आंतरिक कैंडलस्टिक और मूविंग एवरेज पर आधारित स्वचालित क्वांटिटेटिव ट्रेडिंग रणनीति

अवलोकन

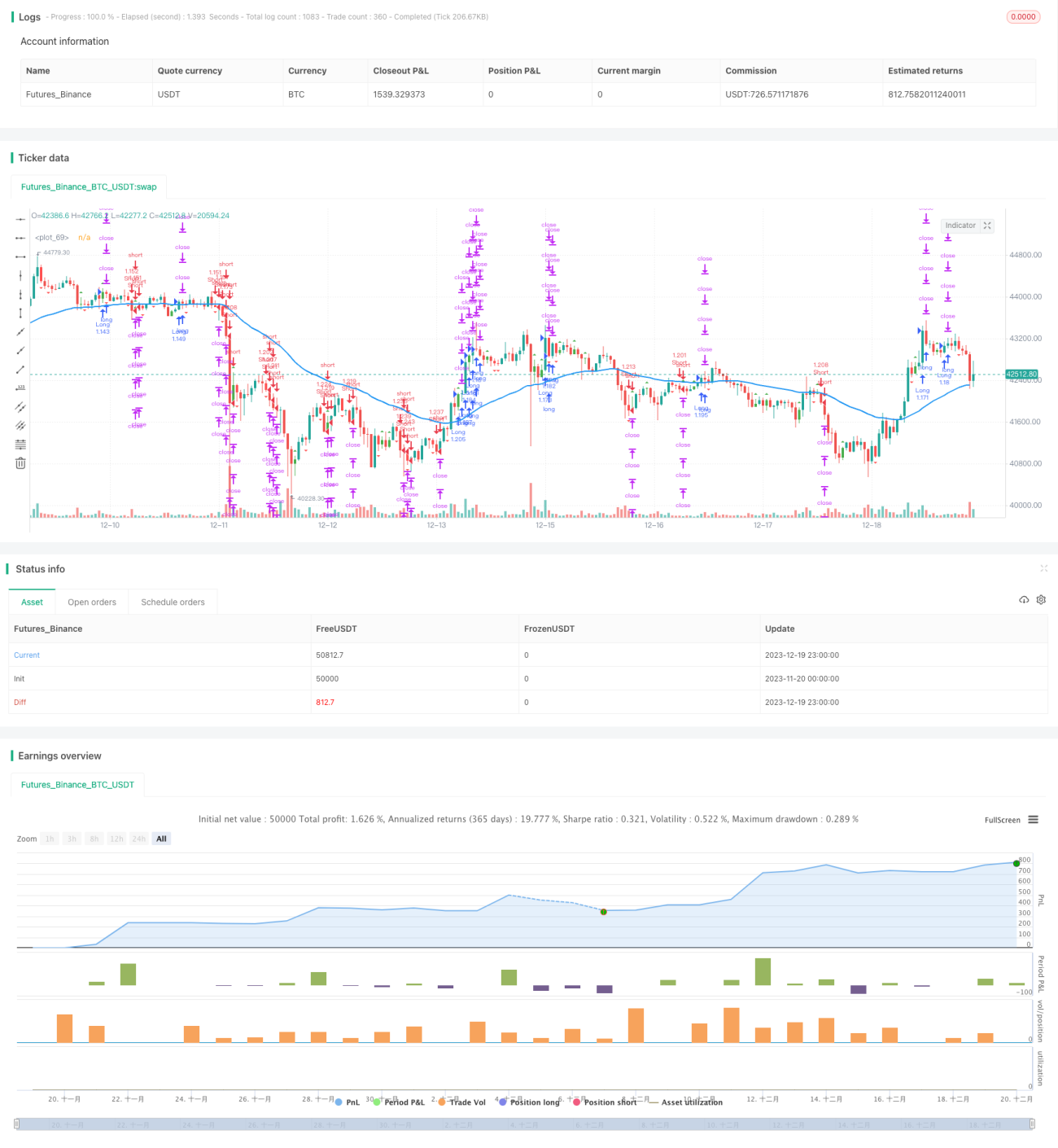

इस रणनीति का मूल विचार आंतरिक बार पैटर्न और मूविंग एवरेज संकेतकों को मिलाकर स्वचालित ट्रेडिंग करना है। जब आंतरिक बार पैटर्न दिखाई देता है, तो यह संकेत करता है कि वर्तमान प्रवृत्ति में संभावित बदलाव हो सकता है, और हम मूविंग एवरेज की स्थिति का उपयोग करके अंतिम ट्रेडिंग दिशा तय करते हैं।

रणनीति का सिद्धांत

-

आंतरिक बार पैटर्न की खोज: आंतरिक बार पैटर्न वह होता है जब किसी कैंडल का उच्चतम और निम्नतम मूल्य पिछली कैंडल के शरीर के बीच होता है। शरीर के रंग के आधार पर हम आंतरिक बार को बुलिश आंतरिक बार या बेयरिश आंतरिक बार के रूप में पहचान सकते हैं।

-

मूविंग एवरेज की स्थिति का निर्धारण: जब आंतरिक बार पैटर्न मिलता है, यदि मूल्य मूविंग एवरेज से ऊपर है, तो यह बुलिश संकेत है, और यदि मूल्य मूविंग एवरेज से नीचे है, तो यह बेयरिश संकेत है।

-

आंतरिक बार पैटर्न और मूविंग एवरेज के बुलिश/बेयरिश संकेतों को मिलाकर अंतिम ट्रेडिंग दिशा प्राप्त करना: अर्थात, बेयरिश आंतरिक बार औसत रेखा को तोड़कर नीचे जाए तो शॉर्ट करें, और बुलिश आंतरिक बार औसत रेखा को तोड़कर ऊपर जाए तो लॉन्ग करें।

रणनीति के लाभ

- तकनीकी संकेतकों और मूल्य पैटर्न का संयोजन, ट्रेडिंग निर्णयों की सटीकता में सुधार।

- आंतरिक बार पैटर्न में स्वयं प्रबल मूल्य उत्क्रमण संकेत होता है, जो प्रवृत्ति में बदलाव के बिंदु को जल्दी पहचानने में मदद करता है।

- मूविंग एवरेज कुछ शोर को फ़िल्टर कर देता है, जिससे सीमा में उतार-चढ़ाव के दौरान फंसने से बचा जा सकता है।

- पूरी तरह से स्वचालित ट्रेडिंग, जो मैन्युअल ट्रेडिंग के समय और मेहनत को काफी कम करती है।

रणनीति के जोखिम और समाधान

- जब मूल्य औसत रेखा के आसपास उतार-चढ़ाव करता है, तो कई गलत संकेत उत्पन्न हो सकते हैं, जिससे अत्यधिक ट्रेडिंग हो सकती है। मूविंग एवरेज के मापदंडों को अनुकूलित करके या अतिरिक्त फ़िल्टरिंग शर्तों को जोड़कर गलत संकेतों को कम किया जा सकता है।

- यह रणनीति स्पष्ट प्रवृत्ति वाले बाजारों में अधिक प्रभावी होती है; सीमा में उतार-चढ़ाव वाले बाजारों में इसका प्रदर्शन कम हो सकता है। एडीएक्स जैसे प्रवृत्ति निर्धारण संकेतकों को जोड़कर एल्गोरिदम के सक्रियण को नियंत्रित किया जा सकता है।

- कुछ समय अंतराल (lag) होता है। मापदंडों को उचित रूप से छोटा करके या मूविंग एवरेज की गणना को अनुकूलित करके इस lag को कम किया जा सकता है।

- ड्रॉडाउन का जोखिम अधिक होता है। स्टॉप लॉस लगाकर नुकसान के जोखिम को नियंत्रित किया जा सकता है, और साथ ही पोजीशन प्रबंधन को समायोजित करके भी ड्रॉडाउन को कम किया जा सकता है।

रणनीति के अनुकूलन की दिशाएँ

- आंतरिक बार की पहचान के लिए अवधि मापदंडों को अनुकूलित करना और सर्वोत्तम मापदंड संयोजन खोजना।

- विभिन्न प्रकार के मूविंग एवरेज जैसे EMA, SMA आदि का प्रयोग करके सबसे उपयुक्त मूविंग एवरेज संकेतक का चयन करना।

- MACD, KDJ जैसे सहायक संकेतकों को शामिल करना, ताकि बुलिश/बेयरिश निर्णय के आधार को समृद्ध किया जा सके और संकेतों की सटीकता बढ़ाई जा सके।

- ADX, ATR जैसे फ़िल्टर संकेतकों को जोड़ना, ताकि एल्गोरिदम के संचालन के लिए उपयुक्त वातावरण को नियंत्रित किया जा सके और अनुपयुक्त बाजारों में चलने से बचा जा सके।

- पोजीशन प्रबंधन रणनीति को अनुकूलित करना, जैसे जोखिम-आधारित पोजीशन नियंत्रण, लाभ के चूक जाने पर पोजीशन वापस लेना आदि, ताकि जोखिम को नियंत्रित करते हुए उच्च लाभ प्राप्त किया जा सके।

निष्कर्ष

यह रणनीति आंतरिक बार संकेतों और मूविंग एवरेज संकेतकों की गतिशील ट्रैकिंग के माध्यम से एक पूर्णतः स्वचालित मात्रात्मक ट्रेडिंग समाधान प्रस्तुत करती है। रणनीति के संकेत उत्पन्न करने की प्रक्रिया सरल और स्पष्ट है, जिसे समझना और ट्रैक करना आसान है। स्पष्ट प्रवृत्ति वाले बाजारों में इसका प्रदर्शन काफी अच्छा होता है। मापदंडों और नियमों को और अनुकूलित करके रणनीति की स्थिरता और लाभप्रदता को और बढ़ाया जा सकता है।

- 1