औसत दिशात्मक सूचकांक फिल्टर पर आधारित मूविंग औसत अस्वीकृति रणनीति

अवलोकन

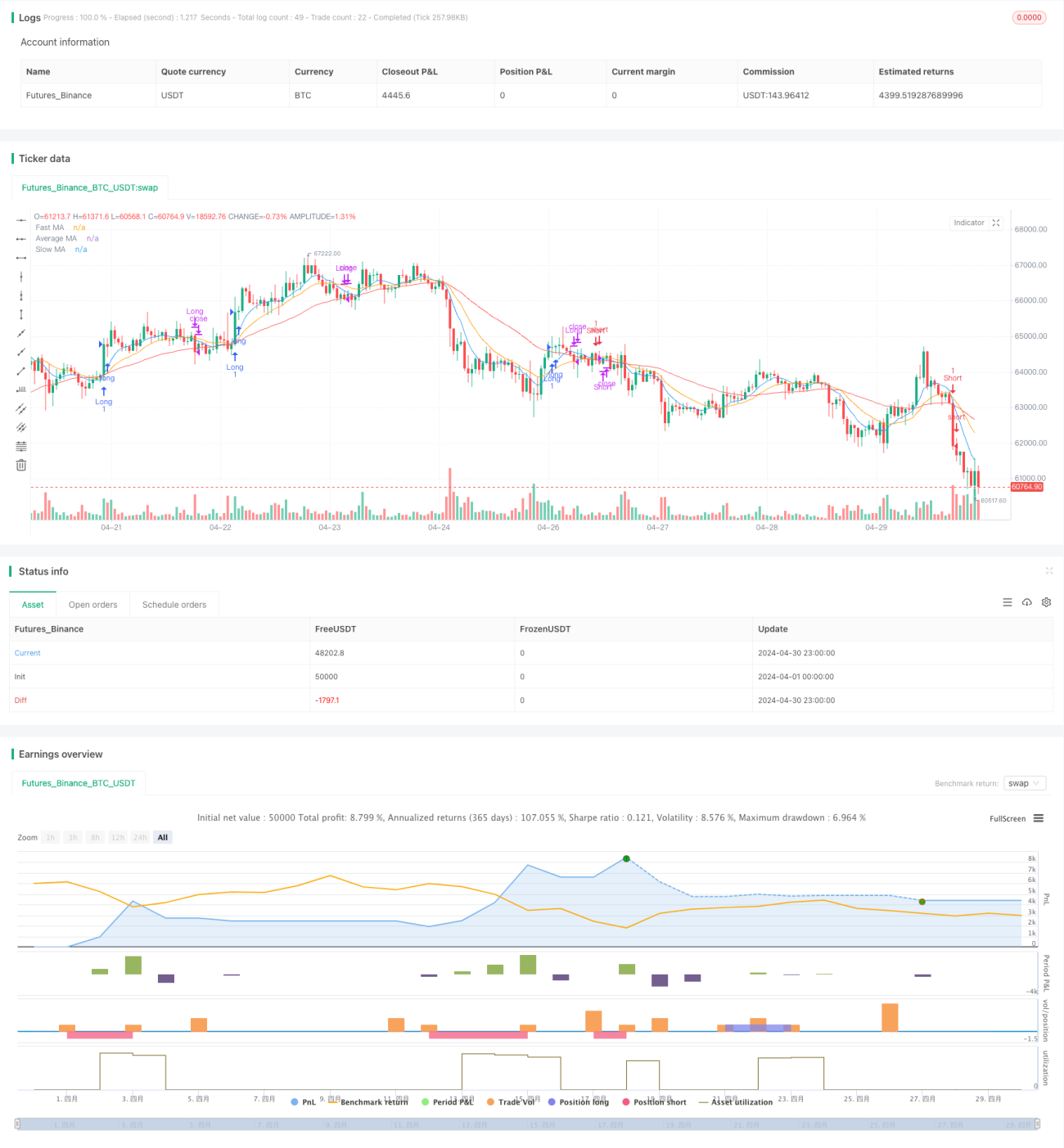

यह रणनीति प्राथमिक ट्रेडिंग सिग्नल के रूप में कई मूविंग एवरेज (MA) का उपयोग करती है, और फ़िल्टर के रूप में औसत दिशात्मक सूचकांक (ADX) को जोड़ती है। रणनीति का मुख्य विचार तेज़ MA, धीमी MA और औसत MA के संबंध की तुलना करके संभावित लॉन्ग और शॉर्ट अवसरों की पहचान करना है। साथ ही, पर्याप्त ट्रेंड मजबूती वाले बाजार परिवेश को फ़िल्टर करने के लिए ADX संकेतक का उपयोग किया जाता है, जिससे ट्रेडिंग सिग्नलों की विश्वसनीयता बढ़ती है।

रणनीति सिद्धांत

- तेज़ MA, धीमी MA और औसत MA की गणना करें।

- बंद मूल्य और धीमी MA के संबंध की तुलना करके संभावित लॉन्ग और शॉर्ट स्तरों की पहचान करें।

- बंद मूल्य और तेज़ MA के संबंध की तुलना करके लॉन्ग और शॉर्ट स्तरों की पुष्टि करें।

- ट्रेंड की मजबूती मापने के लिए ADX संकेतक की मैन्युअल गणना करें।

- जब तेज़ MA औसत MA को ऊपर की ओर क्रॉस करे, ADX निर्धारित सीमा से अधिक हो, और लॉन्ग स्तर की पुष्टि हुई हो, तो लॉन्ग एंट्री सिग्नल उत्पन्न होता है।

- जब तेज़ MA औसत MA को नीचे की ओर क्रॉस करे, ADX निर्धारित सीमा से अधिक हो, और शॉर्ट स्तर की पुष्टि हुई हो, तो शॉर्ट एंट्री सिग्नल उत्पन्न होता है।

- जब बंद मूल्य धीमी MA को नीचे की ओर क्रॉस करता है, तो लॉन्ग एग्ज़िट सिग्नल उत्पन्न होता है; जब बंद मूल्य धीमी MA को ऊपर की ओर क्रॉस करता है, तो शॉर्ट एग्ज़िट सिग्नल उत्पन्न होता है।

रणनीति के लाभ

- कई MA का उपयोग बाजार के रुझान और गति में परिवर्तनों को अधिक व्यापक रूप से कैप्चर करने में मदद करता है।

- तेज़ MA, धीमी MA और औसत MA के संबंध की तुलना करके संभावित ट्रेडिंग अवसरों की पहचान की जा सकती है।

- ADX संकेतक को फ़िल्टर के रूप में उपयोग करने से साइडवे बाजार में अत्यधिक गलत सिग्नलों से बचा जा सकता है, जिससे ट्रेडिंग सिग्नलों की विश्वसनीयता बढ़ती है।

- रणनीति का तर्क स्पष्ट है, इसे समझना और लागू करना आसान है।

रणनीति के जोखिम

- स्पष्ट रुझान न होने या बाजार में साइडवे (दायरे में) स्थिति होने पर, यह रणनीति बार-बार गलत सिग्नल उत्पन्न कर सकती है, जिससे बार-बार ट्रेडिंग और नुकसान हो सकता है।

- रणनीति MA और ADX जैसे लैगिंग संकेतकों पर निर्भर करती है, जो शुरुआती ट्रेंड निर्माण के कुछ अवसरों को चूक सकते हैं।

- रणनीति के पैरामीटर सेटिंग्स (जैसे MA लंबाई और ADX सीमा) का रणनीति प्रदर्शन पर बड़ा प्रभाव पड़ता है, और विभिन्न बाजारों और उपकरणों के अनुसार अनुकूलन की आवश्यकता होती है।

रणनीति अनुकूलन दिशाएँ

- ट्रेडिंग सिग्नलों की विश्वसनीयता और विविधता बढ़ाने के लिए अन्य तकनीकी संकेतकों जैसे RSI, MACD आदि को शामिल करने पर विचार करें।

- विभिन्न बाजार परिवेश के लिए बदलते बाजार के अनुकूल अलग-अलग पैरामीटर संयोजन सेट किए जा सकते हैं।

- संभावित नुकसान को नियंत्रित करने के लिए स्टॉप-लॉस और पोजीशन मैनेजमेंट जैसे जोखिम प्रबंधन उपाय लागू करें।

- अधिक व्यापक बाजार दृष्टिकोण प्राप्त करने के लिए आर्थिक डेटा, नीति परिवर्तनों जैसे मौलिक विश्लेषण को शामिल करें।

सारांश

औसत दिशात्मक सूचकांक फ़िल्टर पर आधारित मूविंग एवरेज रिजेक्शन रणनीति संभावित ट्रेडिंग अवसरों की पहचान करने और निम्न-गुणवत्ता वाले ट्रेडिंग सिग्नलों को फ़िल्टर करने के लिए कई MA और ADX संकेतक का उपयोग करती है। इस रणनीति का तर्क स्पष्ट है, इसे समझना और लागू करना आसान है, लेकिन वास्तविक अनुप्रयोग में बाजार परिवेश में बदलावों पर ध्यान देना आवश्यक है, और अन्य तकनीकी संकेतकों तथा जोखिम प्रबंधन उपायों के साथ मिलकर अनुकूलन करना चाहिए।

- 1