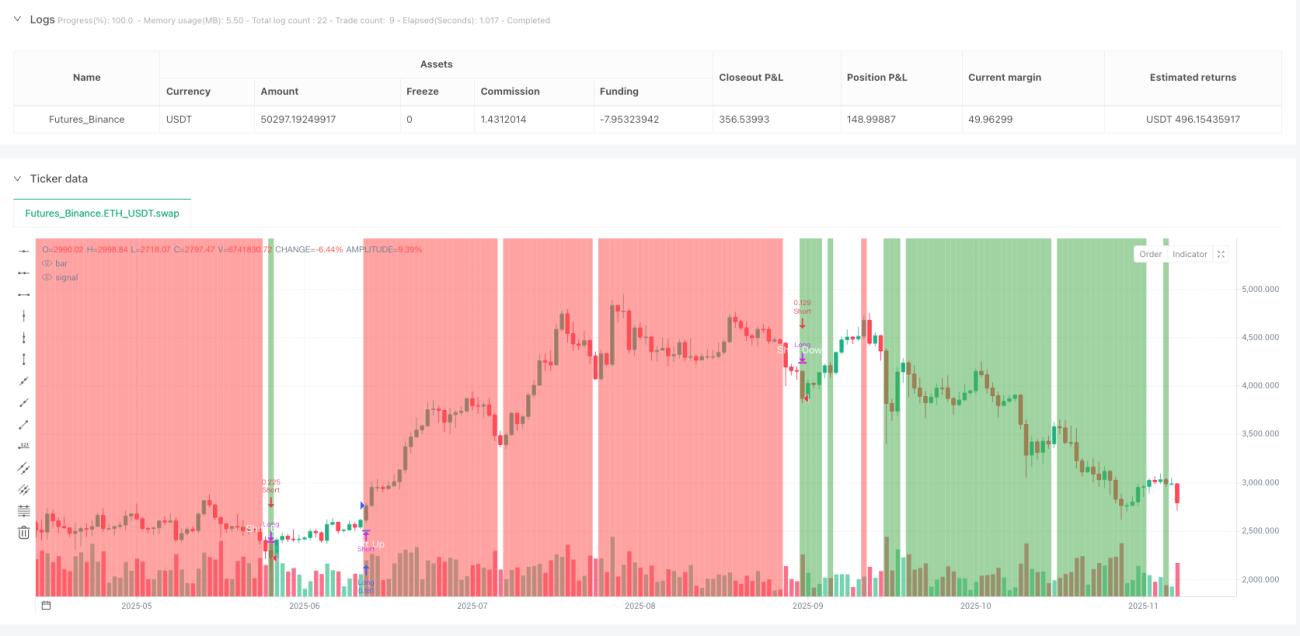

Trendshift Stratégie de retournement de tendance

🎯 Que fait exactement cette stratégie ?

Savez-vous quoi ? Cette stratégie est comme un « détecteur d'humeur » du marché ! 📊 Elle capture spécifiquement ces points de retournement clés qui prennent les petits investisseurs au dépourvu. Imaginez si vous pouviez savoir à l'avance quand le prix d'une action va « changer de visage », n'est-ce pas comme avoir un superpouvoir pour trader ?

Le cœur de cette stratégie est super simple : lorsque le prix franchit un sommet ou un creux important, la structure du marché change. C'est comme quand vous grimpez une montagne et que vous découvrez soudain que la route devient une descente – le changement de tendance se produit souvent en un instant !

🔍 Points clés ! Trois mécanismes fondamentaux

1. Système d'identification des points d'oscillation 🎢

La stratégie identifie automatiquement les sommets et les creux importants sur une période passée, comme si elle dessinait les « pics » et les « vallées » du marché. Lorsque le prix franchit ces niveaux clés, c'est un signal que la tendance pourrait changer !

2. Filtre ATR 📏

Il y a un concept très intelligent ici ! La stratégie ne se laisse pas berner par de petits mouvements – il faut que le franchissement atteigne un certain multiple de l'ATR pour être valide. C'est comme fixer un « seuil minimum » pour filtrer les faux breakouts.

3. Cadre de prime/décote 💎

Le plus intéressant arrive ! La stratégie divise la fourchette de prix en zones « bon marché » et « chères ». Acheter dans la zone bon marché, vendre dans la zone chère – n'est-ce pas la règle d'or de l'investissement ?

🚀 Quels sont les avantages pratiques ?

Guide anti-piège n°1 : Dites adieu au FOMO (peur de manquer) ! Cette stratégie entre en position dès le premier instant du retournement de tendance, vous plaçant du côté de l'« argent intelligent » plutôt que d'être le « repreneur » qui achète au sommet.

Guide anti-piège n°2 : Gestion des risques super intuitive ! Vous pouvez calculer automatiquement la taille de la position en fonction du ratio de votre compte, et également définir un stop-loss basé sur la fourchette, pour dormir sur vos deux oreilles.

Guide anti-piège n°3 : Visualisation géniale ! Les points de retournement sont automatiquement marqués sur le graphique, et l'arrière-plan change de couleur pour indiquer si on est en zone bon marché ou chère – tout est clair d'un coup d'œil !

💡 À quel type de trader cela convient-il ?

Si vous êtes le genre de trader qui aime « acheter bas et vendre haut » mais qui a toujours du mal à trouver le bon timing, cette stratégie est faite sur mesure pour vous ! Elle convient particulièrement aux traders de moyen et long terme, car elle se concentre sur les changements fondamentaux de la structure du marché, et non sur le bruit à court terme.

Rappelez-vous : la meilleure stratégie n'est pas de trader tous les jours, mais de faire la bonne chose au bon moment ! 🎯

- 1