दोहरे समय-फ्रेम और गति संकेतकों पर आधारित अनुकूली लाभ-हानि रोकने की रणनीति

अवलोकन

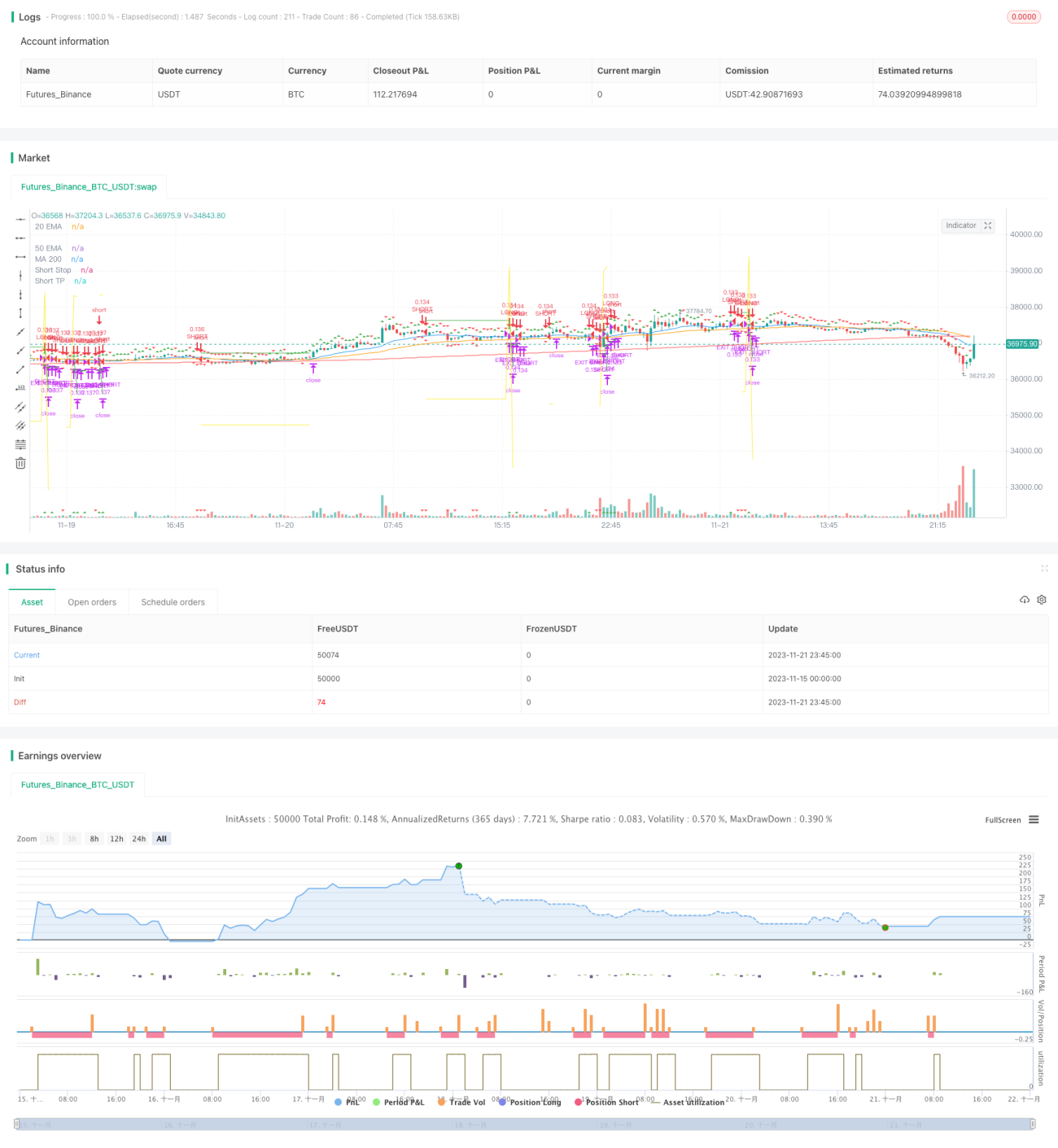

यह रणनीति दोहरे समय-सीमा और गति संकेतकों के संयोजन का उपयोग करके अनुकूली लाभ-सुरक्षित और हानि-सीमा तय करती है। मुख्य समय-सीमा प्रवृत्ति की दिशा की निगरानी करती है, जबकि सहायक समय-सीमा का उपयोग संकेतों की पुष्टि के लिए किया जाता है। जब दोनों की दिशा एक जैसी होती है, तो ट्रेडिंग संकेत उत्पन्न होता है। बाजार में प्रवेश करने के बाद, क्रमिक लाभ-सुरक्षित विधि के माध्यम से लाभ-सुरक्षित और हानि-सीमा के स्तरों को अद्यतन किया जाता है।

रणनीति का सिद्धांत

-

मुख्य समय-सीमा प्रवृत्ति का आकलन करने के लिए लीनियर रिग्रेशन इंडिकेटर Squeeze Momentum (SQM) का उपयोग करती है, जबकि सहायक समय-सीमा SQM संकेतक के EMA के संयोजन से फर्जी संकेतों को फ़िल्टर करती है।

-

जब मुख्य चार्ट पर SQM ऊपर की ओर ब्रेकआउट करता है और सहायक चार्ट पर SQM भी ऊपर जाता है, तो लॉन्ग पोजीशन लें; जब मुख्य चार्ट पर SQM नीचे की ओर ब्रेकआउट करता है और सहायक चार्ट पर SQM भी नीचे जाता है, तो शॉर्ट पोजीशन लें।

-

प्रवेश के बाद, इनपुट पैरामीटर के अनुसार प्रारंभिक लाभ-सुरक्षित और हानि-सीमा स्तर निर्धारित करें। जब कीमत लाभ-सुरक्षित स्तर तक पहुँचती है, तो लाभ-सुरक्षित और हानि-सीमा स्तरों को अपडेट करें। विशिष्ट तरीका यह है: लाभ-सुरक्षित स्तर को निर्धारित अनुपात में बढ़ाया जाता है, और हानि-सीमा स्तर को अनुपात में घटाया जाता है, जिससे क्रमिक लाभ-सुरक्षण सुनिश्चित होता है।

रणनीति के लाभ

-

दोहरी समय-सीमा फर्जी संकेतों को फ़िल्टर करती है, जिससे संकेतों की सटीकता सुनिश्चित होती है।

-

SQM संकेतक प्रवृत्ति की दिशा का आकलन करता है, जिससे बाजार के शोर से बचा जा सकता है।

-

अनुकूली लाभ-सुरक्षित और हानि-सीमा तंत्र, अधिकतम लाभ को सुरक्षित रखता है और जोखिम को प्रभावी ढंग से नियंत्रित करता है।

जोखिम विश्लेषण

-

SQM संकेतक के मापदंडों का अनुचित सेटिंग प्रवृत्ति के मोड़ को चूक सकता है, जिससे नुकसान हो सकता है।

-

सहायक चार्ट के लिए गलत समय-सीमा चुनने से शोर को प्रभावी ढंग से फ़िल्टर नहीं किया जा सकता, जिससे गलत ट्रेड हो सकते हैं।

-

हानि-सीमा की चौड़ाई बहुत अधिक होने पर प्रति ट्रेड नुकसान गंभीर हो सकता है।

अनुकूलन की दिशा

-

SQM संकेतक के मापदंडों को विभिन्न बाजारों के अनुसार समायोजित करने की आवश्यकता है ताकि इसकी संवेदनशीलता सुनिश्चित हो सके।

-

सहायक समय-सीमा के लिए भी विभिन्न अवधियों का परीक्षण किया जाना चाहिए ताकि यह देखा जा सके कि कौन सी अवधि सबसे अच्छी फ़िल्टरिंग प्रदान करती है।

-

हानि-सीमा को एक निश्चित मान के बजाय उतार-चढ़ाव की सीमा पर सेट किया जा सकता है, ताकि इसे बाजार की अस्थिरता के अनुसार समायोजित किया जा सके।

सारांश

यह रणनीति समग्र रूप से बहुत व्यावहारिक है। यह दोहरी समय-सीमा को गति संकेतकों के साथ जोड़कर प्रवृत्ति का आकलन करती है और अनुकूली लाभ-सुरक्षित और हानि-सीमा के माध्यम से स्थिर लाभ प्राप्त करती है। SQM संकेतक के मापदंडों, सहायक चार्ट की अवधि और हानि-सीमा की चौड़ाई को अनुकूलित करके रणनीति के प्रभाव को और बेहतर बनाया जा सकता है, जो इसे वास्तविक ट्रेडिंग में लागू करने और अनुकूलित करने के लिए उपयुक्त बनाता है।

/*backtest

start: 2023-11-15 00:00:00

end: 2023-11-22 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("SQZ Multiframe Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

fast_ema_len = input(11, minval=5, title="Fast EMA")

slow_ema_len = input(34, minval=20, title="Slow EMA")- 1