दोहरी श्रृंखला मिक्स्ड मोमेंटम मूविंग एवरेज ट्रैकिंग ट्रेडिंग सिस्टम

अवलोकन

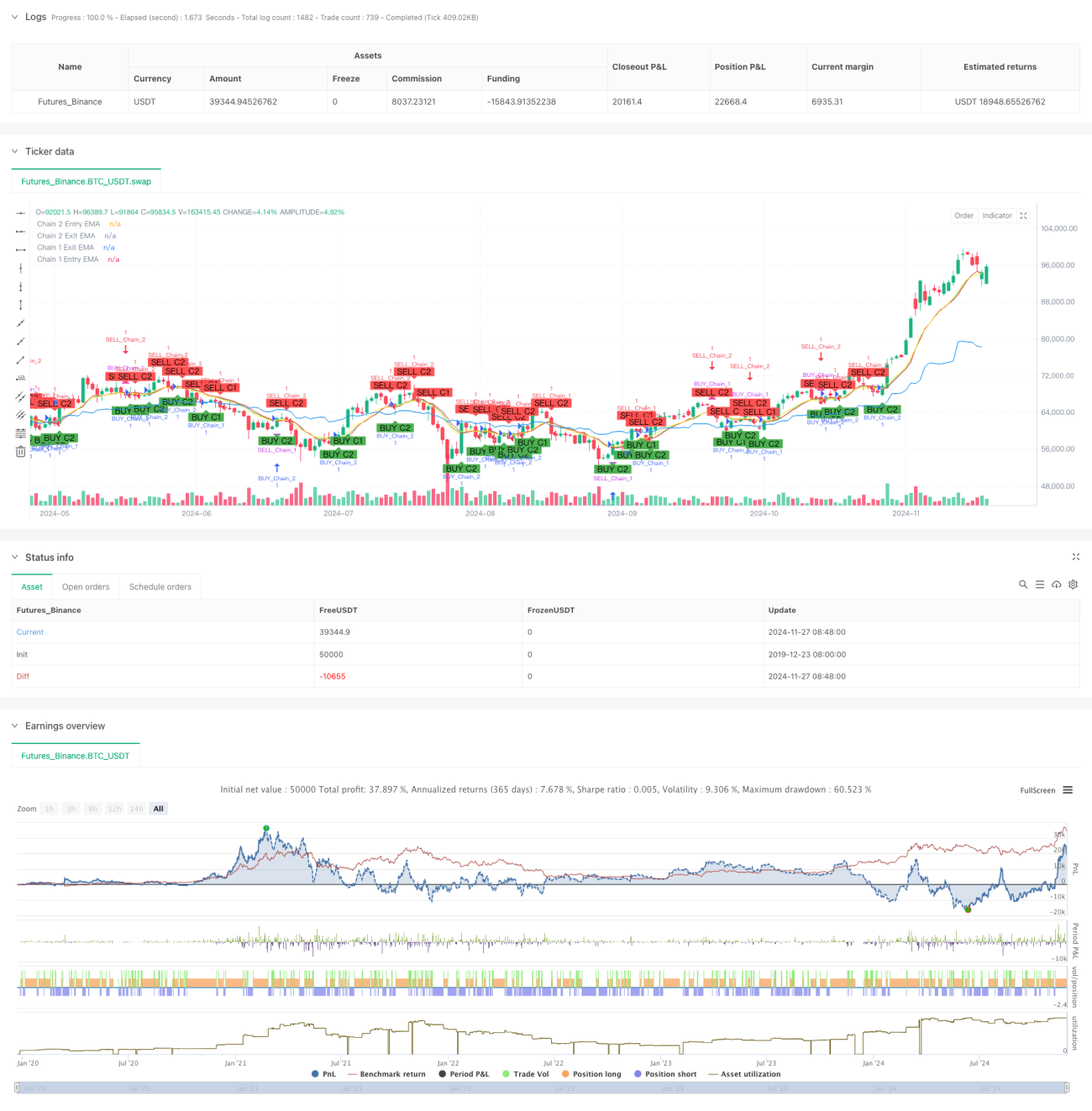

यह रणनीति एक्सपोनेंशियल मूविंग एवरेज (EMA) पर आधारित एक नवीन ट्रेडिंग सिस्टम है, जो विभिन्न समय-सीमाओं पर दो स्वतंत्र ट्रेडिंग चेन स्थापित करके बाजार के अवसरों को कैप्चर करती है। यह रणनीति दीर्घकालिक प्रवृत्ति अनुसरण और अल्पकालिक मोमेंटम ट्रेडिंग के लाभों को एकीकृत करती है, और साप्ताहिक, दैनिक, 12-घंटे और 9-घंटे जैसी कई समय-सीमाओं पर EMA क्रॉसओवर से ट्रेडिंग सिग्नल उत्पन्न करती है, जिससे बाजार का बहुआयामी विश्लेषण और समझ संभव होती है।

रणनीति का सिद्धांत

रणनीति में दोहरी चेन डिज़ाइन का उपयोग किया गया है, प्रत्येक चेन का अपना अद्वितीय प्रवेश और निकास तर्क है:

चेन 1 (दीर्घकालिक प्रवृत्ति) साप्ताहिक और दैनिक समय-सीमा का उपयोग करती है:

- प्रवेश संकेत: जब साप्ताहिक समय-सीमा पर बंद मूल्य EMA को ऊपर से पार करता है, तो लॉन्ग पोजीशन का संकेत उत्पन्न होता है।

- निकास संकेत: जब दैनिक समय-सीमा पर बंद मूल्य EMA को नीचे से पार करता है, तो पोजीशन बंद करने का संकेत उत्पन्न होता है।

- डिफ़ॉल्ट EMA अवधि 10 है, जिसे आवश्यकतानुसार समायोजित किया जा सकता है।

चेन 2 (अल्पकालिक मोमेंटम) 12-घंटे और 9-घंटे की समय-सीमा का उपयोग करती है:

- प्रवेश संकेत: जब 12-घंटे की समय-सीमा पर बंद मूल्य EMA को ऊपर से पार करता है, तो लॉन्ग पोजीशन का संकेत उत्पन्न होता है।

- निकास संकेत: जब 9-घंटे की समय-सीमा पर बंद मूल्य EMA को नीचे से पार करता है, तो पोजीशन बंद करने का संकेत उत्पन्न होता है।

- डिफ़ॉल्ट EMA अवधि 9 है, जिसे आवश्यकतानुसार समायोजित किया जा सकता है।

रणनीति के लाभ

- बहुआयामी बाजार विश्लेषण: विभिन्न समय-सीमाओं के संयोजन के माध्यम से बाजार की प्रवृत्तियों की व्यापक समझ।

- उच्च लचीलापन: दोनों चेन को स्वतंत्र रूप से सक्षम या अक्षम किया जा सकता है, जो विभिन्न ट्रेडिंग शैलियों के अनुकूल है।

- बेहतर जोखिम नियंत्रण: एकाधिक समय-सीमा पुष्टिकरण का उपयोग करके गलत संकेतों का जोखिम कम होता है।

- उच्च पैरामीटर समायोजन क्षमता: EMA अवधि और समय-सीमा दोनों को आवश्यकतानुसार संशोधित किया जा सकता है।

- उन्नत बैकटेस्टिंग क्षमताएं: रणनीति सत्यापन और अनुकूलन के लिए अंतर्निहित बैकटेस्टिंग अवधि सेटिंग्स।

रणनीति के जोखिम

- प्रवृत्ति उत्क्रमण जोखिम: अत्यधिक अस्थिर बाजारों में देरी उत्पन्न हो सकती है।

- समय-सीमा विन्यास जोखिम: विभिन्न बाजारों में अलग-अलग समय-सीमा संयोजनों की आवश्यकता हो सकती है।

- पैरामीटर अनुकूलन जोखिम: अत्यधिक अनुकूलन से ओवरफिटिंग हो सकती है।

- संकेत ओवरलैप जोखिम: दोनों चेन एक साथ सक्रिय होने पर पोजीशन जोखिम बढ़ सकता है।

जोखिम नियंत्रण सुझाव:

- उचित स्टॉप लॉस स्तर निर्धारित करें।

- बाजार की विशेषताओं के अनुसार पैरामीटर समायोजित करें।

- लाइव ट्रेडिंग से पहले पर्याप्त बैकटेस्टिंग करें।

- प्रति ट्रेड पूंजी अनुपात को नियंत्रित करें।

रणनीति अनुकूलन दिशाएँ

- संकेत फ़िल्टरिंग अनुकूलन:

- वॉल्यूम पुष्टिकरण तंत्र जोड़ना।

- अस्थिरता संकेतकों के माध्यम से संकेतों का चयन करना।

- प्रवृत्ति मजबूती पुष्टिकरण जोड़ना।

- जोखिम नियंत्रण अनुकूलन:

- गतिशील स्टॉप लॉस तंत्र विकसित करना।

- पोजीशन प्रबंधन प्रणाली डिज़ाइन करना।

- ड्रॉडाउन नियंत्रण क्षमता जोड़ना।

- समय-सीमा अनुकूलन:

- इष्टतम समय-सीमा संयोजनों का अध्ययन करना।

- अनुकूली समय-सीमा तंत्र विकसित करना।

- बाजार स्थिति पहचान कार्यक्षमता जोड़ना।

सारांश

दोहरी चेन हाइब्रिड मोमेंटम मूविंग एवरेज ट्रेंड ट्रैकिंग ट्रेडिंग सिस्टम, दीर्घकालिक और अल्पकालिक मूविंग एवरेज रणनीतियों को नवीन रूप से संयोजित करके, बाजार के बहुआयामी विश्लेषण और समझ को सक्षम बनाता है। यह प्रणाली लचीली है और विभिन्न बाजार स्थितियों और ट्रेडर शैलियों के अनुसार समायोजित की जा सकती है, जिसमें उच्च व्यावहारिकता है। उचित जोखिम नियंत्रण और निरंतर अनुकूलन के साथ, यह रणनीति वास्तविक ट्रेडिंग में स्थिर लाभ प्राप्त करने में सक्षम हो सकती है। सुझाव है कि ट्रेडर लाइव ट्रेडिंग से पहले पर्याप्त बैकटेस्टिंग और पैरामीटर अनुकूलन करें ताकि सर्वोत्तम ट्रेडिंग परिणाम प्राप्त हो सकें।

- 1