कछुआ व्यापारी रणनीति पर आधारित ब्रेकआउट रिवर्सल मॉडल

अवलोकन

यह रणनीति प्रसिद्ध "कछुआ व्यापारी रणनीति" पर आधारित है, जो वर्षों से सिद्ध है। यह लॉन्ग और शॉर्ट पोजीशन के लिए संकेत भेजती है, और अधिकतम 5 पिरामिड ऑर्डर की अनुमति देती है, जिसका अर्थ है कि यह रणनीति एक ही दिशा में अधिकतम 5 ऑर्डर तक ट्रिगर कर सकती है। इसमें अच्छा जोखिम और धन प्रबंधन है।

यह ध्यान देने योग्य है कि यह रणनीति दो प्रणालियों (S1 और S2) को एक साथ काम करते हुए जोड़ती है।

रणनीति का सिद्धांत

कछुआ व्यापारियों के लिए पोजीशन का आकार जोखिम को ठीक से प्रबंधित करने के लिए बहुत महत्वपूर्ण है। यह पोजीशन साइजिंग रणनीति बाजार की अस्थिरता और खाते (लाभ और हानि) के अनुकूल होती है। यह ATR (औसत सत्य रेंज) पर आधारित है, जिसे "N" भी कहा जा सकता है। इसकी लंबाई डिफ़ॉल्ट रूप से 20 है।

खरीदी जाने वाली इकाइयों की संख्या:

unit = (percentage_to_risk/100)*account/atr*syminfo.pointvalue

आपकी जोखिम सहनशीलता के अनुसार, आप खाते का प्रतिशत बढ़ा सकते हैं, लेकिन कछुआ व्यापारी डिफ़ॉल्ट रूप से 1% रखते हैं। यदि आप कॉन्ट्रैक्ट का व्यापार करते हैं, तो इकाई को डिफ़ॉल्ट रूप से नीचे की ओर पूर्णांकित किया जाना चाहिए।

एक अतिरिक्त नियम है जो खाते का मूल्य प्रारंभिक पूंजी से कम होने पर जोखिम कम करने के लिए है: ऐसे मामले में, इकाई सूत्र में निम्नलिखित का उपयोग किया जाना चाहिए:

account := (strategy.equity-strategy.openprofit)*(strategy.equity-strategy.openprofit)/strategy.initial_capital

दो प्रणालियाँ एक साथ काम करती हैं:

ब्रेकआउट एक नया उच्च या नया निम्न बिंदु है। यदि यह एक नया उच्च है, तो हम लॉन्ग पोजीशन खोलते हैं; इसके विपरीत, यदि यह एक नया निम्न है, तो हम शॉर्ट पोजीशन में प्रवेश करते हैं।

हम एक अतिरिक्त नियम जोड़ते हैं:

यह अतिरिक्त नियम व्यापारी को मुख्य प्रवृत्ति में भाग लेने की अनुमति देता है यदि सिस्टम 1 का संकेत छूट गया हो। यदि सिस्टम 1 का संकेत छूट जाता है और अगला कैंडलस्टिक भी एक नया 20-दिवसीय ब्रेकआउट है, तो S1 संकेत नहीं देगा। हमें S2 संकेत की प्रतीक्षा करनी होगी या ऐसे कैंडलस्टिक की प्रतीक्षा करनी होगी जो नया ब्रेकआउट उत्पन्न न करे, ताकि S1 पुनः सक्रिय हो सके।

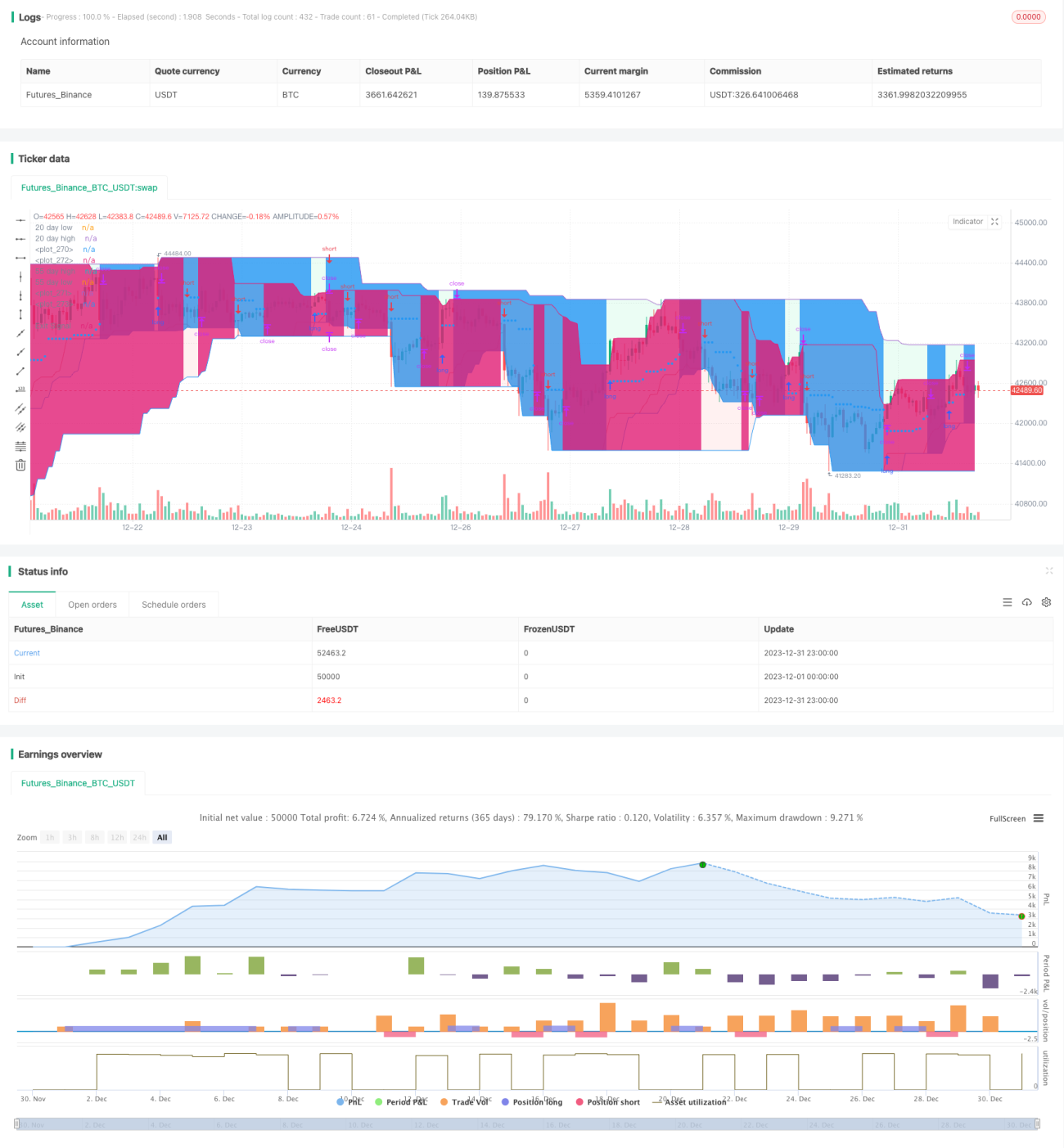

लाभ विश्लेषण

कछुआ रणनीति हमें मूल्य आंदोलन हमारे अनुकूल होने पर पोजीशन में अतिरिक्त इकाइयाँ जोड़ने की अनुमति देती है। मैंने रणनीति को कॉन्फ़िगर किया है ताकि एक ही दिशा में अधिकतम 5 ऑर्डर जोड़े जा सकें। इसलिए, यदि कीमत खरीद से बदलती है, तो हम इकाइयाँ जोड़ते हैं।

हम पहले ऑर्डर (लॉन्ग या शॉर्ट) को सबसे बड़ा ऑर्डर सेट करते हैं। बाद के पिरामिड ऑर्डर में पहले ऑर्डर की तुलना में कम इकाइयाँ होंगी।

हम पहले ऑर्डर के लिए 10% का अधिकतम स्टॉप-लॉस सेट करते हैं, जिसका अर्थ है कि आप पहले ऑर्डर के मूल्य का 10% से अधिक नहीं खोएंगे। हालांकि, चूंकि स्टॉप-लॉस 0.5 * ATR(20) तक बढ़/घट सकता है, इसलिए आपके पिरामिड ऑर्डर अधिक खो सकते हैं, और इस स्थिति में 10% से अधिक नुकसान न होने की गारंटी नहीं है। फिर भी जोखिम अच्छी तरह से प्रबंधित है क्योंकि इन ऑर्डर का मूल्य पहले ऑर्डर के मूल्य से कम है।

जोखिम विश्लेषण

इस रणनीति का सबसे बड़ा जोखिम अत्यधिक बड़ी पोजीशन है। चूंकि ऑर्डर मार्केट ऑर्डर के रूप में दिए जाते हैं, एक साथ कई बड़े मार्केट ऑर्डर देने से कोट पर बड़ा प्रभाव पड़ सकता है, जिससे बड़ी स्लिपेज हो सकती है। इससे भारी पूंजीगत हानि हो सकती है।

एक और जोखिम अनुचित धन प्रबंधन कॉन्फ़िगरेशन है। यदि स्टॉप-लॉस गलत तरीके से सेट किया गया है या अनुपात बहुत बड़ा है, तो इससे भारी नुकसान हो सकता है। अपनी जोखिम सहनशीलता के अनुसार सावधानीपूर्वक कॉन्फ़िगर करना आवश्यक है।

अनुकूलन दिशाएँ

निम्नलिखित पहलुओं में इस रणनीति को अनुकूलित किया जा सकता है:

-

रिटर्न और शार्प अनुपात पर विभिन्न मापदंडों के प्रभाव का परीक्षण किया जा सकता है, जैसे ATR अवधि, स्टॉप-लॉस का ATR गुणक, आदि। इष्टतम पैरामीटर संयोजन खोजें।

-

प्रवेश और निकास के विभिन्न नियमों का परीक्षण किया जा सकता है। जैसे कि कैंडलस्टिक पैटर्न को अतिरिक्त फ़िल्टर के रूप में उपयोग करना।

-

अन्य प्रकार के स्टॉप-लॉस, जैसे ट्रेलिंग स्टॉप, डायनेमिक स्टॉप का प्रयास किया जा सकता है। इससे स्टॉप-लॉस के टूटने की संभावना कम हो सकती है।

-

विभिन्न संख्या में पिरामिड ऑर्डर का परीक्षण किया जा सकता है। जितने अधिक ऑर्डर होंगे, लीवरेज और जोखिम उतना ही अधिक होगा। सर्वोत्तम संतुलन बिंदु खोजें।

-

विशिष्ट समयावधियों में (जैसे अमेरिकी गैर-कृषि रोजगार डेटा जारी होने से पहले) व्यापार रोकने का प्रयास किया जा सकता है, ताकि बड़ी घटनाओं के प्रभाव से बचा जा सके।

सारांश

कुल मिलाकर, यह रणनीति जोखिम-रिटर्न संतुलन में अच्छी है और मध्यम से दीर्घकालिक प्रवृत्ति व्यापार के लिए उपयुक्त है। इसके लाभों में व्यवस्थित व्यापार और नियंत्रणीय जोखिम शामिल हैं। अनुकूलन के माध्यम से, रणनीति की स्थिरता और रिटर्न को और बढ़ाया जा सकता है।

- 1