बोलिंजर बैंड निचला क्रॉस आरएसआई वापसी ट्रेडिंग रणनीति

अवलोकन

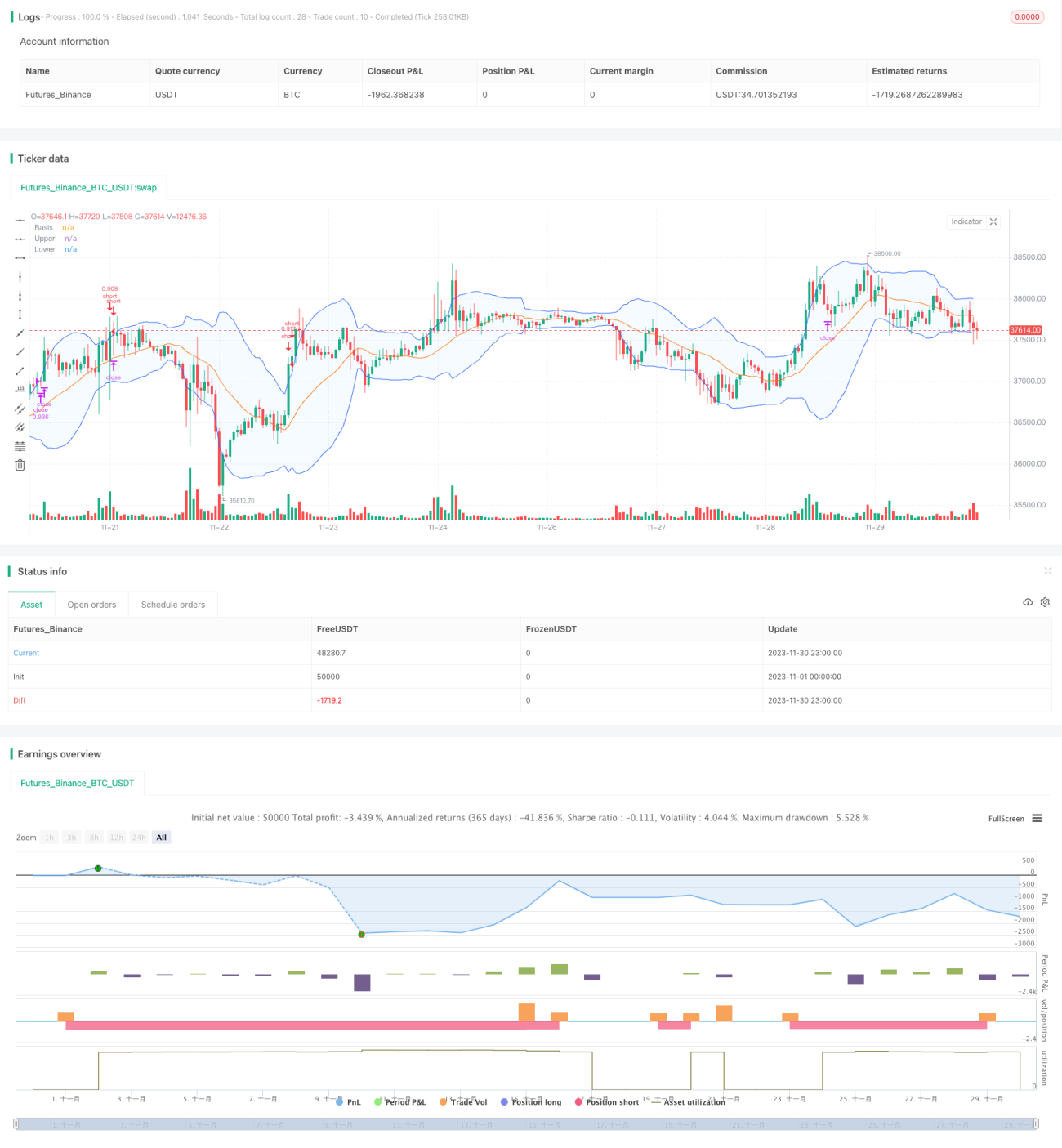

यह रणनीति बोलिंगर बैंड संकेतक का उपयोग करके यह पहचानती है कि कीमत ओवरबॉट या ओवरसोल्ड क्षेत्र में प्रवेश कर गई है या नहीं, और RSI संकेतक के साथ मिलकर यह आकलन करती है कि संभावित सुधार का अवसर है या नहीं। ओवरबॉट क्षेत्र में डेड क्रॉस बनने पर शॉर्ट पोजीशन ली जाती है, और जब कीमत बोलिंगर बैंड के ऊपरी बैंड से ऊपर बढ़ जाती है तो स्टॉप-लॉस लागू किया जाता है।

रणनीति का सिद्धांत

यह रणनीति मुख्य रूप से निम्नलिखित सिद्धांतों पर आधारित है:

- जब क्लोजिंग प्राइस बोलिंगर बैंड के ऊपरी बैंड को ऊपर की ओर पार करती है, तो यह संकेत देता है कि परिसंपत्ति ओवरबॉट क्षेत्र में प्रवेश कर गई है, जिसमें सुधार की संभावना है।

- RSI संकेतक प्रभावी रूप से ओवरबॉट और ओवरसोल्ड क्षेत्रों की पहचान कर सकता है; RSI > 70 ओवरबॉट क्षेत्र को इंगित करता है।

- जब क्लोजिंग प्राइस ऊपरी बैंड से नीचे आती है, तो शॉर्ट पोजीशन खोली जाती है।

- जब RSI ओवरबॉट क्षेत्र से वापस आता है या स्टॉप-लॉस पॉइंट ट्रिगर होता है, तो पोजीशन बंद कर दी जाती है और हानि सीमित की जाती है।

लाभ विश्लेषण

इस रणनीति के निम्नलिखित लाभ हैं:

- बोलिंगर बैंड का उपयोग करके ओवरबॉट/ओवरसोल्ड क्षेत्रों की पहचान करना, जिससे ट्रेडों की सफलता दर में सुधार होता है।

- RSI संकेतक के साथ मिलकर झूठे ब्रेकआउट के अवसरों को फ़िल्टर करना, अनावश्यक हानि से बचना।

- उच्च जोखिम-लाभ अनुपात, जोखिम पर अधिकतम नियंत्रण प्रदान करता है।

जोखिम विश्लेषण

इस रणनीति में निम्नलिखित जोखिम शामिल हैं:

- ऊपरी बैंड को तोड़ने के बाद कीमत में वृद्धि जारी रहने से हानि और अधिक बढ़ सकती है।

- RSI समय पर वापस नहीं आता, जिससे हानि और बढ़ सकती है।

- केवल एकतरफा पोजीशन, साइडवेज़ बाजार में ट्रेड करने में असमर्थता।

निम्नलिखित तरीकों से जोखिम कम किया जा सकता है:

- स्टॉप-लॉस पॉइंट को उचित रूप से समायोजित करें, समय पर हानि सीमित करें।

- RSI वापसी संकेतों का आकलन करने के लिए अन्य संकेतकों के साथ संयोजन करें।

- मूविंग एवरेज संकेतकों के साथ मिलकर यह निर्धारित करें कि बाजार साइडवेज़ है या नहीं।

अनुकूलन की दिशा

इस रणनीति को निम्नलिखित पहलुओं से अनुकूलित किया जा सकता है:

- अधिक ट्रेडिंग वस्तुओं के अनुकूल होने के लिए बोलिंगर बैंड के मापदंडों को अनुकूलित करें।

- संकेतक प्रभावशीलता में सुधार के लिए RSI मापदंडों को अनुकूलित करें।

- प्रवृत्ति उत्क्रमण बिंदुओं का आकलन करने के लिए अन्य संकेतकों का संयोजन जोड़ें।

- लॉन्ग ट्रेडिंग तर्क जोड़ें।

- स्टॉप-लॉस रणनीति के साथ मिलकर, स्टॉप-लॉस पॉइंट को गतिशील रूप से समायोजित करें।

सारांश

कुल मिलाकर, यह रणनीति एक विशिष्ट अल्पकालिक ओवरबॉट क्षेत्र त्वरित ट्रेडिंग रणनीति है। यह बोलिंगर बैंड का उपयोग करके खरीद/बिक्री बिंदुओं का निर्धारण करती है और RSI द्वारा संकेतों को फ़िल्टर करती है। उचित स्टॉप-लॉस के माध्यम से जोखिम स्तर को नियंत्रित किया जाता है। मापदंड अनुकूलन, संकेतक संयोजन और ओपनिंग लॉजिक जोड़कर प्रभावशीलता में सुधार किया जा सकता है।

- 1