स्वर्ण विभाजन आधारित मीन रिवर्जन प्रवृत्ति व्यापार रणनीति

अवलोकन

गोल्डन रेशियो मीन रिवर्ज़न ट्रेंड ट्रेडिंग रणनीति चैनल इंडिकेटर और मूविंग एवरेज का उपयोग करके मजबूत ट्रेंड दिशा की पहचान करती है, और जब कीमत में एक निश्चित प्रतिशत की वापसी होती है, तो यह ट्रेंड की दिशा में पोजीशन खोल सकती है। यह रणनीति उन बाजारों के लिए उपयुक्त है जिनमें मजबूत ट्रेंड विशेषताएं होती हैं, और ट्रेंडिंग बाजार में अच्छा प्रदर्शन कर सकती है।

रणनीति सिद्धांत

इस रणनीति के मुख्य संकेतकों में चैनल इंडिकेटर, मूविंग एवरेज और रिट्रेसमेंट ट्रिगर लाइन शामिल हैं। विशेष रूप से:

- चैनल इंडिकेटर की गणना उच्चतम मूल्य और निम्नतम मूल्य से की जाती है, जिसका उपयोग मूल्य चैनल की पहचान करने के लिए किया जाता है;

- मूविंग एवरेज का उपयोग कीमत की समग्र ट्रेंड दिशा निर्धारित करने के लिए किया जाता है;

- रिट्रेसमेंट ट्रिगर लाइन का उपयोग कीमत के चैनल सीमा से एक निश्चित प्रतिशत वापस आने पर पोजीशन खोलने के लिए किया जाता है।

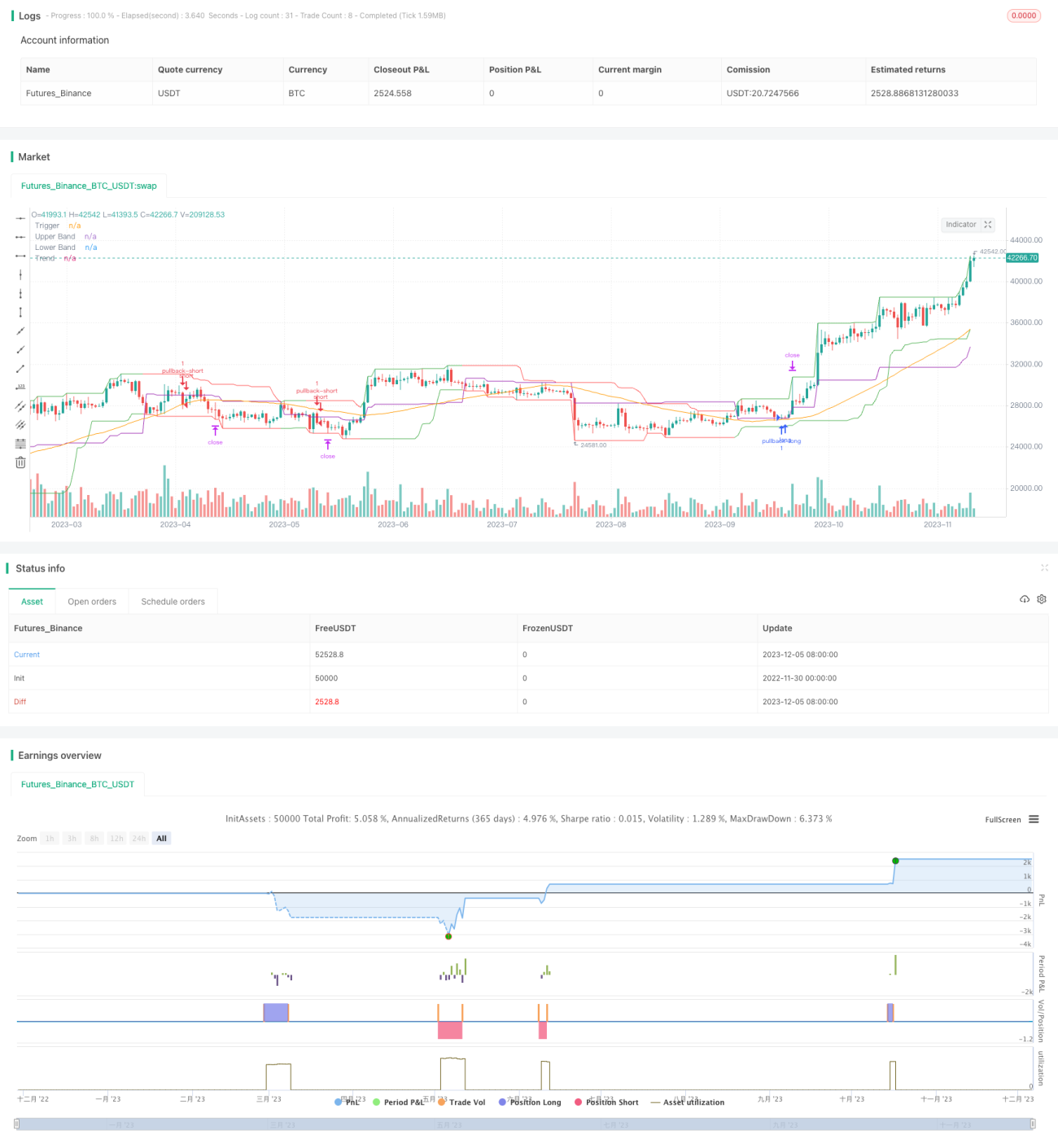

जब कीमत चैनल के निचले हिस्से को छूती है, तो रणनीति न्यूनतम बिंदु को संदर्भ बिंदु के रूप में रिकॉर्ड करती है और शॉर्ट जाने की अनुमति देने वाला फ्लैग सेट करती है। जब कीमत बढ़ती है और वृद्धि की मात्रा रिट्रेसमेंट अनुपात तक पहुंच जाती है, तो रिबाउंड बिंदु के पास शॉर्ट पोजीशन खोली जाती है।

इसके विपरीत, जब कीमत चैनल के शीर्ष को छूती है, तो रणनीति उच्चतम बिंदु को संदर्भ बिंदु के रूप में रिकॉर्ड करती है और लॉन्ग जाने की अनुमति देने वाला फ्लैग सेट करती है। जब कीमत गिरती है और गिरावट की मात्रा रिट्रेसमेंट अनुपालन तक पहुंच जाती है, तो उस बिंदु के पास लॉन्ग पोजीशन खोली जाती है।

इस प्रकार, इस रणनीति का ट्रेडिंग तर्क मूल्य चैनल को ट्रैक करना है और जब रिवर्सल सिग्नल दिखाई देते हैं तो मौजूदा ट्रेंड में शामिल होने के लिए उपयुक्त बिंदु चुनना है। यह ट्रेंड रिट्रेसमेंट प्रकार की ट्रेडिंग रणनीतियों का एक सामान्य तरीका है।

लाभ विश्लेषण

इस रणनीति के मुख्य लाभ इस प्रकार हैं:

- मजबूत ट्रेंडिंग बाजार में अच्छा प्रदर्शन कर सकती है;

- रिट्रेसमेंट अनुपात पैरामीटर के माध्यम से रणनीति की प्रवेश कठोरता को समायोजित किया जा सकता है;

- उचित ड्रॉडाउन नियंत्रण, जो एकल व्यापार में होने वाले नुकसान को सीमित कर सकता है।

विशेष रूप से, क्योंकि रणनीति मुख्य रूप से ट्रेंड रिवर्सल बिंदुओं पर पोजीशन खोलती है, यह उच्च मूल्य अस्थिरता और स्पष्ट ट्रेंड वाले बाजारों में बेहतर काम करती है। इसके अलावा, रिट्रेसमेंट अनुपात पैरामीटर को समायोजित करके रणनीति की ट्रेंड-ट्रैकिंग आक्रामकता को नियंत्रित किया जा सकता है। अंत में, स्टॉप-लॉस के माध्यम से एकल व्यापार में होने वाले नुकसान को अच्छी तरह से नियंत्रित किया जा सकता है।

जोखिम विश्लेषण

इस रणनीति में निम्नलिखित मुख्य जोखिम भी हैं:

- रणनीति ट्रेडिंग उत्पाद की ट्रेंड विशेषताओं के प्रति संवेदनशील है;

- रिट्रेसमेंट अनुपात का अनुचित सेटिंग अत्यधिक आक्रामक या रूढ़िवादी हो सकता है;

- पोजीशन होल्डिंग समय बहुत लंबा हो सकता है, ओवरनाइट जोखिम पर ध्यान देने की आवश्यकता है।

विशेष रूप से, यदि रणनीति जिस ट्रेडिंग उत्पाद पर लागू की जाती है, उसमें कमजोर ट्रेंड और कम अस्थिरता है, तो प्रदर्शन कम हो सकता है। इसके अलावा, रिट्रेसमेंट अनुपात बहुत बड़ा या बहुत छोटा होने से रणनीति के प्रदर्शन पर प्रभाव पड़ता है। अंत में, क्योंकि रणनीति की पोजीशन होल्डिंग अवधि लंबी हो सकती है, ओवरनाइट जोखिम के नियंत्रण पर भी ध्यान देने की आवश्यकता है।

उपरोक्त जोखिमों को कम करने के लिए, निम्नलिखित पहलुओं को अनुकूलित करने पर विचार किया जा सकता है:

- अधिक स्पष्ट ट्रेंड विशेषताओं वाले ट्रेडिंग उत्पादों का चयन करें;

- रिट्रेसमेंट अनुपात पैरामीटर को समायोजित करके सर्वोत्तम पैरामीटर संयोजन खोजें;

- पोजीशन होल्डिंग समय को उचित रूप से नियंत्रित करने के लिए टेक-प्रॉफिट एग्जिट सेट करें।

सारांश

गोल्डन रेशियो मीन रिवर्ज़न ट्रेंड ट्रेडिंग रणनीति सरल संकेतकों के माध्यम से मूल्य ट्रेंड और रिट्रेसमेंट सिग्नल निर्धारित करती है, और मजबूत बाजार में ट्रेंड को ट्रैक करने के लिए पोजीशन खोलती है। यह एक काफी विशिष्ट ट्रेंड सिस्टम है। इस रणनीति में पैरामीटर अनुकूलन के लिए काफी जगह है, और इसे अनुकूलन के माध्यम से अधिक बाजार वातावरण के अनुकूल बनाया जा सकता है, जबकि जोखिम नियंत्रण भी उचित है। इसलिए, यह एक ऐसी रणनीति अवधारणा है जो व्यावहारिक सत्यापन और सुधार के लिए योग्य है।

/*backtest

start: 2022-11-30 00:00:00

end: 2023-12-06 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

//

// A port of the TradeStation EasyLanguage code for a mean-revision strategy described at

// http://traders.com/Documentation/FEEDbk_docs/2017/01/TradersTips.html- 1