हल संकेतक और LSMA संकेतक पर आधारित प्रवृत्ति अनुसरण मात्रात्मक रणनीति

अवलोकन

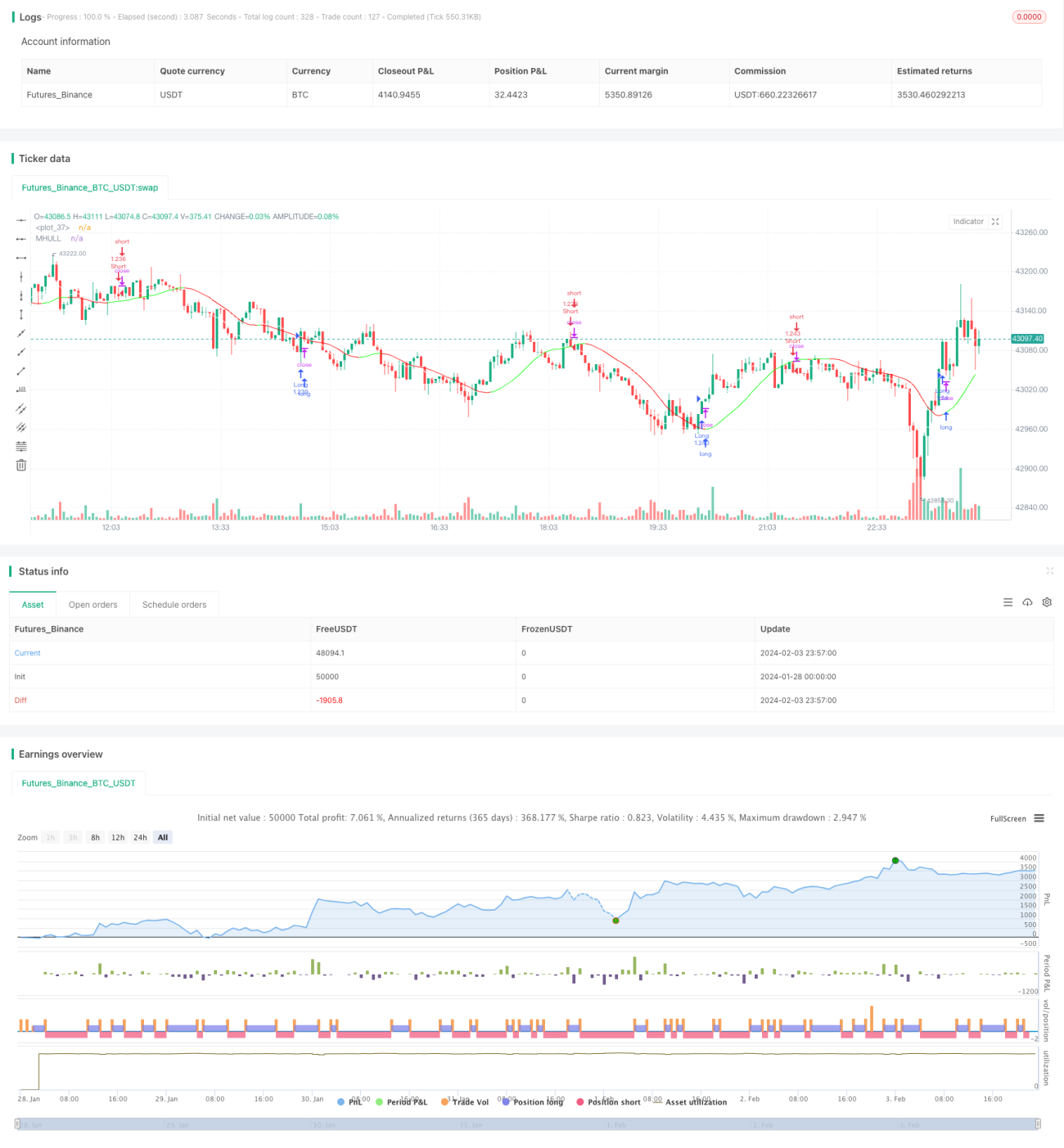

यह रणनीति हल इंडिकेटर और LSMA (न्यूनतम वर्ग चल औसत) इंडिकेटर के संयोजन के माध्यम से ट्रेंड दिशा और ट्रेंड रिवर्सल पॉइंट्स की पहचान करती है, जिससे ट्रेंड का अनुसरण किया जा सकता है। जब हल इंडिकेटर अपट्रेंड दिखाता है और LSMA हल इंडिकेटर को ऊपर से पार करता है, तो लॉन्ग एंट्री ली जाती है। जब हल इंडिकेटर डाउनट्रेंड दिखाता है और LSMA हल इंडिकेटर को नीचे से पार करता है, तो शॉर्ट एंट्री ली जाती है। यह रणनीति मध्यम से निम्न आवृत्ति ट्रेडिंग के लिए उपयुक्त है और 1 मिनट के टाइमफ्रेम पर उपयोग की जा सकती है।

रणनीति का सिद्धांत

-

हल इंडिकेटर का उपयोग मूल्य के ट्रेंड दिशा का निर्धारण करने के लिए किया जाता है। जब मध्य रेखा (MHULL) निचली रेखा (LHULL) से ऊपर होती है, तो यह अपट्रेंड को इंगित करता है; इसके विपरीत, डाउनट्रेंड को इंगित करता है।

-

LSMA इंडिकेटर का उपयोग ट्रेंड रिवर्सल पॉइंट्स की पहचान के लिए किया जाता है। जब LSMA, MHULL को ऊपर से पार करता है, तो यह अपट्रेंड के गठन या तेज होने का संकेत देता है; जब LSMA, MHULL को नीचे से पार करता है, तो यह डाउनट्रेंड के गठन या तेज होने का संकेत देता है।

-

दोनों को मिलाकर, जब हल इंडिकेटर अपट्रेंड दिखाता है (MHULL > LHULL) और LSMA, MHULL को ऊपर पार करता है, तो लॉन्ग किया जाता है; जब हल इंडिकेटर डाउनट्रेंड दिखाता है (MHULL < LHULL) और LSMA, MHULL को नीचे पार करता है, तो शॉर्ट किया जाता है।

-

स्टॉप लॉस निकटतम उतार-चढ़ाव बिंदु पर सेट किया जाता है। लॉन्ग के लिए स्टॉप लॉस निकटतम निम्नतम बिंदु पर होता है, और शॉर्ट के लिए निकटतम उच्चतम बिंदु पर होता है।

लाभ विश्लेषण

इस रणनीति के निम्नलिखित लाभ हैं:

-

हल इंडिकेटर तेज़ी से प्रतिक्रिया करता है और ट्रेंड परिवर्तनों को समय पर पकड़ लेता है; LSMA में उच्च चिकनाई होती है, जिससे रिवर्सल सिग्नल सटीक और विश्वसनीय होते हैं। दोनों का संयोजन प्रभावी होता है।

-

LSMA के क्रॉसओवर के माध्यम से हल इंडिकेटर द्वारा दिए गए झूठे सिग्नलों को फ़िल्टर किया जाता है, जिससे गलत ट्रेडों की संभावना कम हो जाती है।

-

स्टॉप लॉस के रूप में उतार-चढ़ाव बिंदु का उपयोग पूंजी की सुरक्षा को अधिकतम करता है।

-

यह मध्यम से निम्न आवृत्ति ट्रेडिंग के लिए उपयुक्त है और 1 मिनट या उससे भी कम टाइमफ्रेम पर उपयोग किया जा सकता है, जिससे अनुकूलन की व्यापकता है।

जोखिम विश्लेषण

इस रणनीति में कुछ जोखिम भी शामिल हैं:

-

साइडवेज़ बाज़ार में, हल इंडिकेटर और LSMA के बीच बार-बार क्रॉसओवर हो सकते हैं, जिससे ट्रेडिंग अत्यधिक हो जाती है। ट्रेडिंग आवृत्ति को कम करने के लिए पैरामीटरों को उचित रूप से समायोजित करना चाहिए।

-

उतार-चढ़ाव बिंदु पर सेट किया गया स्टॉप लॉस अल्पकालिक मूल्य समायोजन के कारण ट्रिगर हो सकता है, इसलिए स्टॉप लॉस के अंतराल को बढ़ाना चाहिए।

-

LSMA इंडिकेटर की विलंबता के कारण, थोड़ी गलत पहचान का जोखिम हो सकता है। इसकी पुष्टि के लिए कैंडलस्टिक पैटर्न जैसे अन्य इंडिकेटरों का उपयोग करना चाहिए।

अनुकूलन दिशा

इस रणनीति को निम्नलिखित पहलुओं से अनुकूलित किया जा सकता है:

-

हल इंडिकेटर और LSMA के पैरामीटरों को अनुकूलित करना ताकि वे विभिन्न प्रकार के उपकरणों और समय अवधियों के लिए बेहतर रूप से मेल खा सकें।

-

साइडवेज़ बाज़ार में गलत ट्रेडों से बचने के लिए अस्थिरता, ट्रेडिंग वॉल्यूम आदि पर आधारित फ़िल्टरिंग शर्तें जोड़ना।

-

ट्रेंड प्रवृत्ति का अनुमान लगाने में सहायता के लिए मशीन लर्निंग एल्गोरिदम जोड़ना।

-

गहन शिक्षण जैसी तकनीकों का उपयोग करके प्रमुख सपोर्ट और रेज़िस्टेंस क्षेत्रों का निर्धारण करना, जिससे स्टॉप लॉस अधिक उचित हो सके।

सारांश

यह रणनीति हल इंडिकेटर और LSMA के संयुक्त अनुप्रयोग के माध्यम से ट्रेंड दिशा में परिवर्तन का निर्धारण करती है और ट्रेंड-फ़ॉलोइंग ट्रेडिंग को लागू करती है। इसके लाभ सरल संचालन, त्वरित प्रतिक्रिया और मध्यम से निम्न आवृत्ति मात्रात्मक ट्रेडिंग में व्यापक अनुप्रयोग हैं। फ़िल्टरिंग शर्तों, सहायक निर्णय और स्टॉप लॉस एल्गोरिदम आदि के और अनुकूलन के माध्यम से बेहतर रणनीति परिणाम प्राप्त किए जा सकते हैं।

- 1