संवेग व्यापार की दोहरी मूविंग एवरेज क्रॉसओवर रणनीति

सारांश

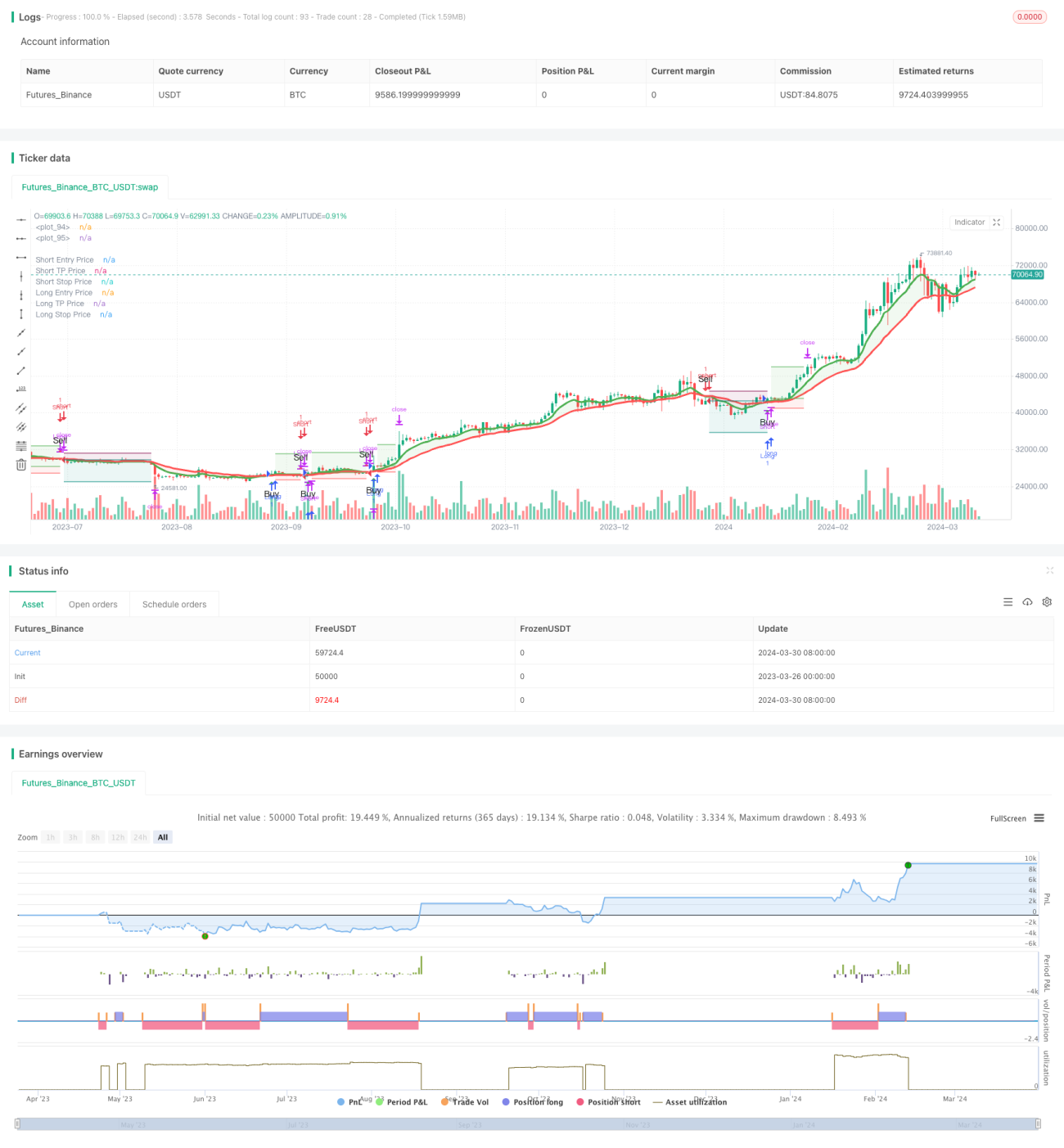

यह रणनीति बाजार के रुझान में बदलाव की पहचान करने के लिए 8-अवधि और 21-अवधि के एक्सपोनेंशियल मूविंग एवरेज (EMA) का उपयोग करती है। जब छोटी अवधि का EMA नीचे से ऊपर की ओर लंबी अवधि के EMA को पार करता है, तो खरीदारी का संकेत उत्पन्न होता है; इसके विपरीत, जब छोटी अवधि का EMA ऊपर से नीचे की ओर लंबी अवधि के EMA को पार करता है, तो बिक्री का संकेत उत्पन्न होता है। यह रणनीति रुझान उलटफेर की आगे की पुष्टि के लिए तीन लगातार उच्च निम्न (HLL) और तीन लगातार निम्न उच्च (LLH) को भी शामिल करती है। इसके अलावा, यह रणनीति जोखिम को नियंत्रित करने और लाभ को लॉक करने के लिए स्टॉप-लॉस और टेक-प्रॉफिट स्तर निर्धारित करती है।

रणनीति सिद्धांत

- मुख्य रुझान दिशा की पहचान करने के लिए 8-अवधि और 21-अवधि के EMA की गणना की जाती है।

- तीन लगातार उच्च निम्न (HLL) और तीन लगातार निम्न उच्च (LLH) की पहचान रुझान उलटफेर के शुरुआती संकेत के रूप में की जाती है।

- जब 8-अवधि का EMA नीचे से 21-अवधि के EMA को पार करता है और HLL ब्रेकआउट होता है, तो खरीदारी का संकेत उत्पन्न होता है; जब 8-अवधि का EMA ऊपर से 21-अवधि के EMA को पार करता है और LLH ब्रेकआउट होता है, तो बिक्री का संकेत उत्पन्न होता है।

- जोखिम नियंत्रण और लाभ लॉक करने के लिए स्टॉप-लॉस स्तर प्रवेश मूल्य का 5% और टेक-प्रॉफिट स्तर प्रवेश मूल्य का 16% निर्धारित किया जाता है।

- जब विपरीत संकेत उत्पन्न होता है, तो पोजीशन बंद कर दी जाती है और विपरीत दिशा में पोजीशन खोली जाती है।

रणनीति के लाभ

- EMA और मूल्य व्यवहार पैटर्न (HLL और LLH) का संयोजन रुझान की पुष्टि करता है, जिससे संकेतों की विश्वसनीयता बढ़ती है।

- स्पष्ट स्टॉप-लॉस और टेक-प्रॉफिट स्तर जोखिम नियंत्रण और लाभ लॉक करने में मदद करते हैं।

- विभिन्न समय-सीमाओं और बाजारों पर लागू, कुछ हद तक सार्वभौमिकता रखता है।

- तर्क स्पष्ट है, समझने और लागू करने में आसान है।

रणनीति के जोखिम

- अस्थिर बाजार में, बार-बार क्रॉसओवर कई झूठे संकेत उत्पन्न कर सकता है, जिससे नुकसान हो सकता है।

- निश्चित स्टॉप-लॉस और टेक-प्रॉफिट स्तर विभिन्न बाजार परिस्थितियों के अनुकूल नहीं हो पाते, जिससे संभावित अवसर लागत या अधिक नुकसान हो सकता है।

- रणनीति ऐतिहासिक डेटा पर निर्भर करती है, आकस्मिक घटनाओं या बुनियादी बदलावों के प्रति अनुकूलन क्षमता कम हो सकती है।

रणनीति अनुकूलन दिशाएँ

- विभिन्न बाजार स्थितियों के अनुकूल बनाने के लिए अनुकूली स्टॉप-लॉस और टेक-प्रॉफिट तंत्र शामिल करना, जैसे अस्थिरता (ATR) के आधार पर स्टॉप-लॉस और टेक-प्रॉफिट स्तरों को समायोजित करना।

- संकेतों को और अधिक फ़िल्टर करने और विश्वसनीयता बढ़ाने के लिए अन्य संकेतकों या कारकों जैसे वॉल्यूम, रिलेटिव स्ट्रेंथ इंडेक्स (RSI) आदि को शामिल करना।

- विशिष्ट बाजार या प्रतिभूति पर सर्वोत्तम प्रदर्शन करने वाले पैरामीटर संयोजन खोजने के लिए पैरामीटर (जैसे EMA अवधि, स्टॉप-लॉस/टेक-प्रॉफिट अनुपात आदि) का अनुकूलन करना।

- एकल ट्रेड में जोखिम जोखिम को नियंत्रित करने के लिए पोजीशन साइज़िंग जैसे जोखिम प्रबंधन उपायों को शामिल करना।

सारांश

यह रणनीति रुझान उलटफेर की पहचान करने और ट्रेडिंग सिग्नल उत्पन्न करने के लिए 8-अवधि और 21-अवधि के EMA के क्रॉसओवर को HLL और LLH मूल्य पैटर्न के साथ जोड़ती है। स्पष्ट स्टॉप-लॉस और टेक-प्रॉफिट नियम जोखिम नियंत्रण और लाभ लॉक करने में मदद करते हैं। हालाँकि, यह रणनीति अस्थिर बाजार में झूठे संकेत उत्पन्न कर सकती है, और निश्चित स्टॉप-लॉस/टेक-प्रॉफिट स्तर विभिन्न बाजार स्थितियों के अनुकूल नहीं हो सकते। आगे सुधार के लिए, अनुकूली स्टॉप-लॉस/टेक-प्रॉफिट, अन्य संकेतकों को शामिल करना, पैरामीटर अनुकूलन और जोखिम प्रबंधन उपायों पर विचार किया जा सकता है। कुल मिलाकर, यह रणनीति मोमेंटम और ट्रेंड फॉलोइंग पर आधारित एक ट्रेडिंग फ्रेमवर्क प्रदान करती है, लेकिन विशिष्ट बाजार और व्यक्तिगत प्राथमिकताओं के अनुसार समायोजित और अनुकूलित करने की आवश्यकता है।

/*backtest

start: 2023-03-26 00:00:00

end: 2024-03-31 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy('Trend Following 8&21EMA with strategy tester [ukiuro7]', overlay=true, process_orders_on_close=true, calc_on_every_tick=true, initial_capital = 10000)

//INPUTS- 1