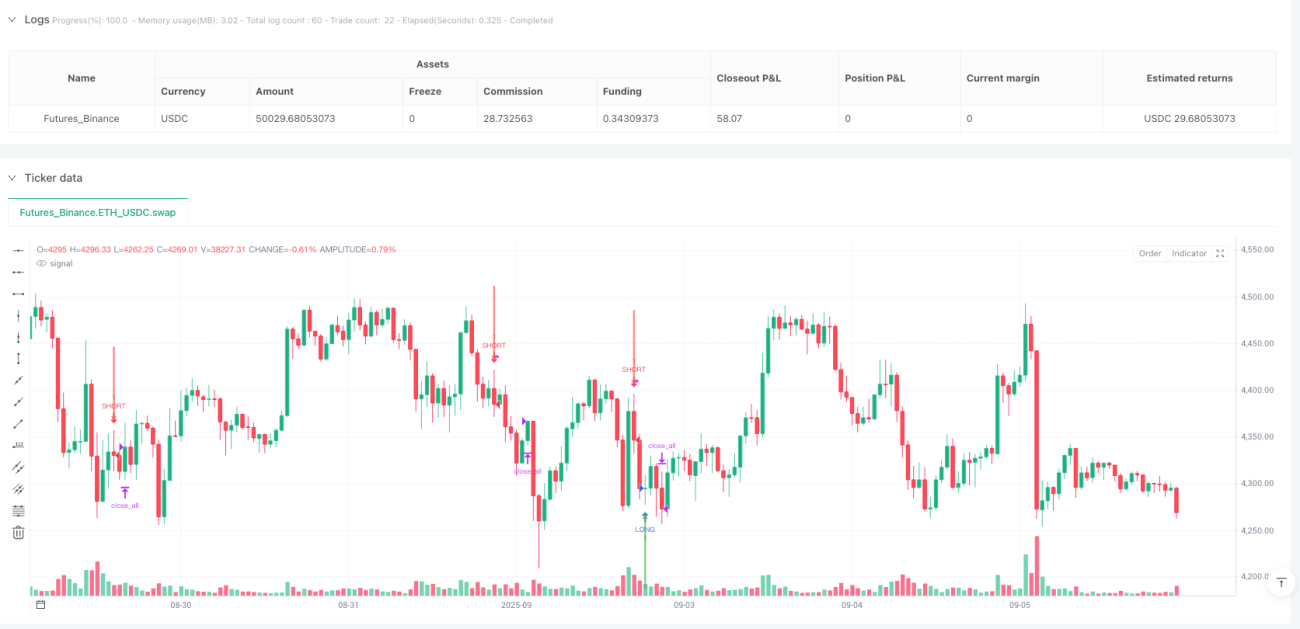

- 🟢 Triangle vert : signal long normal

- 🔴 Triangle rouge : signal short normal

- 🏁 Drapeau : signal de haute qualité (score ≥ 4,5)

- 🟠 X orange : signal d'échec précoce (ignoré)

- 🔴 X rouge : signal d'échec différé (exécution de la sortie)

Guide anti-piège : ne paniquez pas quand un X orange apparaît, c'est une « fausse alerte » que la stratégie ignore délibérément !

💡 Scénarios d'application

Cette stratégie est particulièrement adaptée à :

- Capturer les retournements dans un marché range

- Les traders qui ne supportent pas d'être constamment stoppés

- Les investisseurs qui souhaitent améliorer la qualité des signaux

- Les amateurs de day trading sur actions américaines

Rappelez-vous : la patience est la plus grande arme du trader. Parfois, « attendre avant de partir » est plus sage que « agir immédiatement » ! 🚀

- 1