दोहरा प्रणाली संवेग व्यापार रणनीति

अवलोकन

यह रणनीति MACD और Stoch RSI दो संकेतकों के संयोजन का उपयोग करती है, एक दोहरी-ट्रैक ट्रेडिंग प्रणाली बनाती है जो ट्रेंड फॉलोइंग और ओवरसोल्ड/ओवरबॉट निर्णय को सक्षम बनाती है। रणनीति दैनिक और 4-घंटे के समय-सीमा पर संकेतक बनाती है ताकि बहु-समय-सीमा निर्णय हो सके और गलत निर्णय की संभावना कम हो सके।

रणनीति सिद्धांत

रणनीति MACD और Stoch RSI, दो अलग-अलग प्रकार के तकनीकी संकेतकों को जोड़ती है। MACD एक गति संकेतक है जो मूल्य परिवर्तन की गति का आकलन करता है; Stoch RSI एक ओवरबॉट/ओवरसोल्ड संकेतक है जो सापेक्ष मूल्य शक्ति का आकलन करता है।

रणनीति सबसे पहले दैनिक और 4-घंटे के समय-सीमा पर क्रमशः MACD और Stoch RSI संकेतक बनाती है ताकि ट्रेंड और ओवरबॉट/ओवरसोल्ड निर्णय हो सके। जब दोनों समय-सीमाओं पर संकेत सक्रिय होते हैं, तब संबंधित खरीद/बिक्री कार्रवाई की जाती है।

विशेष रूप से, MACD संकेतक में DIF और DEA लाइनों के गोल्डन क्रॉस/डेड क्रॉस का उपयोग निर्णय के लिए किया जाता है; Stoch RSI संकेतक में K और D लाइनों के गोल्डन क्रॉस/डेड क्रॉस का उपयोग निर्णय के लिए किया जाता है। जब दोनों संकेतक जोड़ियों में गोल्डन क्रॉस हों, तो खरीद संकेत उत्पन्न होते हैं; जब दोनों में डेड क्रॉस हों, तो बिक्री संकेत उत्पन्न होते हैं।

इस प्रकार, दोहरी-ट्रैक संकेतक प्रणाली और बहु-समय-सीमा निर्णयों के व्यापक अनुप्रयोग के माध्यम से, रणनीति मूल्य गति और सापेक्ष शक्ति का पूरी तरह से आकलन करती है, जो निर्णय सटीकता में सुधार करने और बेहतर रिटर्न प्राप्त करने में मदद करती है।

लाभ विश्लेषण

इस रणनीति के निम्नलिखित लाभ हैं:

- दोहरी-ट्रैक संकेतक प्रणाली का संयोजन, व्यापक निर्णय और उच्च निर्णय सटीकता प्रदान करता है

- बहु-समय-सीमा का उपयोग गलत निर्णय की संभावना को कम करता है

- ट्रेंड फॉलोइंग और ओवरबॉट/ओवरसोल्ड निर्णय को अपनाकर मूल्य गति और सापेक्ष शक्ति दोनों पर विचार करता है

- संकेतक पैरामीटर लचीले होते हैं, विभिन्न उत्पादों और बाजार परिस्थितियों के अनुकूल बनाए जा सकते हैं

- कोड संरचना स्पष्ट है, समझने और विस्तार करने में आसान है

जोखिम विश्लेषण

इस रणनीति में कुछ जोखिम भी हैं:

- बाजार में प्रणालीगत जोखिम मौजूद हैं जिन्हें पूरी तरह से टाला नहीं जा सकता

- अनुचित संकेतक पैरामीटर सेटिंग्स से अत्यधिक ट्रेडिंग या अवसरों की हानि हो सकती है

- दोहरे संकेतक गलत संकेत एक साथ दे सकते हैं, लेकिन एकल संकेतक की तुलना में कम संभावना होती है

- अचानक बाजार परिवर्तनों जैसे कि ब्लैक स्वान घटनाओं से निपटने में असमर्थ

समाधान:

- पैरामीटर ऑप्टिमाइज़ करें और ट्रेडिंग शर्तों को समायोजित करें ताकि गलत निर्णय कम हों

- संयुक्त निर्णय के लिए अधिक संकेतक शामिल करें

- एकल हानि जोखिम को नियंत्रित करने के लिए स्टॉप-लॉस रणनीतियाँ जोड़ें

अनुकूलन दिशाएँ

इस रणनीति को निम्नलिखित पहलुओं में भी बेहतर बनाया जा सकता है:

- बहु-संकेतक रणनीतियों के लिए अधिक संकेतक शामिल करें

- गतिशील पैरामीटर ऑप्टिमाइज़ेशन के लिए मशीन लर्निंग एल्गोरिदम जोड़ें

- अधिक व्यापक बाजार स्थिति निर्णय के लिए भावना संकेतकों, समाचार आदि को संयोजित करें

- पैसे प्रबंधन को अनुकूलित करने के लिए स्टॉप-लॉस, टेक-प्रॉफिट रणनीतियाँ जोड़ें

- बेहतर अवसर खोजने के लिए अधिक ट्रेडिंग उत्पादों तक विस्तार करें

सारांश

यह रणनीति दोहरी-ट्रैक संकेतकों और बहु-समय-सीमा निर्णयों के संयोजन के माध्यम से मूल्य गति और सापेक्ष शक्ति का व्यापक रूप से आकलन करती है, जो बाजार के रुझानों को प्रभावी ढंग से पकड़ सकती है और एकल संकेतकों की गलत निर्णय खामियों में सुधार कर सकती है। साथ ही, इसमें मापदंडों को लचीले ढंग से समायोजित करने, समझने और विस्तार करने में आसानी जैसे लाभ हैं। भविष्य में बहु-संकेतक संयोजन, गतिशील पैरामीटर ऑप्टिमाइज़ेशन, भावना संकेतकों के समावेश आदि के माध्यम से इसका विस्तार और अनुकूलन किया जा सकता है, जिससे रणनीति का प्रदर्शन और बेहतर हो सके।

निष्कर्ष

दोहरी-संकेतक प्रणाली और बहु-समय-सीमा निर्णयों के संयुक्त अनुप्रयोग से, यह रणनीति मूल्य गति और सापेक्ष शक्ति का गहन मूल्यांकन करती है, जो प्रभावी रूप से बाजार के रुझानों को पकड़ सकती है और एकल संकेतकों की कमियों को सुधार सकती है। इसके अलावा, इसमें लचीला पैरामीटर ट्यूनिंग, आसान समझ और विस्तार जैसे लाभ हैं। बहु-संकेतक संयोजन, गतिशील पैरामीटर अनुकूलन, भावना संकेतक शामिल करना आदि के माध्यम से आगे विस्तार रणनीति के प्रदर्शन को बढ़ाने में मदद कर सकता है।

[trans]

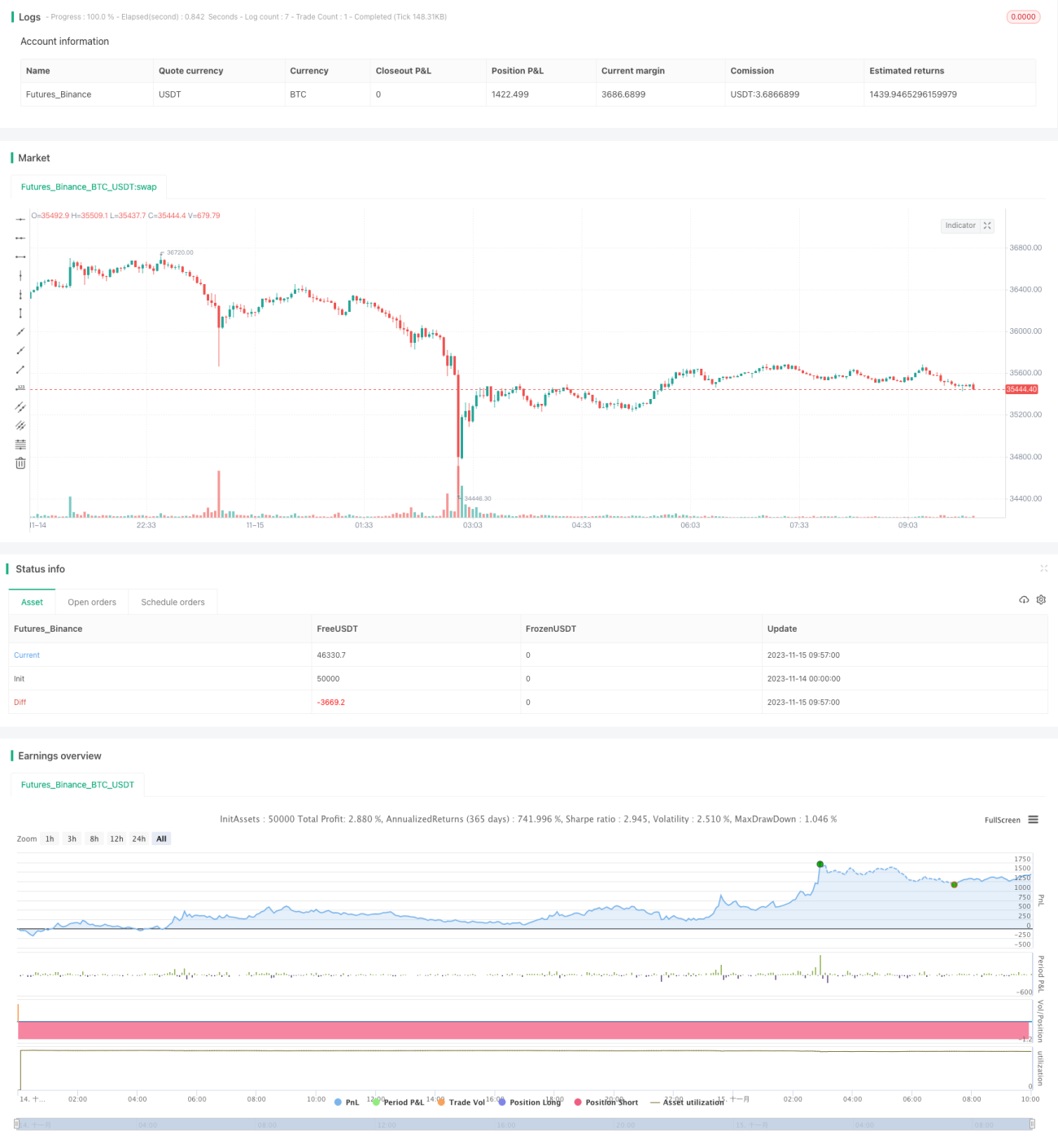

/*backtest

start: 2023-11-14 00:00:00

end: 2023-11-15 10:00:00

period: 3m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy(title='[RS]Khizon (UWTI) Strategy V0', shorttitle='K', overlay=false, pyramiding=0, initial_capital=100000, currency=currency.USD)

// || Inputs:

macd_src = input(title='MACD Source:', defval=close)- 1