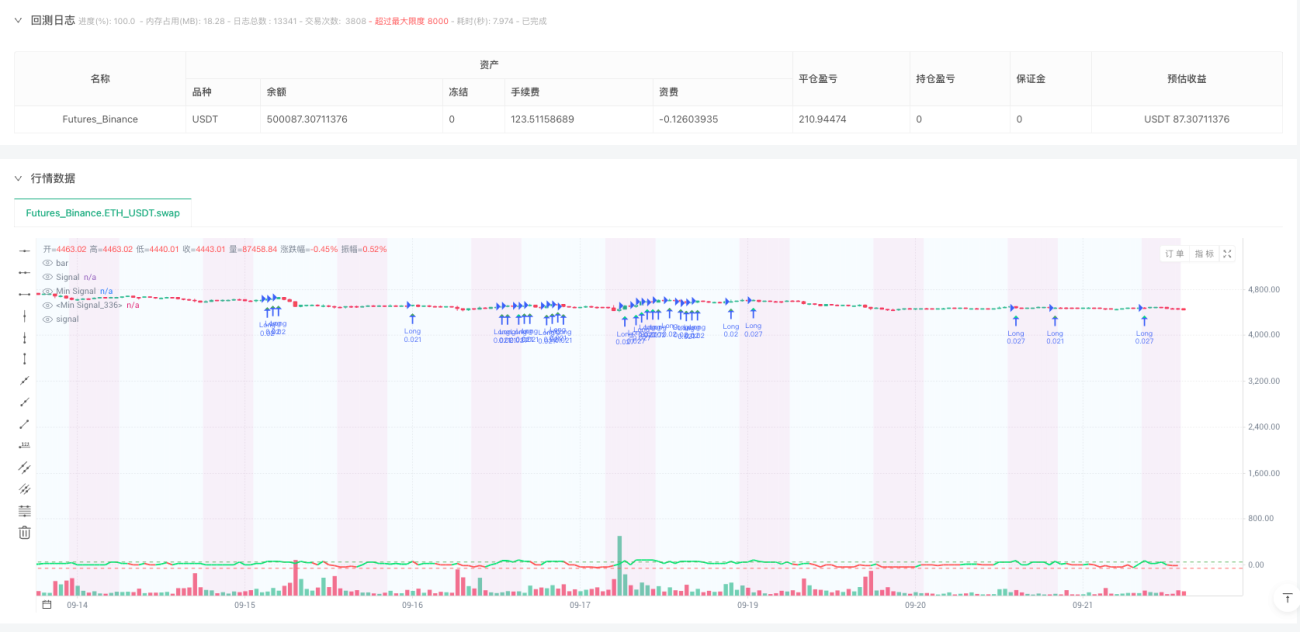

🎯 Cœur de la stratégie : cibler l'argent intelligent du marché du week-end

Le saviez-vous ? Pendant que les grands noms de Wall Street sont en week-end, le marché des cryptomonnaies recèle des opportunités cachées ! Cette stratégie agit comme un gardien de nuit, ramassant les opportunités lorsque les investisseurs institutionnels sont "hors service".

À retenir ! Cette stratégie ne trade que le samedi et le dimanche, en particulier pendant la période UTC 0h-8h le dimanche. Pourquoi ? Parce que la liquidité est alors relativement faible, ce qui rend l'analyse technique plus efficace, un peu comme il est plus facile d'entendre des bruits subtils dans une bibliothèque silencieuse.

📊 Fusion d'indicateurs multiples : pas de travail en solitaire

Cette stratégie rassemble une équipe de super-héros :

- RSI (période 8) : capture rapidement les signaux de surachat/survente

- MACD (8,17,9) : confirme la dynamique de tendance

- Bandes de Bollinger (20,2.5) : identifie les zones de prix extrêmes

- Divergence CVD : détecte les véritables intentions de l'argent intelligent

Guide anti-erreur : Un seul indicateur, c'est comme regarder un film seul – on se laisse facilement tromper par l'intrigue. La confirmation multi-indicateurs, c'est comme regarder avec des amis – on entend différents points de vue !

💰 Gestion intelligente du capital : 500 $ suffisent

La partie la plus intéressante arrive ! Ce système est conçu pour les petits capitaux :

- Minimum 120 $ par trade : pas de mise en jeu totale

- Maximum 4 positions simultanées : diversification des risques, pas tous les œufs dans le même panier

- Effet de levier dynamique de 5x à 20x : ajustement automatique selon la volatilité du marché

Comme au volant, on peut accélérer sur autoroute mais ralentir dans les ruelles. Le système ajuste la taille des positions en fonction des caractéristiques de risque de chaque crypto.

🛡️ Contrôle des risques : plus vigilant que votre mère

Mécanisme de triple protection :

- Perte journalière max 5 % : trop perdu aujourd'hui ? On recommence demain.

- Perte maximale du week-end 15 % : même si le week-end est agité, une limite existe.

- Arrêt après 4 pertes consécutives : éviter les trades émotionnels.

Système de freinage d'urgence : si le compte perd plus de 30 %, tous les trades sont immédiatement arrêtés. C'est comme le système ABS d'une voiture, crucial en cas d'urgence !

- 1