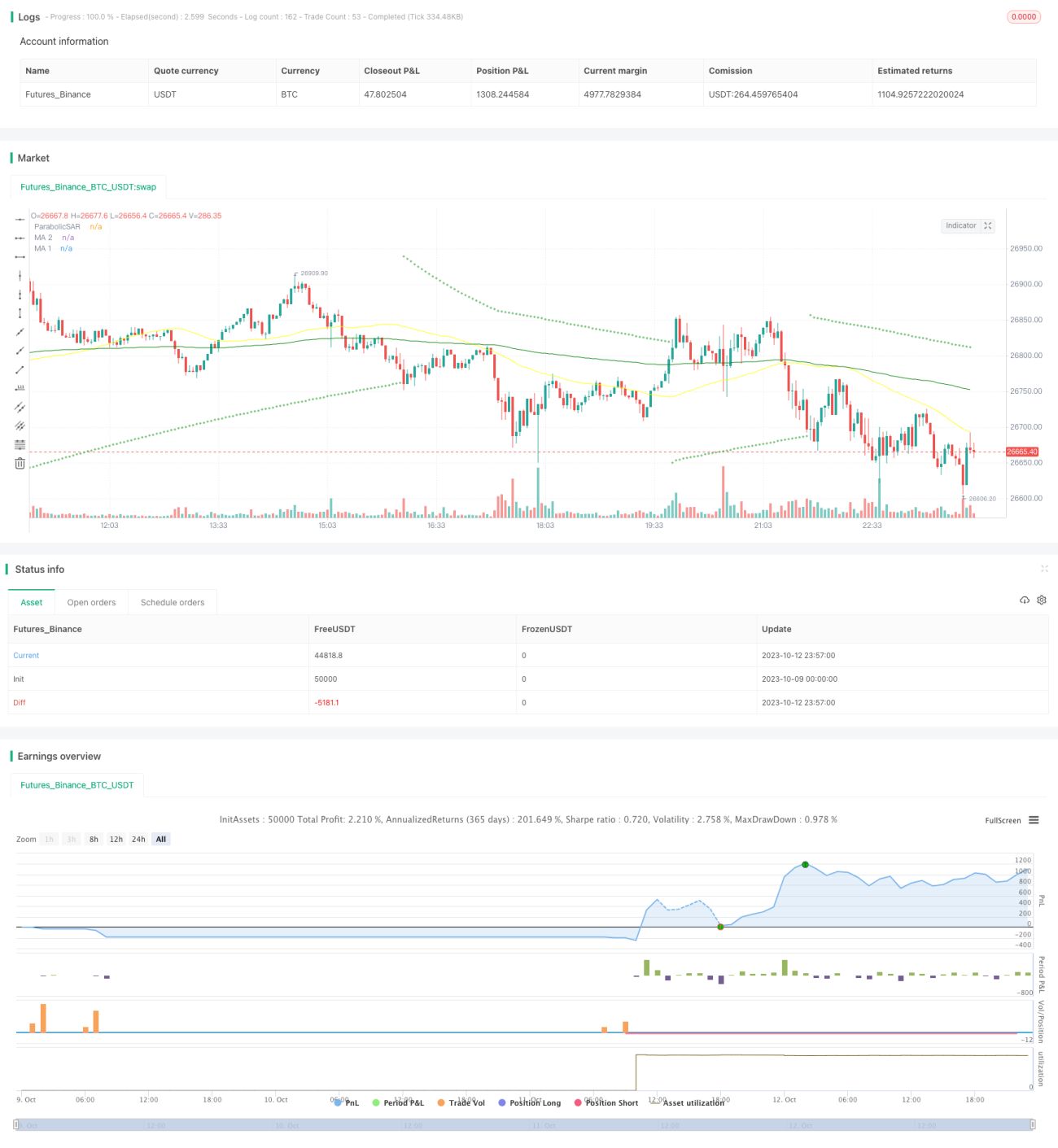

प्रवृत्ति अनुसरण चार तत्व रणनीति

अवलोकन

यह रणनीति SAR संकेतक, RSI संकेतक, VOL संकेतक और MA मूविंग एवरेज जैसे चार तत्वों का उपयोग करके प्रवृत्ति की पहचान करती है और मजबूत जोखिम प्रबंधन उपायों के साथ प्रवृत्ति का अनुसरण करके लाभ कमाती है। रणनीति में SAR संकेतक मुख्य भूमिका निभाता है, जिसमें RSI ओवरबॉट/ओवरसोल सीमाओं की मदद से उलटफेर के संकेतों की पहचान की जाती है, VOL संकेतक वॉल्यूम विशेषताओं का निर्धारण करता है, और MA मूविंग एवरेज मुख्य एवं गौण प्रवृत्तियों की दिशा का आकलन करता है। कई संकेतकों के संयोजन से झूठे संकेतों को फ़िल्टर किया जा सकता है और वास्तविक प्रवृत्ति दिशा की पहचान की जा सकती है। जोखिम प्रबंधन में स्टॉप-लॉस और टेक-प्रॉफिट सेट किए जाते हैं, जो एकल व्यापार में होने वाले नुकसान और संचित लाभ को प्रभावी ढंग से नियंत्रित करते हैं। यह रणनीति मध्यम से दीर्घकालिक धारकों के लिए उपयुक्त है, जो मुख्यधारा की प्रवृत्ति के अनुरूप स्थिर रिटर्न प्राप्त कर सकते हैं।

रणनीति सिद्धांत

इस रणनीति में चार प्रमुख तकनीकी संकेतकों का उपयोग किया गया है:

-

पैराबोलिक SAR: यह संकेतक बिंदुओं और प्रवृत्ति के बीच संबंधों का उपयोग करके प्रवृत्ति की दिशा और उलटफेर बिंदुओं का निर्धारण करता है। जब बिंदु कीमत से ऊपर होता है तो यह तेजी (बुलिश) का संकेत है, और जब बिंदु कीमत से नीचे होता है तो यह मंदी (बेयरिश) का संकेत है। जब बिंदु कीमत को पार करता है तो यह प्रवृत्ति के उलटफेर को दर्शाता है। रणनीति SAR को प्रवृत्ति दिशा निर्धारित करने के लिए मुख्य संकेतक के रूप में उपयोग करती है।

-

RSI: सापेक्ष शक्ति सूचकांक। यह संकेतक 0-100 के बीच उतार-चढ़ाव के माध्यम से बाजार की ओवरबॉट या ओवरसोल स्थिति का आकलन करता है। RSI 70 से ऊपर ओवरबॉट क्षेत्र, 30 से नीचे ओवरसोल क्षेत्र और 50 के आसपास मध्य क्षेत्र को दर्शाता है। रणनीति RSI का उपयोग ओवरबॉट और ओवरसोल उलटफेर के संकेतों की पहचान करने के लिए करती है।

-

VOL: वॉल्यूम संकेतक। रणनीति VOL का उपयोग यह निर्धारित करने के लिए करती है कि वॉल्यूम में उल्लेखनीय वृद्धि हुई है या नहीं, जो प्रवृत्ति की पुष्टि और उलटफेर संकेतों की गुणवत्ता का आकलन करने में मदद करता है।

-

MA: मूविंग एवरेज। रणनीति मुख्य और गौण प्रवृत्तियों की दिशा निर्धारित करने के लिए छोटी और लंबी अवधि के मूविंग एवरेज का उपयोग करती है। जब छोटा MA लंबे MA को नीचे से ऊपर पार करता है तो यह तेजी (लॉन्ग) का संकेत है, और जब छोटा MA लंबे MA को ऊपर से नीचे पार करता है तो यह मंदी (शॉर्ट) का संकेत है।

ट्रेडिंग सिग्नल उत्पन्न करने के नियम:

लॉन्ग (खरीदारी) की शर्तें: SAR बिंदु K-लाइन के नीचे आ जाए, RSI नीचे से ऊपर की ओर बढ़ते हुए मध्य क्षेत्र में प्रवेश करे, VOL में स्पष्ट वृद्धि हो, और छोटा MA नीचे से ऊपर की ओर लंबे MA को पार करे।

शॉर्ट (बिक्री) की शर्तें: SAR बिंदु K-लाइन के ऊपर आ जाए, RSI ऊपर से नीचे की ओर गिरते हुए मध्य क्षेत्र में प्रवेश करे, VOL में स्पष्ट वृद्धि हो, और छोटा MA ऊपर से नीचे की ओर लंबे MA को पार करे।

इस रणनीति में टेक-प्रॉफिट और स्टॉप-लॉस जोखिम प्रबंधन नियम भी शामिल हैं। टेक-प्रॉफिट लक्ष्य प्रवेश मूल्य का 2 गुना है, और स्टॉप-लॉस मूल्य प्रवेश मूल्य का 0.8 गुना है, जो लाभ को लॉक करने और जोखिम को नियंत्रित करने में प्रभावी है।

लाभ विश्लेषण

इस रणनीति के निम्नलिखित लाभ हैं:

-

एकाधिक संकेतकों का संयोजन झूठे संकेतों को रोकता है और वास्तविक प्रवृत्ति परिवर्तनों को पकड़ता है।

-

जोखिम प्रबंधन में स्टॉप-लॉस और टेक-प्रॉफिट सेट करके जोखिम को प्रभावी ढंग से नियंत्रित किया जाता है।

-

पोजीशन प्रबंधन में किश्तों में प्रवेश और किश्तों में टेक-प्रॉफिट से लाभ अधिकतम होता है।

-

पैरामीटर बार-बार अनुकूलन और परीक्षण के माध्यम से सुनिश्चित किए गए हैं, जो पैरामीटर की मजबूती की गारंटी देते हैं।

-

बैकटेस्टिंग डेटा पर्याप्त है, जो वास्तविक ट्रेडिंग वातावरण का अनुकरण करता है।

-

संचालन तर्क स्पष्ट और सरल है, जिसे समझना और लागू करना आसान है।

जोखिम विश्लेषण

इस रणनीति में निम्नलिखित जोखिम भी हैं:

-

बाजार में असामान्य उतार-चढ़ाव के कारण स्टॉप-लॉस टूट सकता है। स्टॉप-लॉस की दूरी को उचित रूप से बढ़ाने की सलाह दी जाती है।

-

ट्रेडिंग उपकरण की कम तरलता के कारण स्टॉप-लॉस लागू नहीं हो पाता। ऐसे उपकरण चुनें जिनमें अच्छी तरलता हो।

-

प्रणालीगत जोखिम के कारण असामान्य गैप आ सकते हैं। लीवरेज कम करें और मूल्य-आधारित अच्छी संपत्ति रखें।

-

अत्यधिक पैरामीटर अनुकूलन के कारण कर्व बहुत सुंदर दिखाई दे सकता है। मजबूती बढ़ाने के लिए पैरामीटर को थोड़ा कमजोर करना चाहिए।

-

अत्यधिक ट्रेडिंग आवृत्ति के कारण स्लिपेज लागत बढ़ सकती है। ट्रेडिंग सिग्नल उत्पन्न करने के अंतराल को थोड़ा बढ़ाया जा सकता है।

-

संकेतों की प्रभावशीलता समय के साथ कम हो सकती है, जिसके लिए नियमित बैकटेस्टिंग और पैरामीटर अनुकूलन आवश्यक है।

अनुकूलन दिशाएँ

इस रणनीति को निम्नलिखित पहलुओं में और अनुकूलित किया जा सकता है:

-

MACD, KD आदि जैसे अधिक संकेतक संयोजनों का परीक्षण करके बेहतर मिलान खोजें।

-

MA अवधि पैरामीटर को अनुकूलित करके मुख्य और गौण प्रवृत्तियों को अधिक स्पष्ट रूप से पहचानें।

-

सर्वोत्तम जोखिम-लाभ अनुपात प्राप्त करने के लिए टेक-प्रॉफिट और स्टॉप-लॉस गुणांक को अनुकूलित करें।

-

विभिन्न उपकरणों पर पैरामीटर की मजबूती का परीक्षण करें और सर्वोत्तम पैरामीटर संयोजन खोजें।

-

ट्रेडिंग सिग्नल निर्धारण में सहायता के लिए मशीन लर्निंग मॉडल शामिल करें।

-

अनुकूली स्टॉप-लॉस एल्गोरिदम जोड़ें ताकि स्टॉप-लॉस वास्तविक उतार-चढ़ाव के करीब हो।

-

लंबी अवधि के पैरामीटर सेटिंग का परीक्षण करें और टेक-प्रॉफिट सीमा का विस्तार करें।

सारांश

यह रणनीति कई संकेतकों का उपयोग करके झूठे संकेतों को फ़िल्टर करती है और प्रवृत्ति दिशा का निर्धारण करती है, स्टॉप-लॉस और टेक-प्रॉफिट उपायों के साथ जोखिम को नियंत्रित करती है, और पैरामीटर अनुकूलन और संयोजन समायोजन के माध्यम से रणनीति की प्रभावशीलता में लगातार सुधार करती है। हालांकि कोई भी रणनीति भविष्य की पूर्ण भविष्यवाणी नहीं कर सकती, लेकिन एक व्यवस्थित ट्रेडिंग योजना और अच्छा जोखिम प्रबंधन लाभ की संभावना को काफी बढ़ा देगा। यह रणनीति एक अपेक्षाकृत मजबूत प्रवृत्ति अनुसरण समाधान प्रदान करती है, जो तर्कसंगत रूप से दीर्घकालिक स्थिर रिटर्न चाहने वाले निवेशकों के लिए उपयुक्त है।

- 1