वॉल्यूम ऑसिलेटर पर आधारित ट्रेंड फॉलोइंग ट्रेडिंग रणनीति

अवलोकन

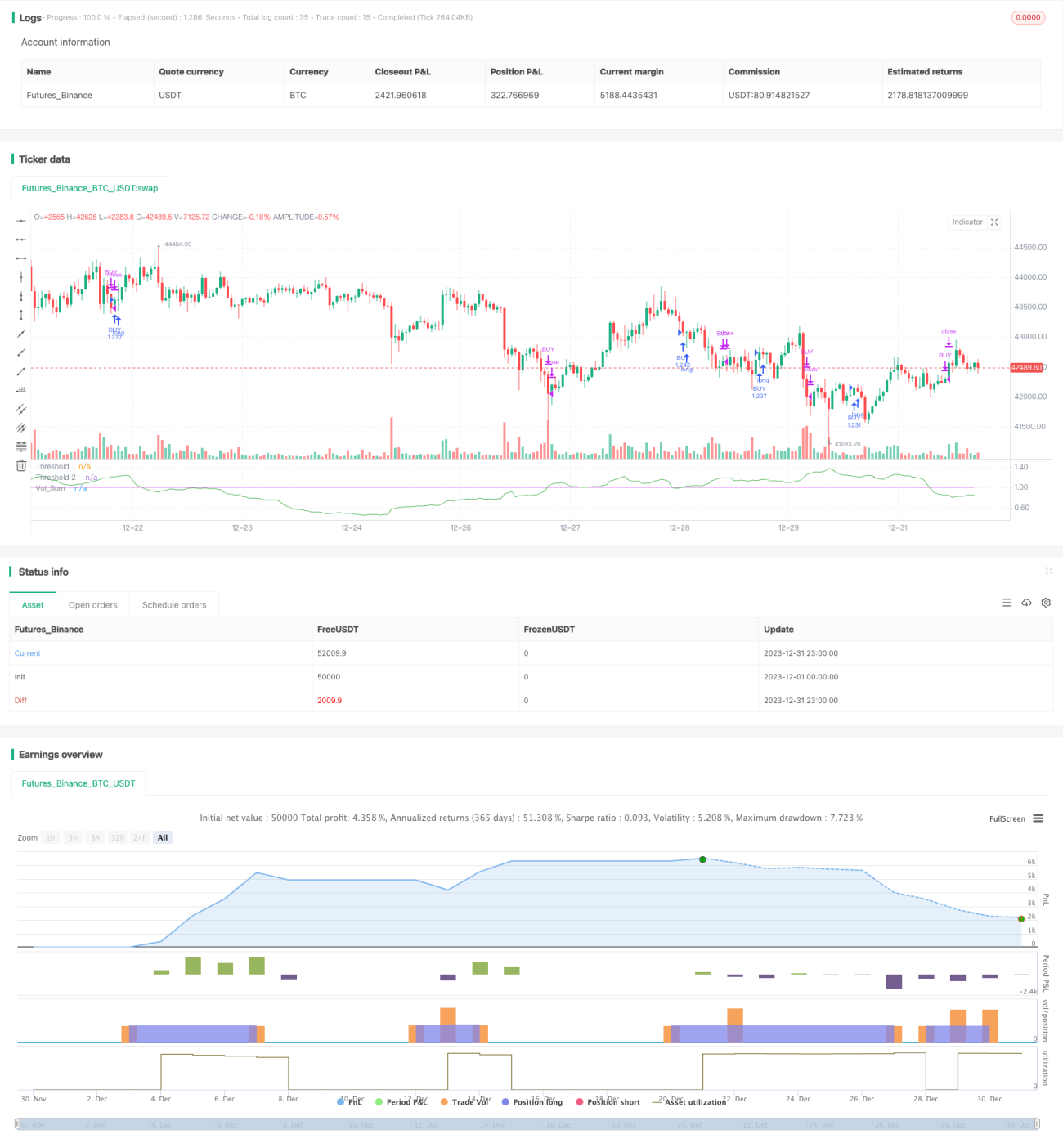

यह रणनीति एक संशोधित वॉल्यूम ऑसिलेटर इंडिकेटर पर आधारित ट्रेंड-फॉलोइंग रणनीति है। यह वॉल्यूम के मूविंग एवरेज का उपयोग करके वॉल्यूम में वृद्धि के सिग्नलों की पहचान करती है, जिससे पोजीशन में प्रवेश या निकास का निर्णय लिया जाता है। साथ ही, यह मूल्य के रुझान का विश्लेषण करके कीमत में उतार-चढ़ाव के दौरान गलत सिग्नल उत्पन्न होने से बचाती है।

रणनीति का सिद्धांत

- वॉल्यूम का मूविंग एवरेज vol_sum की गणना करें, जिसकी लंबाई vol_length है, और इसे vol_smooth लंबाई के मूविंग एवरेज द्वारा स्मूथ किया जाता है।

- जब vol_sum निर्धारित थ्रेशोल्ड threshold से ऊपर बढ़ता है, तो खरीद सिग्नल उत्पन्न होता है; जब यह थ्रेशोल्ड से नीचे गिरता है, तो बिक्री सिग्नल उत्पन्न होता है।

- गलत संचालन को फ़िल्टर करने के लिए, खरीद संचालन केवल तभी किया जाता है जब पिछले direction कैंडल्स की समाप्ति कीमत से तुलना करने पर मूल्य का रुझान ऊपर की ओर हो। बिक्री संचालन केवल तभी किया जाता है जब मूल्य का रुझान नीचे की ओर हो।

- दो थ्रेशोल्ड सेट करें: threshold और threshold2। threshold का उपयोग ट्रेडिंग सिग्नल उत्पन्न करने के लिए किया जाता है, जबकि threshold2 का उपयोग स्टॉप-लॉस के लिए किया जाता है।

- स्टेट मशीन के माध्यम से ऑर्डर के खोलने और बंद करने के तर्क को प्रबंधित किया जाता है।

लाभ विश्लेषण

- वॉल्यूम इंडिकेटर का उपयोग बाजार में खरीद-बिक्री की शक्ति में बदलाव को पकड़ने में मदद करता है, जिससे सिग्नलों की सटीकता बढ़ती है।

- मूल्य के रुझान के साथ संयोजन करने से मूल्य में उतार-चढ़ाव के दौरान गलत सिग्नल उत्पन्न होने से बचा जा सकता है।

- दो थ्रेशोल्ड का उपयोग करके पोजीशन खोलने और स्टॉप-लॉस करने से जोखिम को बेहतर ढंग से नियंत्रित किया जा सकता है।

जोखिम विश्लेषण

- वॉल्यूम इंडिकेटर में स्वाभाविक रूप से पिछड़ेपन (लैग) होता है, जिससे मूल्य के मोड़ पर सिग्नल देर से मिल सकते हैं।

- गलत पैरामीटर सेटिंग से ट्रेडिंग की आवृत्ति बहुत अधिक हो सकती है या सिग्नल में देरी हो सकती है।

- वॉल्यूम में अचानक वृद्धि के परिदृश्य में, स्टॉप-लॉस बिंदु टूट सकता है।

इन जोखिमों को नियंत्रित करने के लिए पैरामीटर समायोजित करना, इंडिकेटर की गणना विधि को अनुकूलित करना और अन्य इंडिकेटरों के साथ पुष्टि करना संभव है।

अनुकूलन की दिशाएँ

- इंडिकेटर के पैरामीटर को स्व-अनुकूलित किया जा सकता है, जो बाजार की स्थिति के अनुसार स्वचालित रूप से समायोजित हो।

- अन्य इंडिकेटरों, जैसे प्राइस ऑसिलेटर, के साथ जोड़कर सिग्नल की पुष्टि की जा सकती है, जिससे सटीकता बढ़ेगी।

- सिग्नल निर्णय में मशीन लर्निंग मॉडल का उपयोग करके सटीकता में सुधार किया जा सकता है।

सारांश

यह रणनीति एक बेहतर वॉल्यूम ऑसिलेटर पर आधारित है, जिसमें मूल्य के रुझान का विश्लेषण शामिल है और पोजीशन खोलने तथा स्टॉप-लॉस के लिए दो थ्रेशोल्ड का उपयोग किया जाता है। कुल मिलाकर यह एक स्थिर ट्रेंड-फॉलोइंग रणनीति है। अनुकूलन की गुंजाइश मुख्य रूप से पैरामीटर समायोजन, सिग्नल फ़िल्टरिंग और स्टॉप-लॉस रणनीति में है। कुल मिलाकर, इस रणनीति में व्यावहारिक मूल्य है और आगे अनुसंधान एवं अनुकूलन के लिए यह उपयुक्त है।

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy('Volume Advanced', default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.075, currency='USD')

startP = timestamp(input(2017, "Start Year"), input(12, "Start Month"), input(17, "Start Day"), 0, 0)

end = timestamp(input(9999, "End Year"), input(1, "End Month"), input(1, "End Day"), 0, 0)- 1