आरएसआई संकेतक पर आधारित क्रॉस-टाइमफ्रेम रणनीति

1

Follow

1789

Followers

अवलोकन

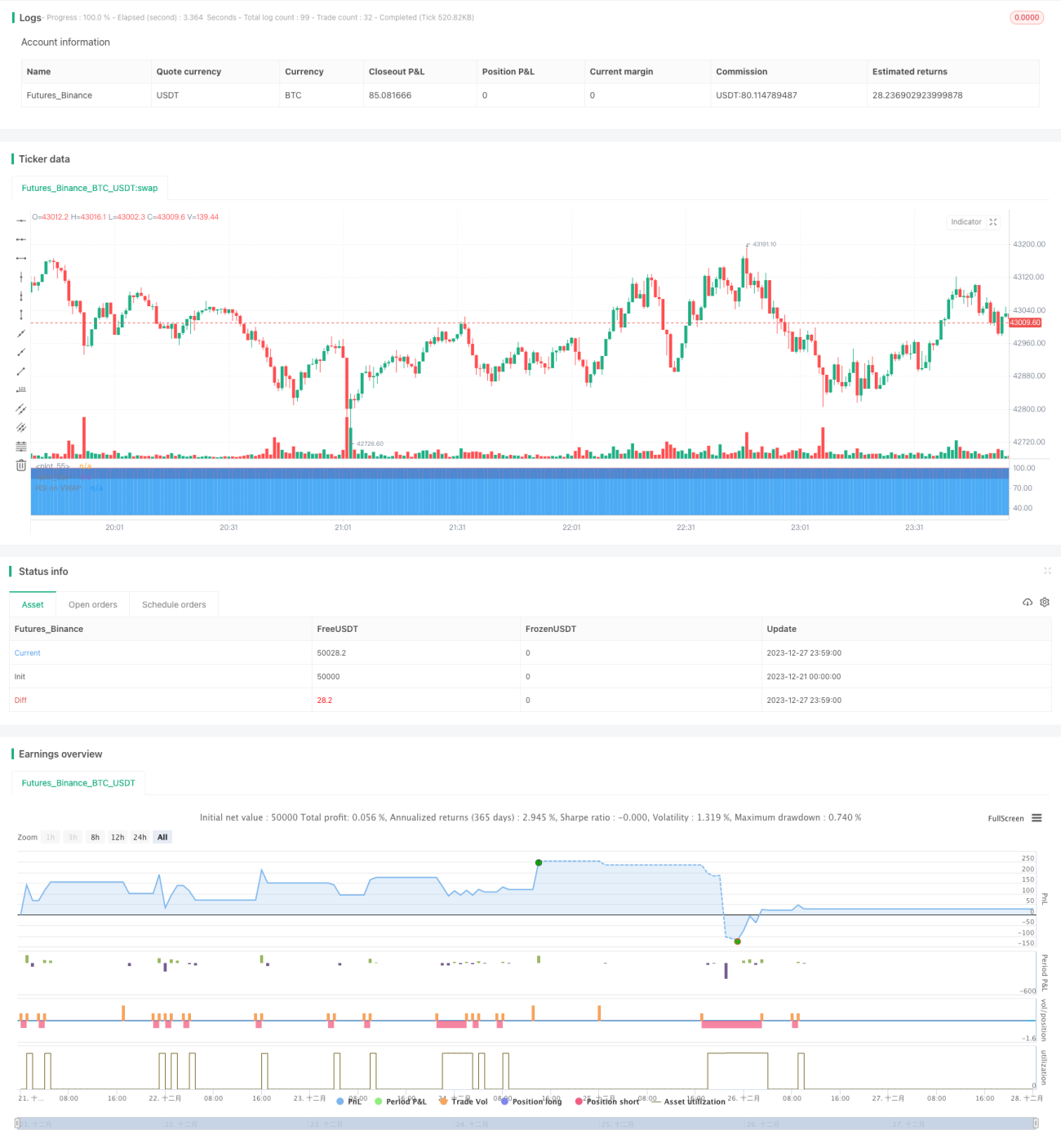

यह रणनीति आरएसआई पर आधारित एक क्रॉस टाइम फ्रेम बीटीसी कमोडिटी रणनीति है। इस रणनीति को प्रत्येक के-लाइन के लिए लेन-देन के भारित औसत मूल्य (वीडब्ल्यूएपी) की गणना करके एक वीडब्ल्यूएपी वक्र प्राप्त किया जाता है, और फिर आरएसआई को उस वक्र पर लागू किया जाता है। जब आरएसआई ओवरबॉय क्षेत्र से नीचे की ओर जाने वाले डेड फोर्क सिग्नल का संकेत देता है, तो बीटीसी को कम करें।

रणनीति सिद्धांत

- प्रत्येक K लाइन के लिए लेनदेन भारित औसत मूल्य (VWAP) की गणना करें, एक VWAP वक्र प्राप्त करें

- आरएसआई को वीडब्ल्यूपी वक्र पर लागू करें, पैरामीटर 20 दिन है, ओवरबॉय लाइन 85 है, ओवरबॉय लाइन 30 है

- जब आरएसआई सूचकांक ओवरबॉय क्षेत्र से नीचे की ओर बढ़ता है (85), ओवरबॉय क्षेत्र (30) से नीचे की ओर बढ़ता है, तो स्थिति खोलें

- 28 के लाइन के बाद, यदि आरएसआई सूचकांक फिर से ओवरसोल्ड लाइन को पार कर जाता है, तो स्थिति को बंद कर दिया जाता है

श्रेष्ठता विश्लेषण

- वीडब्ल्यूपीएपी का उपयोग वास्तविक लेनदेन की कीमतों को प्रतिबिंबित करने के लिए एक सरल समापन मूल्य के बजाय किया जाता है

- आरएसआई सूचक का उपयोग करें ओवरबॉट और ओवरसोल्ड स्थिति की पहचान करने के लिए

- समय सीमा के साथ काम करें और फंसने से बचें

- 28 के-लाइनों का नुकसान

जोखिम और समाधान

- अचानक हुई घटना ने कीमतों में तेजी से वृद्धि को रोक नहीं पाया

- समय सीमा के साथ जोखिम को कम करें

- गलत पैरामीटर, अवसरों को याद करना आसान

- आरएसआई पैरामीटर और ओवरबॉय ओवरसोल लाइन का परीक्षण और अनुकूलन

- के-लाइन को सुपरमार्केट में प्रवेश करने से रोक दिया गया

- अन्य संकेतकों के साथ प्रवृत्ति का आकलन करने के लिए, पैरामीटर को लचीले ढंग से समायोजित करें

अनुकूलन दिशा

- अधिक संयोजनों का परीक्षण करें और सबसे अच्छा खोजें

- MACD, KD और अन्य संकेतकों के साथ संयुक्त, यह निर्धारित करने के लिए कि क्या यह ओवरबॉट और ओवरसोल्ड क्षेत्र में है

- विभिन्न किस्मों के अनुसार परीक्षण मापदंडों की स्थापना

- ऑप्टिमाइज़्ड स्टॉप लॉस मैकेनिज्म, अस्थिरता के आधार पर स्टॉप लॉस की सीमा सेट करें

संक्षेप

यह रणनीति वीडब्ल्यूपी और आरएसआई के संयोजन के माध्यम से बीटीसी की ओवरबॉय और ओवरसोल स्थिति की पहचान करती है, जो समय-सीमा के तरीके से संचालन करती है, जो जोखिम को प्रभावी ढंग से नियंत्रित करने में सक्षम है। रणनीति विचार स्पष्ट और समझने योग्य है, आगे परीक्षण और अनुकूलन के लायक है, जो कि वास्तविक समय के व्यापार के लिए लागू है।

Source

Pine

/*backtest

start: 2023-12-21 00:00:00

end: 2023-12-28 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("Soran Strategy 2 - SHORT SIGNALS", pyramiding=1, initial_capital=1000, default_qty_type=strategy.percent_of_equity, default_qty_value=50, overlay=false)Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1