गतिशील जोखिम प्रबंधन और निश्चित लाभ पर आधारित उन्नत उचित मूल्य अंतर पहचान रणनीति

सारांश

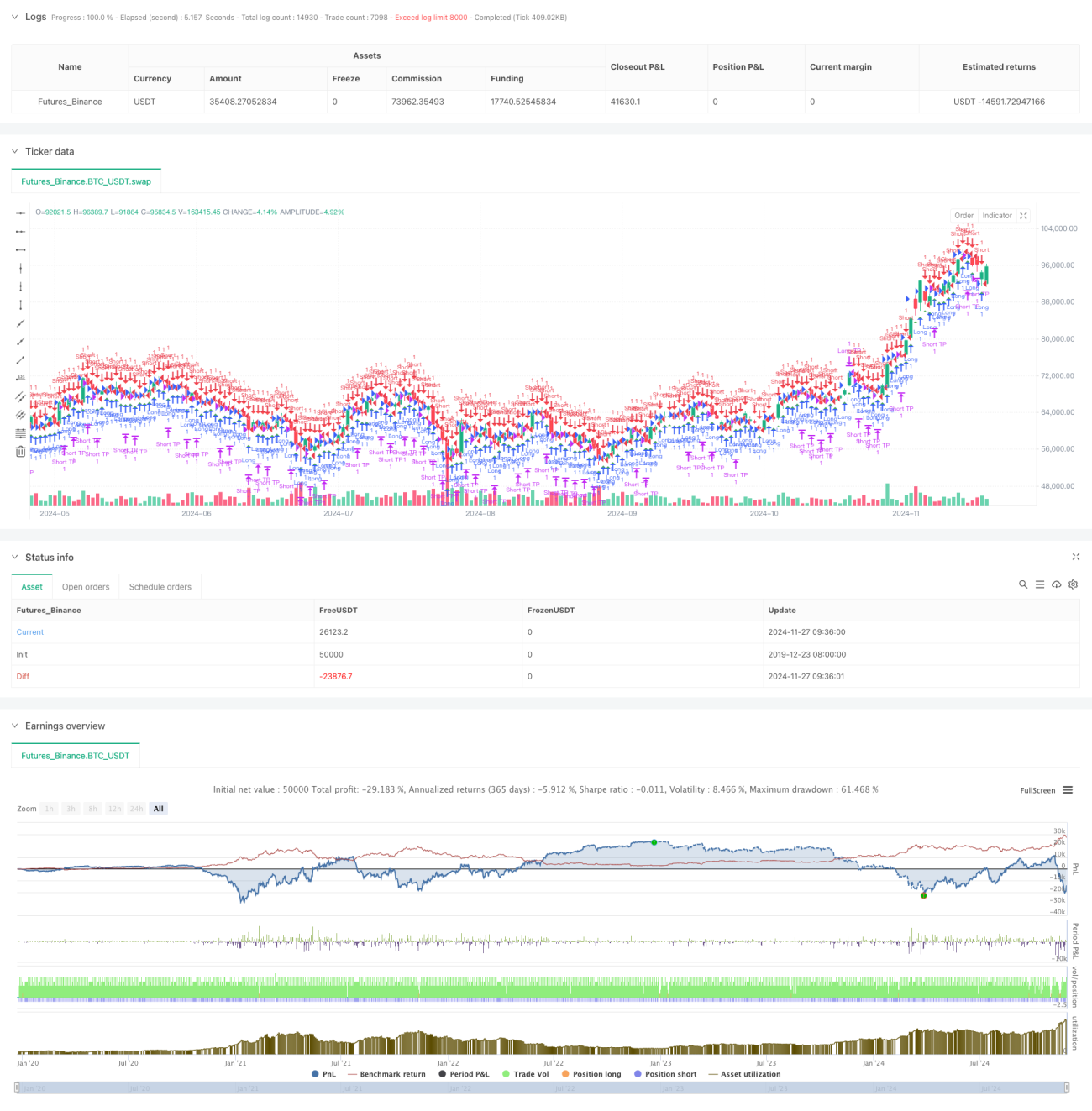

यह एक फेयर वैल्यू गैप (FVG) पर आधारित ट्रेडिंग रणनीति है, जिसमें गतिशील जोखिम प्रबंधन और निश्चित लाभ लक्ष्य शामिल है। यह रणनीति 15 मिनट के टाइमफ्रेम पर काम करती है और बाजार में मूल्य अंतराल की पहचान करके संभावित ट्रेडिंग अवसरों को कैप्चर करती है। बैकटेस्ट डेटा के अनुसार, नवंबर 2023 से अगस्त 2024 की अवधि में, इस रणनीति ने 284.40% का शुद्ध रिटर्न दिया, कुल 153 ट्रेड पूरे किए, जिसमें लाभप्रदता दर 71.24% और लाभ कारक 2.422 रहा।

रणनीति सिद्धांत

रणनीति का मूल लगातार तीन कैंडल्स के बीच मूल्य संबंधों की निगरानी करके फेयर वैल्यू गैप की पहचान करना है। विशेष रूप से:

- लॉन्ग FVG निर्माण की शर्त: जब वर्तमान कैंडल का उच्चतम मूल्य पिछली दो कैंडल्स के न्यूनतम मूल्य से कम हो

- शॉर्ट FVG निर्माण की शर्त: जब वर्तमान कैंडल का न्यूनतम मूल्य पिछली दो कैंडल्स के उच्चतम मूल्य से अधिक हो

- एंट्री सिग्नल FVG थ्रेशोल्ड पैरामीटर द्वारा नियंत्रित होता है, जो केवल तब ट्रिगर होता है जब गैप का आकार मूल्य के एक निश्चित प्रतिशत से अधिक हो

- जोखिम नियंत्रण खाता इक्विटी के एक निश्चित अनुपात (1%) को स्टॉप लॉस मानक के रूप में उपयोग करता है

- लाभ लक्ष्य एक निश्चित पिप मान (50 पिप्स) पर सेट किया गया है

रणनीति के लाभ

- जोखिम प्रबंधन वैज्ञानिक और उचित है: खाता इक्विटी अनुपात पर आधारित स्टॉप लॉस गतिशील जोखिम नियंत्रण सक्षम बनाता है

- ट्रेडिंग नियम स्पष्ट हैं: निश्चित लाभ लक्ष्य का उपयोग, व्यक्तिपरक निर्णय से बचा जाता है

- बेहतरीन प्रदर्शन: उच्च लाभप्रदता दर और लाभ कारक रणनीति की अच्छी स्थिरता दर्शाते हैं

- सरल कार्यान्वयन: कोड तर्क स्पष्ट है, समझने और बनाए रखने में आसान है

- उच्च अनुकूलनशीलता: विभिन्न बाजार स्थितियों के अनुकूल पैरामीटर समायोजन किया जा सकता है

रणनीति जोखिम

- बाजार अस्थिरता जोखिम: उच्च अस्थिरता वाले बाजार में, निश्चित पिप लाभ लक्ष्य पर्याप्त लचीला नहीं हो सकता

- स्लिपेज जोखिम: बार-बार ट्रेडिंग से उच्च स्लिपेज लागत हो सकती है

- पैरामीटर निर्भरता: रणनीति का प्रदर्शन FVG थ्रेशोल्ड सेटिंग पर अत्यधिक निर्भर करता है

- झूठे ब्रेकआउट का जोखिम: कुछ FVG सिग्नल झूठे ब्रेकआउट हो सकते हैं, जिसके लिए अतिरिक्त पुष्टिकरण संकेतक की आवश्यकता होती है

- पूंजी प्रबंधन जोखिम: लगातार घाटे के दौरान निश्चित अनुपात स्टॉप लॉस से पूंजी तेजी से घट सकती है

रणनीति अनुकूलन दिशाएँ

- बाजार अस्थिरता संकेतक शामिल करें, लाभ लक्ष्य को गतिशील रूप से समायोजित करें

- ट्रेंड फिल्टर जोड़ें, रेंज बाजार में ट्रेडिंग से बचें

- मल्टी-टाइमफ्रेम पुष्टिकरण तंत्र विकसित करें

- पोजीशन प्रबंधन एल्गोरिदम अनुकूलित करें, फ्लोटिंग पोजीशन सिस्टम शामिल करें

- ट्रेडिंग समय फिल्टर जोड़ें, उच्च अस्थिरता अवधि से बचें

- सिग्नल तीव्रता रेटिंग सिस्टम विकसित करें, उच्च गुणवत्ता वाले ट्रेडिंग अवसरों का चयन करें

निष्कर्ष

यह रणनीति फेयर वैल्यू गैप सिद्धांत और वैज्ञानिक जोखिम प्रबंधन विधियों को मिलाकर अच्छे ट्रेडिंग परिणाम दिखाती है। रणनीति की उच्च लाभप्रदता दर और स्थिर लाभ कारक इसके व्यावहारिक मूल्य को इंगित करते हैं। सुझाए गए अनुकूलन दिशाओं के माध्यम से, रणनीति में और सुधार की गुंजाइश है। ट्रेडर्स को लाइव ट्रेडिंग में उपयोग करने से पहले पर्याप्त पैरामीटर अनुकूलन और बैकटेस्ट सत्यापन करने की सलाह दी जाती है।

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-28 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Fair Value Gap Strategy with % SL and Fixed TP", overlay=true, initial_capital=500, default_qty_type=strategy.fixed, default_qty_value=1)

// Parameters- 1