द्विगुण प्रवृत्ति फ़िल्टर श्रृंखला गतिशील औसत अनुपात रणनीति

अवलोकन

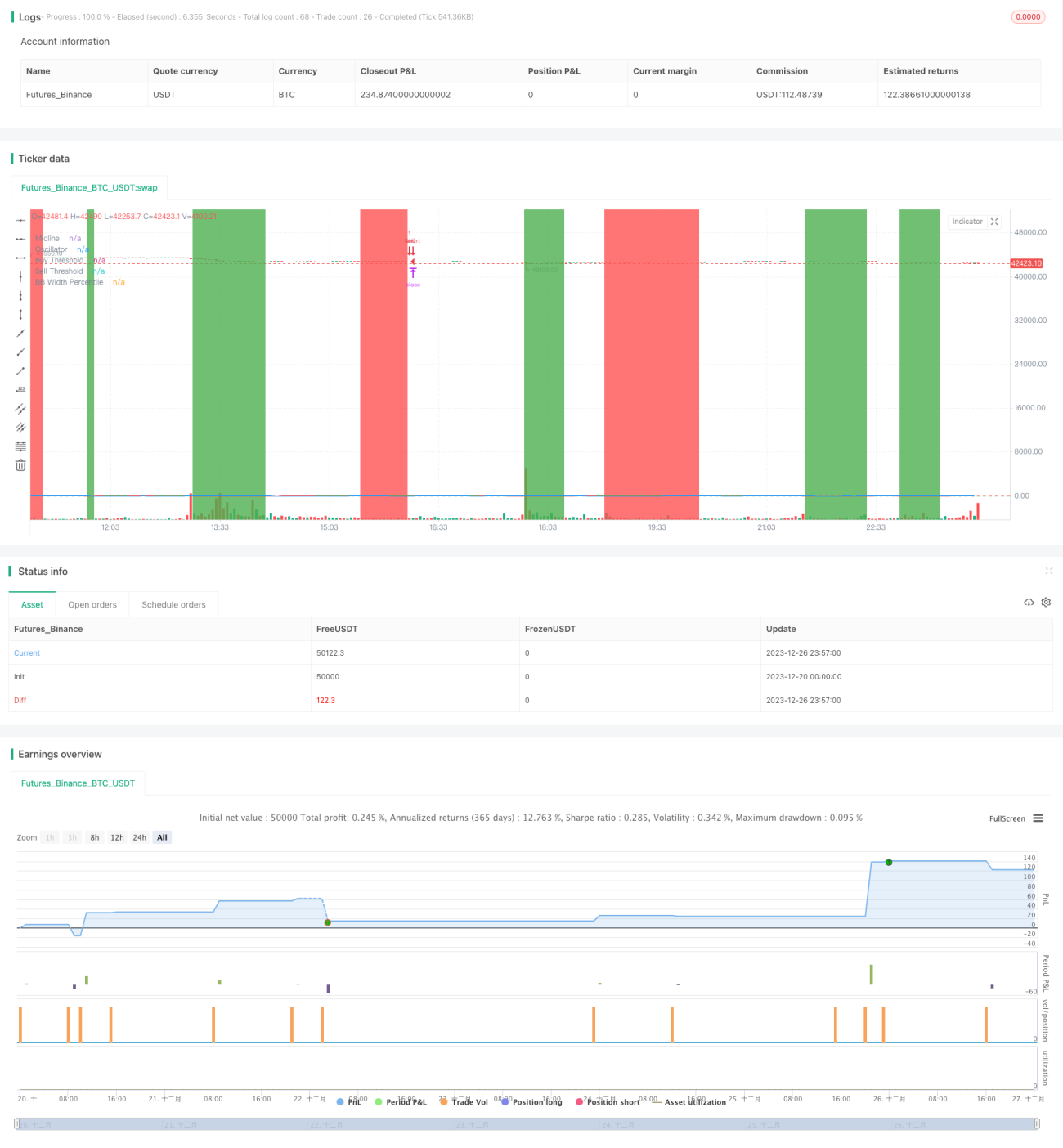

यह रणनीति दोहरी मूविंग एवरेज अनुपात संकेतक, बोलिंगर बैंड फ़िल्टर और दोहरी प्रवृत्ति फ़िल्टर संकेतक पर आधारित एक प्रवृत्ति-अनुसरण रणनीति है, जिसमें श्रृंखला-आधारित निकास तंत्र का उपयोग किया गया है। इस रणनीति का उद्देश्य मूविंग एवरेज अनुपात संकेतक का उपयोग करके मध्यम-दीर्घकालिक प्रवृत्ति की दिशा की पहचान करना है, और जब प्रवृत्ति स्पष्ट हो तो बेहतर प्रवेश बिंदु चुनकर प्रवेश करना है, साथ ही लाभ को लॉक करने और हानि को कम करने के लिए लाभ-लक्ष्य और स्टॉप-लॉस निकास तंत्र स्थापित करना है।

रणनीति सिद्धांत

- तेज़ मूविंग एवरेज (10-दिवसीय) और धीमी मूविंग एवरेज (50-दिवसीय) की गणना करें, और उनका अनुपात निकालें, जिसे मूल्य मूविंग एवरेज अनुपात कहा जाता है। यह अनुपात मध्यम-दीर्घकालिक प्रवृत्ति में परिवर्तन को प्रभावी ढंग से पहचान सकता है।

- मूल्य मूविंग एवरेज अनुपात को प्रतिशतक में बदलें, अर्थात पिछली अवधि में वर्तमान अनुपात की सापेक्ष शक्ति। इस प्रतिशतक को ऑसिलेटर के रूप में परिभाषित किया जाता है।

- जब ऑसिलेटर निर्धारित खरीद सीमा (10) को ऊपर से पार करता है, तो खरीद संकेत उत्पन्न होता है, और जब बिक्री सीमा (90) को नीचे से पार करता है, तो बिक्री संकेत उत्पन्न होता है, जिससे प्रवृत्ति का अनुसरण किया जाता है।

- बोलिंगर बैंड चौड़ाई संकेतक का उपयोग करके व्यापार संकेतों को फ़िल्टर किया जाता है; जब बोलिंगर बैंड संकीर्ण होता है, तो कार्रवाई की जाती है।

- दोहरे प्रवृत्ति फ़िल्टर संकेतक का उपयोग किया जाता है; केवल जब मूल्य आरोही प्रवृत्ति चैनल में हो, तब खरीद संकेत उत्पन्न होता है, और केवल जब मूल्य अवरोही चैनल में हो, तब बिक्री संकेत उत्पन्न होता है, जिससे प्रतिकूल प्रवृत्ति में व्यापार से बचा जाता है।

- श्रृंखला-आधारित निकास तंत्र स्थापित किया जाता है, जिसमें लाभ-लक्ष्य, स्टॉप-लॉस और संयुक्त निकास शामिल हैं; कई निकास शर्तों को पूर्व निर्धारित किया जा सकता है और सबसे अधिक लाभ वाली शर्त को प्राथमिकता दी जाती है।

रणनीति लाभ

- दोहरा प्रवृत्ति फ़िल्टर तंत्र मुख्य प्रवृत्ति की दिशा का विश्वसनीय निर्धारण करता है, जिससे प्रतिकूल प्रवृत्ति में व्यापार से बचा जाता है।

- मूविंग एवरेज अनुपात संकेतक एकल मूविंग एवरेज की तुलना में प्रवृत्ति परिवर्तन का अधिक प्रभावी ढंग से निर्धारण करता है।

- बोलिंगर बैंड चौड़ाई संकेतक बाजार की कम अस्थिरता की अवधि का प्रभावी ढंग से पता लगा सकता है, जब व्यापार संकेत अधिक विश्वसनीय होते हैं।

- श्रृंखला-आधारित निकास तंत्र लाभ को अधिक स्थिर बनाता है और कुल लाभ को अधिकतम करता है।

जोखिम और समाधान

- जब बाजार में कोई स्पष्ट प्रवृत्ति न हो और उतार-चढ़ाव हो, तो अधिक गलत संकेत और उलटफेर हो सकते हैं। समाधान: बोलिंगर बैंड चौड़ाई का उपयोग करके फ़िल्टर करें और संकीर्ण होने पर ही कार्रवाई करें।

- जब स्पष्ट प्रवृत्ति उलटफेर होता है, तो मूविंग एवरेज में पिछड़ापन होता है और तुरंत उलट संकेत का पता नहीं चल पाता। समाधान: मूविंग एवरेज की अवधि पैरामीटर को उचित रूप से छोटा करें।

- जब बाजार में गैप (अंतराल) होता है, तो स्टॉप-लॉस बिंदु तुरंत टकरा सकता है, जिससे बड़ी हानि हो सकती है। समाधान: स्टॉप-लॉस पैरामीटर को उचित रूप से ढीला करें।

रणनीति अनुकूलन दिशा-निर्देश

- पैरामीटर अनुकूलन। मूविंग एवरेज अवधि, ऑसिलेटर खरीद/बिक्री बिंदु, बोलिंगर बैंड पैरामीटर और प्रवृत्ति फ़िल्टर पैरामीटर का व्यापक परीक्षण करके सर्वोत्तम पैरामीटर संयोजन खोजा जा सकता है।

- अन्य संकेतकों का सम्मिलन। प्रवृत्ति उलटफेर का पता लगाने वाले अन्य संकेतक, जैसे KD संकेतक, MACD संकेतक आदि, जोड़ने पर विचार किया जा सकता है, जिससे रणनीति की सटीकता में सुधार होगा।

- मशीन लर्निंग। ऐतिहासिक डेटा एकत्र करके, मशीन लर्निंग एल्गोरिदम का उपयोग करके मॉडल को प्रशिक्षित किया जा सकता है, विभिन्न पैरामीटरों को गतिशील रूप से अनुकूलित किया जा सकता है और पैरामीटरों का स्व-अनुकूलन प्राप्त किया जा सकता है।

सारांश

यह रणनीति दोहरे मूविंग एवरेज अनुपात संकेतक और बोलिंगर बैंड संकेतक का एकीकृत उपयोग करके मध्यम-दीर्घकालिक प्रवृत्ति की दिशा निर्धारित करती है, प्रवृत्ति की पुष्टि के बाद सबसे अच्छा प्रवेश बिंदु ढूंढती है, और श्रृंखला-आधारित निकास तंत्र के माध्यम से लाभ को लॉक करती है। यह उच्च विश्वसनीयता और स्पष्ट प्रभाव प्रदान करती है। इस रणनीति को पैरामीटर अनुकूलन, अन्य सहायक निर्णय संकेतकों के समावेश और मशीन लर्निंग के माध्यम से और बेहतर बनाकर लाभप्रदता बढ़ाई जा सकती है।

- 1