MACD और R:R अनुपात इंट्राडे सीमित अभिसरण रणनीति

अवलोकन

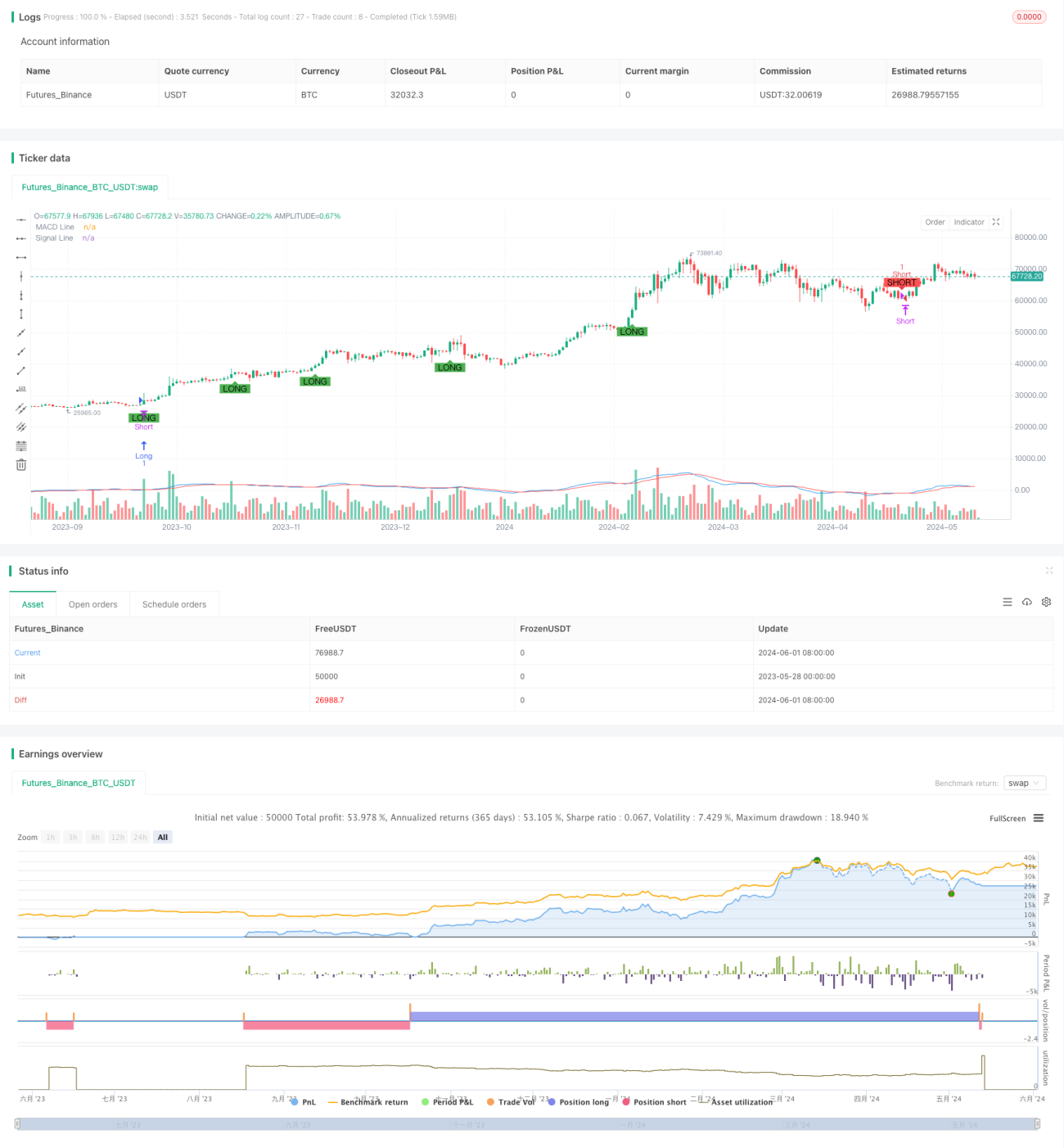

यह रणनीति MACD इंडिकेटर के अभिसरण और विचलन पर आधारित है ताकि ट्रेडिंग सिग्नल उत्पन्न किए जा सकें। जब MACD रेखा और सिग्नल रेखा क्रॉस करती हैं, और MACD रेखा का मान 1.5 से अधिक या -1.5 से कम होता है, तो क्रमशः लॉन्ग और शॉर्ट सिग्नल उत्पन्न होते हैं। साथ ही, रणनीति निश्चित टेक-प्रॉफिट और स्टॉप-लॉस बिंदु निर्धारित करती है, और जोखिम-लाभ अनुपात (R:R) की अवधारणा शामिल करती है। इसके अतिरिक्त, यह रणनीति दिन के अंदर अधिकतम हानि और अधिकतम लाभ की सीमा, साथ ही अधिक सख्त ट्रेलिंग स्टॉप उपायों का उपयोग करती है ताकि जोखिम को बेहतर ढंग से नियंत्रित किया जा सके।

रणनीति सिद्धांत

- MACD इंडिकेटर की MACD रेखा और सिग्नल रेखा की गणना की जाती है।

- MACD रेखा और सिग्नल रेखा के क्रॉसओवर की पहचान की जाती है, साथ ही यह देखा जाता है कि MACD रेखा का मान निर्दिष्ट सीमा (1.5 और -1.5) से अधिक है या नहीं।

- जब लॉन्ग सिग्नल होता है, तो लॉन्ग पोजीशन खोली जाती है, जिसमें टेक-प्रॉफिट मूल्य वर्तमान उच्चतम मूल्य + 600 न्यूनतम मूल्य परिवर्तन इकाइयों पर और स्टॉप-लॉस मूल्य वर्तमान न्यूनतम मूल्य - 100 न्यूनतम मूल्य परिवर्तन इकाइयों पर सेट किया जाता है।

- जब शॉर्ट सिग्नल होता है, तो शॉर्ट पोजीशन खोली जाती है, जिसमें टेक-प्रॉफिट मूल्य वर्तमान न्यूनतम मूल्य - 600 न्यूनतम मूल्य परिवर्तन इकाइयों पर और स्टॉप-लॉस मूल्य वर्तमान उच्चतम मूल्य + 100 न्यूनतम मूल्य परिवर्तन इकाइयों पर सेट किया जाता है।

- ट्रेलिंग स्टॉप तर्क लागू किया जाता है: जब मूल्य ओपनिंग मूल्य से (लॉन्ग के लिए) बढ़ता है या (शॉर्ट के लिए) घटता है, जो 300 न्यूनतम मूल्य परिवर्तन इकाइयों से अधिक होता है, तो स्टॉप-लॉस मूल्य को ओपनिंग मूल्य + (क्लोज़िंग मूल्य - ओपनिंग मूल्य - 300) (लॉन्ग) या ओपनिंग मूल्य - (ओपनिंग मूल्य - क्लोज़िंग मूल्य - 300) (शॉर्ट) पर स्थानांतरित कर दिया जाता है।

- दिन के अंदर अधिकतम हानि और अधिकतम लाभ की सीमा निर्धारित की जाती है: जब दिन की हानि 600 न्यूनतम मूल्य परिवर्तन इकाइयों तक पहुँचती है या लाभ 1800 न्यूनतम मूल्य परिवर्तन इकाइयों तक पहुँचता है, तो सभी पोजीशन बंद कर दी जाती हैं।

लाभ विश्लेषण

- MACD इंडिकेटर और मूल्य सीमा शर्तों का संयोजन, शोर सिग्नलों को प्रभावी ढंग से फ़िल्टर करता है।

- निश्चित जोखिम-लाभ अनुपात (R:R) हर व्यापार में जोखिम और लाभ को नियंत्रणीय बनाता है।

- ट्रेलिंग स्टॉप तर्क प्रवृत्ति बनने के बाद लाभ की रक्षा करने और ड्रॉडाउन को कम करने में मदद करता है।

- दिन के अंदर अधिकतम हानि और लाभ सीमा एक दिन के जोखिम को नियंत्रित करने में मदद करती है, अत्यधिक हानि या लाभ के बाद ड्रॉडाउन से बचाती है।

जोखिम विश्लेषण

- MACD इंडिकेटर में पिछड़ापन है, जिससे सिग्नल में देरी या गलत सिग्नल आ सकते हैं।

- निश्चित टेक-प्रॉफिट और स्टॉप-लॉस बिंदु विभिन्न बाजार स्थितियों के अनुकूल नहीं हो सकते, और अस्थिर बाजार में बार-बार स्टॉप-लॉस ट्रिगर हो सकता है।

- ट्रेलिंग स्टॉप तर्क प्रवृत्ति के उलटने पर समय पर स्टॉप-लॉस नहीं कर सकता, जिससे लाभ वापस चला जाता है।

- दिन के अंदर अधिकतम हानि और लाभ सीमा रणनीति को स्पष्ट दैनिक प्रवृत्ति के दौरान समय से पहले पोजीशन बंद करने पर मजबूर कर सकती है, जिससे संभावित लाभ छूट सकता है।

अनुकूलन दिशाएँ

- सिग्नल की पुष्टि के लिए एकाधिक समय-सीमा वाले MACD इंडिकेटर का उपयोग करने पर विचार करें, जिससे सिग्नल सटीकता बढ़ेगी।

- बाजार की अस्थिरता के अनुसार टेक-प्रॉफिट और स्टॉप-लॉस बिंदुओं को गतिशील रूप से समायोजित करें, ताकि विभिन्न बाजार स्थितियों के अनुकूल हो सके।

- ट्रेलिंग स्टॉप तर्क को अनुकूलित करें, जैसे ATR इंडिकेटर के आधार पर ट्रेलिंग स्टॉप दूरी निर्धारित करना, ताकि मूल्य अस्थिरता को बेहतर ढंग से संभाला जा सके।

- दिन के अंदर अधिकतम हानि और लाभ सीमा के पैरामीटर अनुकूलित करें, उपयुक्त सीमा मान खोजें जो जोखिम को नियंत्रित करते हुए प्रवृत्ति को पकड़ने में मदद करें।

सारांश

यह रणनीति MACD इंडिकेटर के अभिसरण और विचलन के आधार पर ट्रेडिंग सिग्नल उत्पन्न करती है, और साथ ही जोखिम-लाभ अनुपात, ट्रेलिंग स्टॉप और दैनिक सीमा जैसे जोखिम नियंत्रण उपायों को शामिल करती है। हालाँकि यह रणनीति कुछ हद तक प्रवृत्तियों को पकड़ सकती है और जोखिम को नियंत्रित कर सकती है, फिर भी इसमें अनुकूलन और सुधार की गुंजाइश है। भविष्य में सिग्नल पुष्टि, टेक-प्रॉफिट/स्टॉप-लॉस, ट्रेलिंग स्टॉप और दैनिक सीमा जैसे आयामों पर अनुकूलन किया जा सकता है, ताकि अधिक स्थिर और महत्वपूर्ण रिटर्न प्राप्त किया जा सके।

- 1