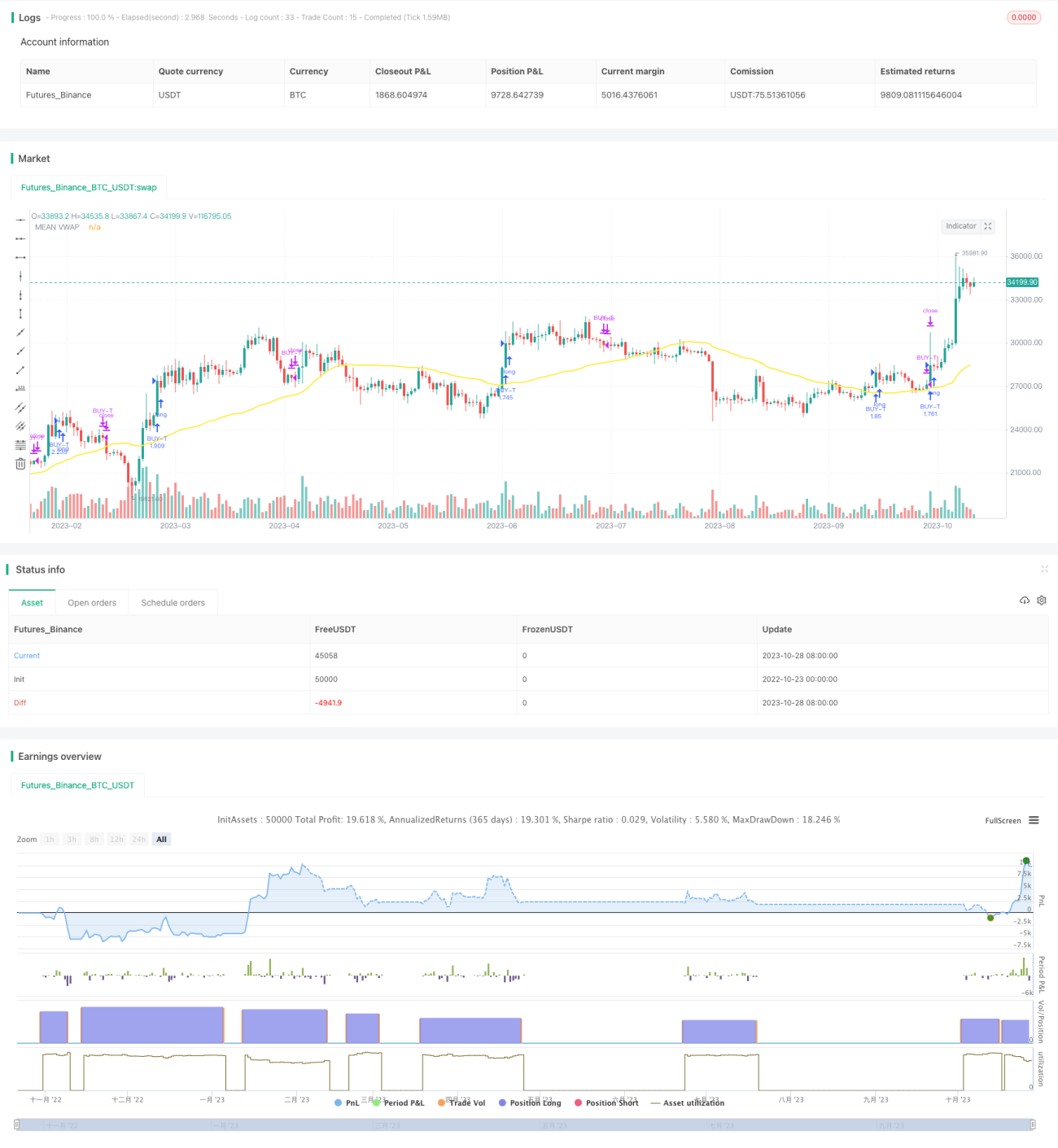

दोहरी रेखा ट्रैकिंग एल्गोरिथम व्यापार रणनीति

अवलोकन

यह रणनीति मुख्य रूप से मूविंग एवरेज क्रॉसओवर सिद्धांत, RSI संकेतक के उलट संकेत और कस्टम डुअल-लाइन ट्रैकिंग एल्गोरिदम का उपयोग करके मूविंग एवरेज क्रॉसओवर ट्रैकिंग ट्रेडिंग को लागू करती है। यह रणनीति दो अलग-अलग अवधियों के मूविंग एवरेज के क्रॉसओवर को ट्रैक करती है, एक तेज़ मूविंग एवरेज अल्पकालिक प्रवृत्ति को ट्रैक करता है और दूसरा धीमा मूविंग एवरेज दीर्घकालिक प्रवृत्ति को ट्रैक करता है। जब तेज़ मूविंग एवरेज धीमे मूविंग एवरेज को ऊपर की ओर पार करता है, तो यह अल्पकालिक प्रवृत्ति के ऊपर जाने का संकेत देता है, और खरीदारी की जा सकती है; जब तेज़ मूविंग एवरेज धीमे मूविंग एवरेज को नीचे की ओर पार करता है, तो यह अल्पकालिक प्रवृत्ति के समाप्त होने का संकेत देता है, और पोजीशन बंद कर देनी चाहिए।

रणनीति सिद्धांत

-

दो अलग-अलग मापदंडों के VWAP मूविंग एवरेज की गणना करें, जो क्रमशः दीर्घकालिक प्रवृत्ति और अल्पकालिक प्रवृत्ति का प्रतिनिधित्व करते हैं

- धीमी तियानमू रेखा और आधार रेखा दीर्घकालिक प्रवृत्ति की गणना करती है

- तेज़ तियानमू रेखा और आधार रेखा अल्पकालिक प्रवृत्ति की गणना करती है

-

दोनों समूहों की तियानमू रेखा और आधार रेखा के औसत को क्रमशः धीमी मूविंग एवरेज और तेज़ मूविंग एवरेज के रूप में लें

-

बोलिंगर बैंड संकेतक की गणना करके रेंज और ब्रेकआउट का निर्धारण करें

- मध्य रेखा तेज़ मूविंग एवरेज और धीमी मूविंग एवरेज का औसत है

- बोलिंगर बैंड की ऊपरी और निचली रेखाएं ब्रेकआउट का निर्धारण करने के लिए उपयोग की जाती हैं

-

TSV संकेतक की गणना करके ट्रेडिंग वॉल्यूम ऊर्जा का निर्धारण करें

- TSV > 0 का अर्थ है कि बढ़त की ताकत गिरावट की ताकत से अधिक है

- TSV > इसके EMA का अर्थ है कि ताकत बढ़ रही है

-

RSI संकेतक की गणना करके ओवरबॉट और ओवरसोल्ड की स्थिति का निर्धारण करें

- RSI < 30 ओवरसोल्ड क्षेत्र है, खरीदारी की जा सकती है

- RSI > 70 ओवरबॉट क्षेत्र है, बेच देना चाहिए

-

प्रवेश की शर्तें:

- तेज़ मूविंग एवरेज धीमी मूविंग एवरेज को ऊपर की ओर पार करे

- बंद मूल्य बोलिंगर बैंड की ऊपरी रेखा को ऊपर की ओर पार करे

- TSV > 0 और TSV > इसका EMA

- RSI < 30

-

निकास की शर्तें:

- तेज़ मूविंग एवरेज धीमी मूविंग एवरेज को नीचे की ओर पार करे

- RSI > 70

लाभ विश्लेषण

-

डुअल मूविंग एवरेज सिस्टम का उपयोग करके दीर्घकालिक और अल्पकालिक दोनों प्रवृत्तियों को एक साथ पकड़ा जा सकता है

-

RSI संकेतक ओवरबॉट क्षेत्र में खरीदारी और ओवरसोल्ड क्षेत्र में बिक्री से बचाता है

-

TSV संकेतक सुनिश्चित करता है कि प्रवृत्ति को समर्थन देने के लिए पर्याप्त ट्रेडिंग वॉल्यूम है

-

बोलिंगर बैंड का उपयोग करके महत्वपूर्ण ब्रेकआउट बिंदुओं का निर्धारण किया जा सकता है

-

कई संकेतकों का संयोजन झूठे ब्रेकआउट को प्रभावी ढंग से फ़िल्टर कर सकता है

जोखिम विश्लेषण

-

मूविंग एवरेज सिस्टम आसानी से गलत संकेत उत्पन्न कर सकता है, जिसे सहायक संकेतकों से फ़िल्टर करने की आवश्यकता होती है

-

RSI संकेतक के मापदंडों को अनुकूलित करने की आवश्यकता है, अन्यथा खरीद/बिक्री के अवसर छूट सकते हैं

-

TSV संकेतक भी मापदंडों के प्रति संवेदनशील है, इसलिए ध्यानपूर्वक परीक्षण की आवश्यकता है

-

बोलिंगर बैंड की ऊपरी रेखा का ब्रेकआउट झूठा हो सकता है, इसलिए सत्यापन की आवश्यकता है

-

कई संकेतकों के संयोजन से मापदंड अनुकूलन कठिन हो जाता है, और अत्यधिक अनुकूलन का खतरा रहता है

-

प्रशिक्षण और परीक्षण डेटा की अपर्याप्तता से कर्व फिटिंग हो सकती है

अनुकूलन दिशाएँ

-

अधिक अवधि मापदंडों का परीक्षण करके सर्वोत्तम मापदंड संयोजन खोजें

-

RSI के विकल्प या संयोजन के रूप में MACD, KD जैसे अन्य संकेतकों का प्रयास करें

-

मापदंड अनुकूलन में वॉक फॉरवर्ड विश्लेषण का पूरा उपयोग करें

-

एकल हानि को नियंत्रित करने के लिए स्टॉप-लॉस रणनीति जोड़ें

-

संकेत निर्णय में सहायता के लिए मशीन लर्निंग मॉडल शामिल करने पर विचार करें

-

विभिन्न बाजारों के लिए मापदंडों को समायोजित करें, एकल मापदंड संयोजन पर अत्यधिक निर्भर न रहें

सारांश

यह रणनीति डुअल मूविंग एवरेज सिस्टम के माध्यम से दीर्घकालिक और अल्पकालिक प्रवृत्तियों को पकड़ती है, साथ ही RSI, TSV, बोलिंगर बैंड जैसे कई संकेतकों का उपयोग करके संकेतों को फ़िल्टर करती है। रणनीति का लाभ यह है कि यह प्रवृत्ति के अनुसार चल सकती है और दीर्घकालिक बढ़त की लहर को पकड़ सकती है। हालांकि, इसमें कुछ झूठे संकेतों का जोखिम भी है, जिसके लिए मापदंडों को और अनुकूलित करने और जोखिम को कम करने के लिए स्टॉप-लॉस को नियंत्रित करने की आवश्यकता है। कुल मिलाकर, यह रणनीति प्रवृत्ति अनुसरण और उलट संकेतकों को जोड़ती है, और दीर्घकालिक तेजी वाले बाजारों में अच्छा प्रभाव दिखाती है, लेकिन विभिन्न बाजारों के लिए इसके मापदंडों को समायोजित करने की आवश्यकता है।

- 1