गतिशील व्यापार सिद्धांत का एक्सपोनेंशियल मूविंग एवरेज तथा संचयी वॉल्यूम अवधि क्रॉसओवर रणनीति

अवलोकन

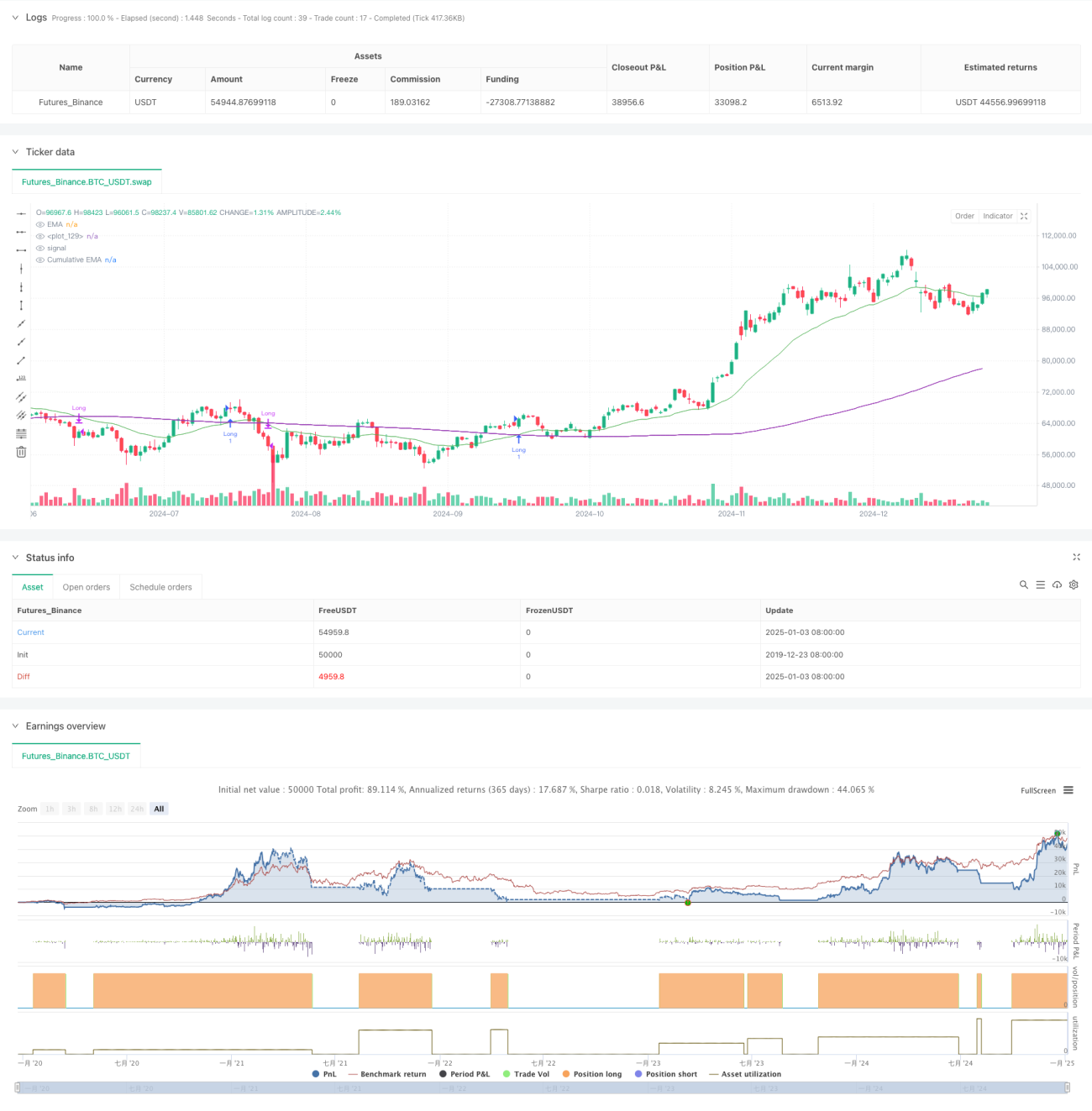

यह रणनीति एक ट्रेडिंग सिस्टम है जो एक्सपोनेंशियल मूविंग एवरेज (EMA) और संचयी वॉल्यूम पीरियड (CVP) को जोड़ती है। यह मूल्य के EMA और संचयी वॉल्यूम भारित मूल्य के क्रॉसओवर का विश्लेषण करके बाजार के रुझान में टर्निंग पॉइंट को कैप्चर करता है। इस रणनीति में एक टाइम फ़िल्टर बनाया गया है, जो ट्रेडिंग घंटों को सीमित कर सकता है, और ट्रेडिंग घंटों के अंत में स्वचालित रूप से पोजीशन बंद करने का समर्थन करता है। यह दो अलग-अलग एग्जिट तरीके प्रदान करता है: रिवर्स क्रॉसओवर एग्जिट और कस्टम CVP एग्जिट, जो इसे उच्च लचीलापन और अनुकूलनशीलता प्रदान करता है।

रणनीति का सिद्धांत

रणनीति का मुख्य तर्क निम्नलिखित प्रमुख गणनाओं पर आधारित है:

- औसत मूल्य (AVWP) की गणना: उच्चतम मूल्य, निम्नतम मूल्य और समापन मूल्य के अंकगणितीय औसत को वॉल्यूम से गुणा करना।

- संचयी वॉल्यूम पीरियड मान की गणना: निर्धारित अवधि में वॉल्यूम भारित मूल्यों को जोड़ना और उन्हें संचयी वॉल्यूम से विभाजित करना।

- क्रमशः समापन मूल्य के EMA और CVP के EMA की गणना।

- जब मूल्य EMA ऊपर की ओर CVP के EMA को पार करता है तो लॉन्ग सिग्नल उत्पन्न होता है; जब मूल्य EMA नीचे की ओर CVP के EMA को पार करता है तो शॉर्ट सिग्नल उत्पन्न होता है।

- एग्जिट सिग्नल या तो एक रिवर्स क्रॉसओवर सिग्नल हो सकता है, या कस्टम CVP अवधि पर आधारित क्रॉसओवर सिग्नल हो सकता है।

रणनीति के लाभ

- सिग्नल प्रणाली मजबूत: मूल्य प्रवृत्ति और वॉल्यूम जानकारी को जोड़कर, यह बाजार की गतिविधियों का अधिक सटीकता से न्याय कर सकता है।

- उच्च अनुकूलनशीलता: EMA अवधि और CVP अवधि को समायोजित करके विभिन्न बाजार स्थितियों के अनुकूल बनाया जा सकता है।

- जोखिम प्रबंधन पूर्ण: बिल्ट-इन टाइम फ़िल्टर अनुपयुक्त ट्रेडिंग घंटों के दौरान संचालन से बचने में मदद करता है।

- एग्जिट तंत्र लचीला: बाजार की विशेषताओं के अनुसार दो अलग-अलग एग्जिट तरीके प्रदान करता है।

- विज़ुअलाइज़ेशन प्रभाव अच्छा: रणनीति सिग्नल मार्कर और ट्रेंड एरिया फिलिंग सहित एक स्पष्ट ग्राफिकल इंटरफ़ेस प्रदान करती है।

रणनीति जोखिम

- अंतराल जोखिम: EMA में स्वाभाविक रूप से कुछ अंतराल होता है, जिससे एंट्री और एग्जिट के समय में थोड़ी देरी हो सकती है।

- अस्थिर बाजार जोखिम: साइडवेज़ या रेंज-बाउंड बाजारों में गलत सिग्नल उत्पन्न हो सकते हैं।

- पैरामीटर संवेदनशीलता: विभिन्न पैरामीटर संयोजनों के परिणामस्वरूप प्रदर्शन में महत्वपूर्ण अंतर हो सकता है।

- तरलता जोखिम: कम तरलता वाले बाजारों में, CVP गणना पर्याप्त सटीक नहीं हो सकती है।

- समय क्षेत्र निर्भरता: रणनीति टाइम फ़िल्टर के लिए न्यूयॉर्क समय का उपयोग करती है, विभिन्न बाजारों के ट्रेडिंग समय में अंतर पर ध्यान देने की आवश्यकता है।

रणनीति अनुकूलन दिशाएँ

- अस्थिरता फ़िल्टर शामिल करना: बाजार की अस्थिरता के अनुसार रणनीति मापदंडों को समायोजित करके अनुकूलनशीलता में सुधार किया जा सकता है।

- टाइम फ़िल्टर को अनुकूलित करना: ट्रेडिंग घंटों को अधिक सटीक रूप से नियंत्रित करने के लिए कई टाइम विंडो जोड़े जा सकते हैं।

- वॉल्यूम गुणवत्ता मूल्यांकन बढ़ाना: निम्न-गुणवत्ता वाले वॉल्यूम सिग्नल को फ़िल्टर करने के लिए वॉल्यूम विश्लेषण संकेतक शामिल करना।

- गतिशील पैरामीटर समायोजन: बाजार की स्थितियों के आधार पर EMA और CVP अवधियों को स्वचालित रूप से समायोजित करने के लिए एक अनुकूली पैरामीटर सिस्टम विकसित करना।

- बाजार भावना संकेतक जोड़ना: ट्रेडिंग सिग्नल की पुष्टि करने के लिए अन्य तकनीकी संकेतकों के साथ संयोजन।

सारांश

यह एक संरचित, तार्किक मात्रात्मक ट्रेडिंग रणनीति है। EMA और CVP की ताकतों को मिलाकर, यह एक ट्रेडिंग सिस्टम बनाता है जो ट्रेंड को कैप्चर करता है और साथ ही जोखिम प्रबंधन पर भी ध्यान केंद्रित करता है। रणनीति उच्च स्तर की अनुकूलन क्षमता प्रदान करती है, जो इसे विभिन्न बाजार वातावरणों में उपयोग के लिए उपयुक्त बनाती है। अनुकूलन सुझावों के कार्यान्वयन के साथ, रणनीति के प्रदर्शन में और सुधार की गुंजाइश है।

- 1