संशोधित हल मूविंग एवरेज और इचिमोकू किन्को हियो पर आधारित मात्रात्मक ट्रेडिंग रणनीति

अवलोकन

इस रणनीति में दो तकनीकी संकेतकों को शामिल किया गया है, एक संशोधित हल चलती औसत ((HMA) और एक दृष्टि संतुलन ((Ichimoku Kinko Hyo) बाजार के मध्यम और दीर्घकालिक रुझानों को पकड़ने के लिए। रणनीति का मुख्य विचार एचएमए का उपयोग करना है और एक दृष्टि संतुलन में एक आधार रेखा ((किजुन सेन) के साथ क्रॉस सिग्नल का उपयोग करना है, जबकि एक दृष्टि संतुलन के बादल ((कुमो) को फ़िल्टर शर्त के रूप में जोड़ना है, ताकि बाजार की प्रवृत्ति की दिशा का आकलन किया जा सके और व्यापार किया जा सके।

रणनीति सिद्धांत

- संशोधित हल चल औसत (HMA) की गणना करें

- WMA ((वजनित चलती औसत) की गणना करें और एक दोहरी चिकनाई प्रक्रिया करें, जो एक संशोधित HMA प्राप्त करता है

- पहले नजर में संतुलित सूचकांकों की गणना

- टर्नओवर लाइन की गणना करें (टेन्कन सेन), बेंचमार्क लाइन (किजुन सेन), अग्रणी अपलाइन (सेन्को स्पैन ए) और अग्रणी डाउनलाइन (सेन्को स्पैन बी)

- व्यापार संकेत उत्पन्न करें

- जब HMA पर बेंचमार्क लाइन को पार करता है और क्लोज-आउट मूल्य बादल के ऊपर होता है, तो एक बहुसंकेत उत्पन्न होता है

- जब HMA नीचे बेंचमार्क लाइन को पार करता है और क्लोज-आउट मूल्य बादल के नीचे होता है, तो एक कम संकेत उत्पन्न होता है

- लेनदेन निष्पादित करें

- अधिक या कम संकेतों के आधार पर संबंधित ट्रेडिंग ऑपरेशन

- व्यापार से बाहर निकलें

- जब HMA विपरीत दिशा में बेंचमार्क लाइन को पार करता है, तो वर्तमान स्थिति से बाहर निकलें

रणनीतिक लाभ

- एचएमए और एक नजर में संतुलन के संयोजन के साथ दो प्रभावी ट्रेंड ट्रैकिंग संकेतकों के साथ, बाजार की प्रवृत्तियों को बेहतर ढंग से पकड़ने में सक्षम

- फ़िल्टर के रूप में एक संतुलित बादल का उपयोग करना, झूठे संकेतों को कम करने और ट्रेडों को जीतने की संभावना को बढ़ा सकता है

- संशोधित एचएमए में पारंपरिक चलती औसत की तुलना में तेजी से प्रतिक्रिया और कम विलंबता है, जो बाजार में बदलाव को समय पर प्रतिबिंबित करने में सक्षम है

- स्पष्ट रणनीति तर्क, आसानी से समझने और लागू करने के लिए, विभिन्न बाजारों और समय अवधि के लिए

रणनीतिक जोखिम

- बाजार में उतार-चढ़ाव या अनिश्चित रुझान के दौरान, यह रणनीति अधिक झूठे संकेत दे सकती है, जिससे अक्सर व्यापार और धन की हानि होती है।

- रणनीति के पैरामीटर सेटिंग्स का व्यापार के परिणामों पर अधिक प्रभाव पड़ता है, विभिन्न पैरामीटर संयोजनों के कारण अलग-अलग प्रदर्शन हो सकता है

- इस रणनीति में बाजार की आकस्मिक घटनाओं और तर्कहीन व्यवहार को ध्यान में नहीं रखा गया है जो चरम बाजार स्थितियों में अधिक जोखिम पैदा कर सकता है

रणनीति अनुकूलन दिशा

- सिग्नल की विश्वसनीयता और स्थिरता बढ़ाने के लिए अन्य तकनीकी संकेतकों या बाजार की भावना के संकेतकों को शामिल करना

- अनुकूलन रणनीति पैरामीटर, जैसे कि मशीन सीखने या आनुवंशिक एल्गोरिदम के माध्यम से सर्वोत्तम पैरामीटर संयोजन की तलाश करना

- जोखिम प्रबंधन मॉड्यूल को शामिल करने पर विचार करें, जैसे कि स्टॉप लॉस स्टॉप, पोजीशन मैनेजमेंट आदि, ताकि रणनीति के जोखिम को नियंत्रित किया जा सके

- विभिन्न बाजारों और समय अवधि की विशेषताओं के अनुसार रणनीतियों के लिए लक्षित समायोजन और अनुकूलन

संक्षेप

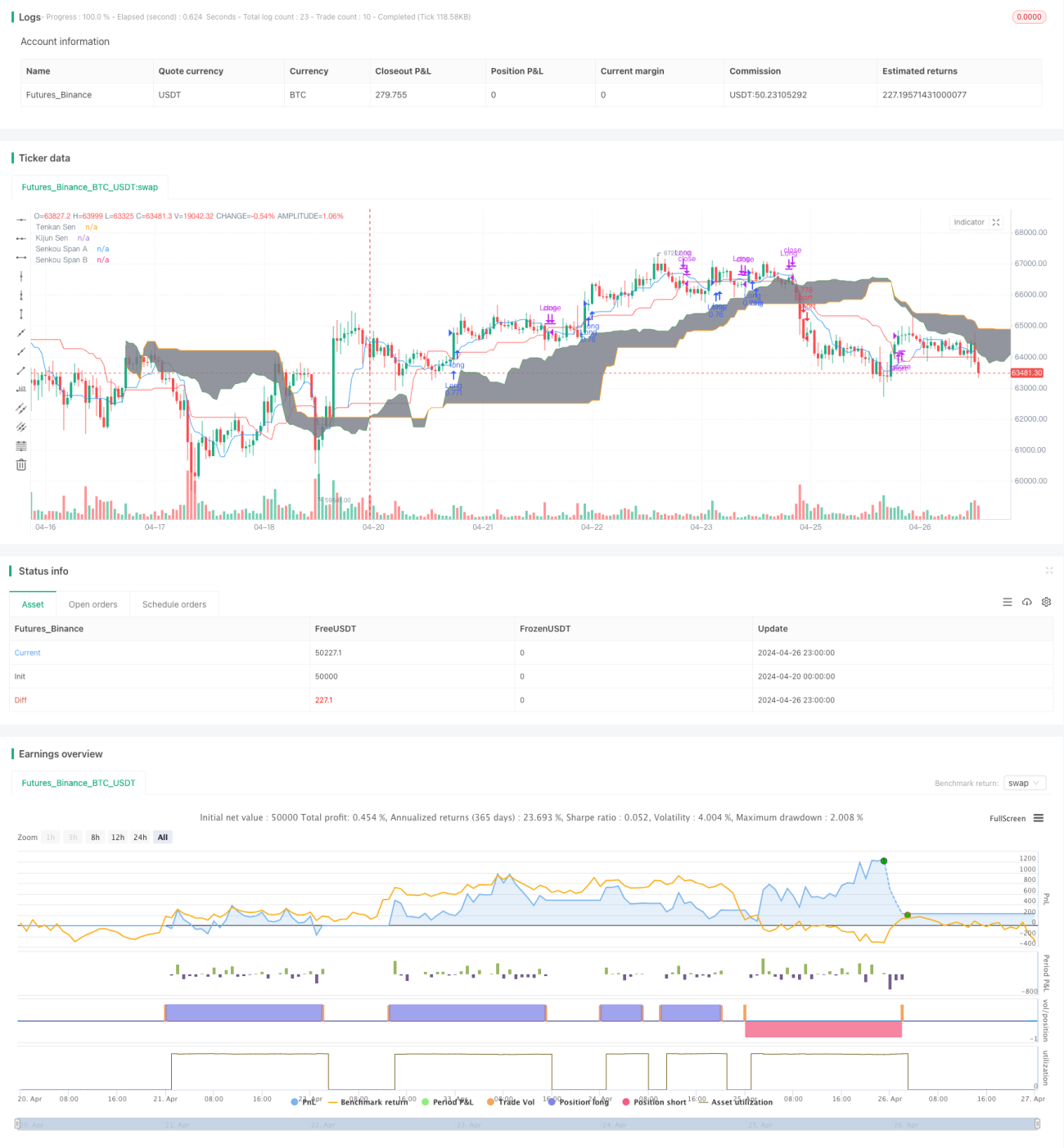

इस रणनीति में एक संशोधित हल चलती औसत और एक दृष्टि संतुलन के साथ एक अपेक्षाकृत मजबूत प्रवृत्ति ट्रैक ट्रेडिंग प्रणाली का निर्माण किया गया है। रणनीति तर्क स्पष्ट है, इसे लागू करना आसान है, लेकिन इसके कुछ फायदे भी हैं। हालांकि, रणनीति का प्रदर्शन अभी भी बाजार की स्थितियों और पैरामीटर सेटिंग्स से प्रभावित है, और आगे अनुकूलन और सुधार की आवश्यकता है। वास्तविक अनुप्रयोगों में, रणनीति को विशिष्ट बाजार विशेषताओं और जोखिम वरीयताओं के साथ उचित रूप से समायोजित और प्रबंधित किया जाना चाहिए ताकि बेहतर व्यापार परिणाम प्राप्त किए जा सकें।

/*backtest

start: 2024-04-20 00:00:00

end: 2024-04-27 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("Hull MA_X + Ichimoku Kinko Hyo Strategy", shorttitle="HMX+IKHS", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100, pyramiding=0)

// Hull Moving Average Parameters- 1