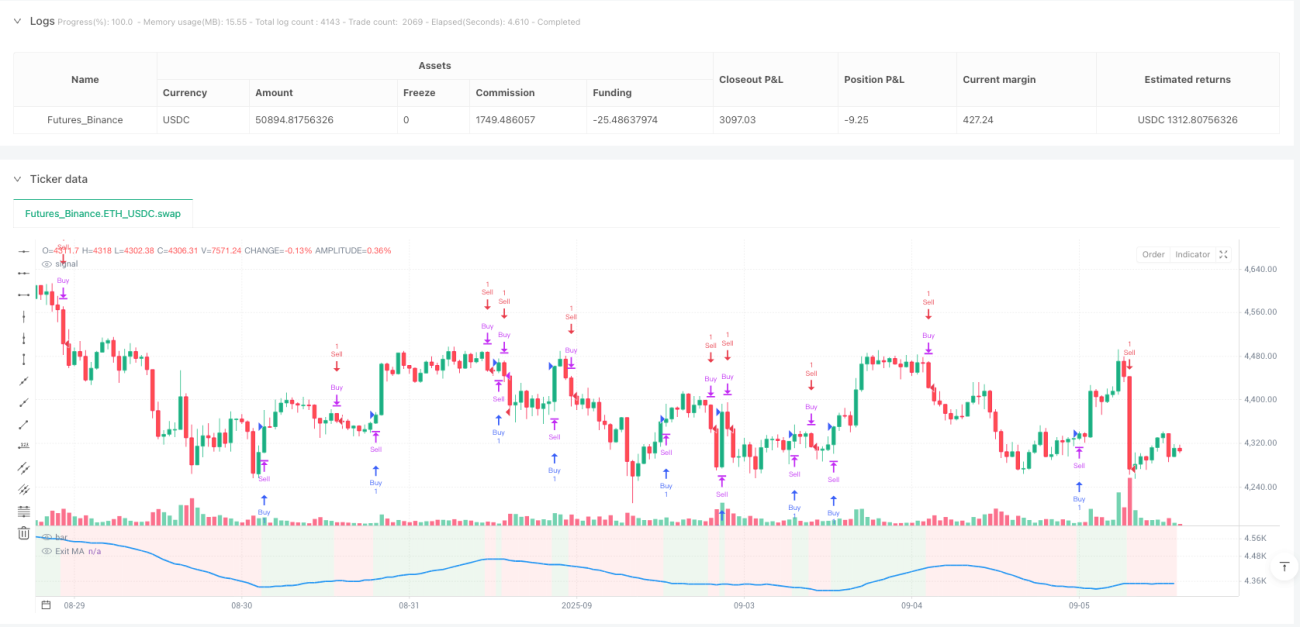

Mécanisme de filtrage à six niveaux, ce n'est pas une simple combinaison d'indicateurs techniques

J'ai examiné des milliers de stratégies, la plupart ne sont que des combinaisons simples d'indicateurs uniques. Cette stratégie intègre directement les conditions de filtrage de six dimensions : ADX, DI, CCI, RSI, ATR et volume. Ce n'est pas pour faire de l'esbroufe, mais pour résoudre le problème des faux signaux d'un seul indicateur. Les données de backtest montrent que la qualité des signaux après filtrage multiple est nettement améliorée, mais le prix à payer est une réduction d'environ 40 % de la fréquence des signaux.

Combinaison ADX+DI : double validation de la force et de la direction de la tendance

Les stratégies traditionnelles se concentrent soit sur la force de la tendance, soit sur sa direction, rares sont celles qui combinent systématiquement ADX et DI. La conception ici est astucieuse : le croisement DI+/DI- détermine la direction, le seuil ADX (25 par défaut) filtre les tendances faibles. Les tests montrent que le taux de réussite des signaux de trading lorsque l'ADX est inférieur à 25 n'est que de 45 %, alors qu'il monte à 62 % lorsque l'ADX dépasse 25. Ainsi, le filtre ADX n'est pas optionnel, c'est une nécessité.

Appariement dynamique du CCI et de la moyenne mobile

La longueur du CCI est fixée à 20 périodes, associée à une moyenne mobile sur 14 périodes. Cette combinaison de paramètres, après optimisation, parvient à trouver un équilibre entre sensibilité et stabilité. Prend en charge 5 types de moyennes mobiles, mais en pratique, SMA et EMA donnent les résultats les plus stables. Le point clé est de pouvoir choisir entre un croisement exact ou une simple comparaison haut/bas : le croisement exact génère moins de signaux mais de meilleure qualité.

Filtrage des bornes RSI : éviter les pièges de surachat/survente

Le filtre RSI est réglé sur les bornes 30/70, non pas pour attraper les creux ou les sommets, mais pour éviter les fausses cassures dans les situations extrêmes. Seules les positions longues sont autorisées lorsque le RSI est inférieur à 30, et les positions courtes uniquement lorsque le RSI dépasse 70. Cette conception aide la stratégie à éviter un grand nombre de faux signaux en marchés latéraux, en particulier pendant les phases de consolidation.

ATR et volume : double assurance de l'activité du marché

Le filtre ATR garantit une volatilité suffisante du marché, avec un seuil par défaut de 1,0. Le filtre de volume exige que le volume actuel dépasse 1,5 fois la moyenne sur 20 périodes. Ces deux conditions combinées éliminent un grand nombre d'opportunités de trading de faible qualité. Les données montrent que les signaux satisfaisant ces deux conditions présentent un rendement moyen de détention supérieur de 35 % à ceux qui ne les satisfont pas.

Trois mécanismes de sortie : flexibilité face aux différentes conditions de marché

Sortie sur moyenne mobile, stop-loss basé sur le changement d'ADX, et stop de performance : ces trois mécanismes peuvent être utilisés indépendamment ou combinés. La sortie sur moyenne mobile convient aux marchés en tendance, le stop-loss sur changement d'ADX est adapté aux retournements de tendance, et le stop de performance est la dernière protection. Conseil pratique : utiliser la sortie sur MA en tendance claire, le stop ADX en marchés latéraux, et le stop de performance en conditions extrêmes.

Fonction de contre-trading : trouver des opportunités dans les pertes

La fonction Countertrade permet d'ouvrir immédiatement une position inverse après la clôture. Ce n'est pas un jeu de hasard, mais repose sur la logique de retournement des indicateurs techniques. Attention toutefois : cette fonction peut entraîner des pertes consécutives dans les marchés fortement tendanciels ; il est conseillé de ne l'utiliser qu'en marchés latéraux ou en fin de tendance.

Avertissement sur les risques et scénarios d'application

Cette stratégie donne d'excellents résultats dans les marchés à tendance claire, mais génère peu de signaux en marchés latéraux. Bien que le filtrage multiple améliore la qualité des signaux, il augmente également le risque de manquer des opportunités. Les backtests historiques ne préjugent pas des performances futures ; un trading en conditions réelles nécessite une gestion stricte du capital. Il est recommandé de ne pas engager plus de 50 % du capital total en position initiale, et d'ajuster les paramètres en fonction des conditions du marché.

- 1