गतिशील औसत लागत निवेश चक्रवृद्धि ब्याज रणनीति

अवलोकन

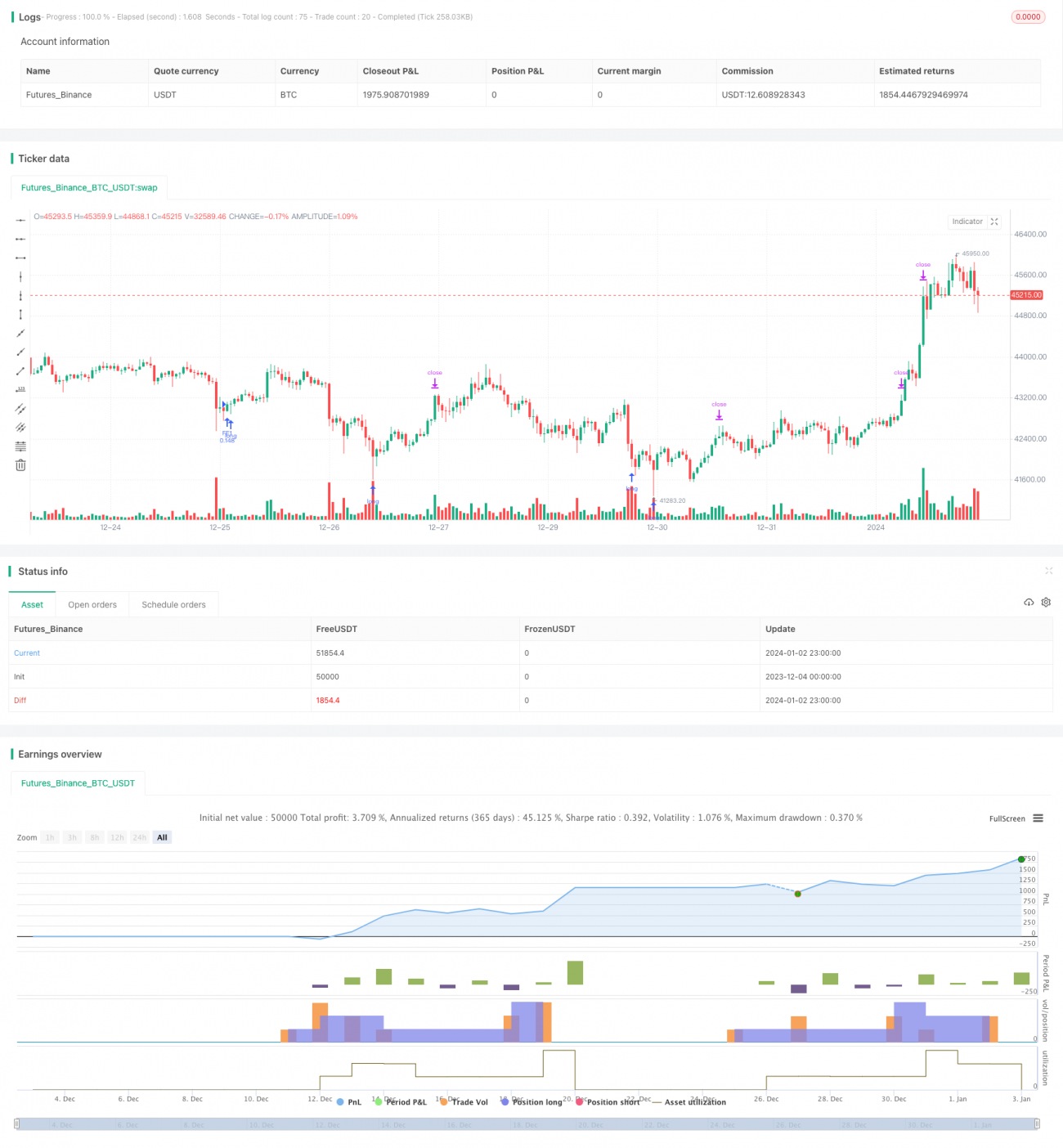

गतिशील औसत लागत निवेश (DCA) चक्रवृद्धि ब्याज रणनीति प्रत्येक बार खोले जाने वाले पोजीशन की मात्रा को गतिशील रूप से समायोजित करती है। प्रवृत्ति की शुरुआत में कम मात्रा में पोजीशन खोली जाती है और जैसे-जैसे सीमा-व्यापार (रेंज ट्रेडिंग) की गहराई बढ़ती है, पोजीशन का आकार धीरे-धीरे बढ़ाया जाता है। यह रणनीति प्रति स्तर पर स्टॉप-लॉस मूल्य की गणना के लिए एक घातांकीय फलन का उपयोग करती है, और जब यह ट्रिगर होता है तो नए बैचों में फिर से पोजीशन खोलती है, जिससे होल्डिंग कॉस्ट लाइन घातांकीय रूप से नीचे आती रहती है। गहराई बढ़ने के साथ पोजीशन की लागत धीरे-धीरे कम की जा सकती है, और कीमत के उलटने के बाद चरणबद्ध तरीके से लाभ बुक करके बड़ा मुनाफा प्राप्त किया जा सकता है।

रणनीति सिद्धांत

यह रणनीति सरल RSI ओवरसोल्ड पॉइंट सिग्नल और मूविंग एवरेज के समय-चयन तरीके को जोड़ती है ताकि पोजीशन खोलने का समय चुना जा सके। जब RSI ओवरसोल्ड लाइन से नीचे होता है और क्लोजिंग प्राइस मूविंग एवरेज से कम होती है, तो पहला ऑर्डर सिग्नल उत्पन्न होता है। पहला ऑर्डर खोलने के बाद, घातांकीय फलन के अनुसार मूल्य में गिरावट की निचली सीमा की गणना की जाती है, जिससे DCA सिग्नल उत्पन्न होता है। प्रत्येक DCA के बाद, होल्डिंग मात्रा को समायोजित किया जाता है ताकि प्रति लॉट पोजीशन बराबर रहे। होल्डिंग मात्रा और होल्डिंग लागत में गतिशील परिवर्तन के कारण, यह एक लीवरेज एम्प्लीफिकेशन प्रभाव के समान कार्य करता है।

जैसे-जैसे DCA की संख्या बढ़ती है, होल्डिंग लागत लगातार घटती जाती है, और लाभ बुक करने के लिए केवल एक छोटे से रिबाउंड की आवश्यकता होती है। लगातार कई ऑर्डर खोलने के बाद, औसत मूल्य के ऊपर एक स्टॉप-लॉस लाइन खींची जाती है। एक बार जब कीमत ऊपर की ओर टूटकर होल्डिंग औसत मूल्य और स्टॉप-लॉस लाइन से ऊपर चली जाती है, तो स्टॉप-लॉस निकास होता है।

इस रणनीति का सबसे बड़ा लाभ यह है कि होल्डिंग लागत लगातार कम होने के कारण, सीमा-व्यापार (रेंज मार्केट) में भी लागत को धीरे-धीरे कम किया जा सकता है। जब प्रवृत्ति उलटती है, तो होल्डिंग लागत बाजार मूल्य से काफी कम होने के कारण अधिक लाभ प्राप्त किया जा सकता है।

जोखिम और कमियाँ

इस रणनीति का सबसे बड़ा जोखिम प्रारंभिक पोजीशन की सीमित मात्रा है। यदि कीमत लगातार गिरती रहती है, तो स्टॉप-लॉस का जोखिम होता है। इसलिए अपनी सहनशीलता के अनुसार उचित स्टॉप-लॉस सीमा निर्धारित करना आवश्यक है।

इसके अलावा, स्टॉप-लॉस सीमा निर्धारित करने में भी दो चरम स्थितियाँ होती हैं। बहुत बड़ी स्टॉप-लॉस सीमा से पर्याप्त गहराई का रिबाउंड नहीं मिल पाता, जबकि बहुत छोटी स्टॉप-लॉस सीमा के मामले में मध्यम अवधि के समायोजन के दौरान कीमत के फिर से उलटने और तेजी की संभावना अधिक होती है। इसलिए, विभिन्न बाजारों और अपनी जोखिम सहनशीलता के अनुसार उपयुक्त स्टॉप-लॉस सीमा चुनना बहुत महत्वपूर्ण है।

जब DCA चक्र लंबा होता है और कई स्तर बन जाते हैं, यदि कीमत में बड़ी तेजी आती है, तो पोजीशन की लागत बहुत अधिक हो सकती है, जिससे स्टॉप-लॉस निकास असंभव हो सकता है। इसलिए अपनी कुल पोजीशन और सहन करने योग्य अधिकतम पोजीशन लागत के आधार पर DCA स्तरों को उचित रूप से निर्धारित करना आवश्यक है।

अनुकूलन सुझाव

-

समय-चयन संकेतों का अनुकूलन करें। अधिक जीत दर वाले संकेतों की उम्मीद में विभिन्न पैरामीटर और विभिन्न संकेतक संयोजनों का परीक्षण किया जा सकता है।

-

स्टॉप-लॉस तंत्र का अनुकूलन करें। सरल मूविंग स्टॉप-लॉस के बजाय Λ-आकार या गोलाकार स्टॉप-लॉस का परीक्षण किया जा सकता है, जो बेहतर स्टॉप-लॉस प्रभाव दे सकता है। पोजीशन को समय-विभाजित करके स्टॉप-लॉस सीमा को समायोजित करने की रणनीति भी जोड़ी जा सकती है।

-

लाभ-बुक करने के तरीके का अनुकूलन करें। विभिन्न प्रकार के मूविंग प्रॉफिट-टेकिंग का परीक्षण करके बेहतर लाभ-बुकिंग निकास अवसर खोजें, जिससे समग्र रिटर्न दर में सुधार हो सके।

-

एंटी-रिबाउंड तंत्र जोड़ें। स्टॉप-लॉस के बाद, फिर से DCA सिग्नल ट्रिगर हो सकता है और नई पोजीशन खोली जा सकती है। ऐसे में, एक निश्चित सीमा तक एंटी-रिबाउंड रेंज जोड़ने पर विचार किया जा सकता है ताकि स्टॉप-लॉस के तुरंत बाद आक्रामक तरीके से पोजीशन न खोली जाए।

सारांश

यह रणनीति RSI संकेतक का उपयोग करके खरीद के समय का निर्धारण करती है, और घातांकीय फलन के आधार पर गणना की गई गतिशील स्टॉप-लॉस DCA रणनीति के माध्यम से होल्डिंग मात्रा और होल्डिंग लागत को गतिशील रूप से समायोजित करती है, जिससे रेंज मार्केट में मूल्य लाभ प्राप्त होता है। अनुकूलन मुख्य रूप से प्रवेश/निकास संकेतों, स्टॉप-लॉस और लाभ-बुकिंग तरीकों पर केंद्रित है। कुल मिलाकर, यह रणनीति घातांकीय DCA के मूल सिद्धांत का उपयोग करती है, जिससे होल्डिंग लागत लगातार नीचे आती है, सीमा-व्यापार के दौरान अधिक संचालन स्थान मिलता है, और प्रवृत्ति में उच्च रिटर्न प्राप्त होता है। फिर भी, अपने धन प्रबंधन योजना के अनुसार कुल पोजीशन जोखिम को नियंत्रित करने के लिए उपयुक्त पैरामीटर चुनना आवश्यक है।

- 1