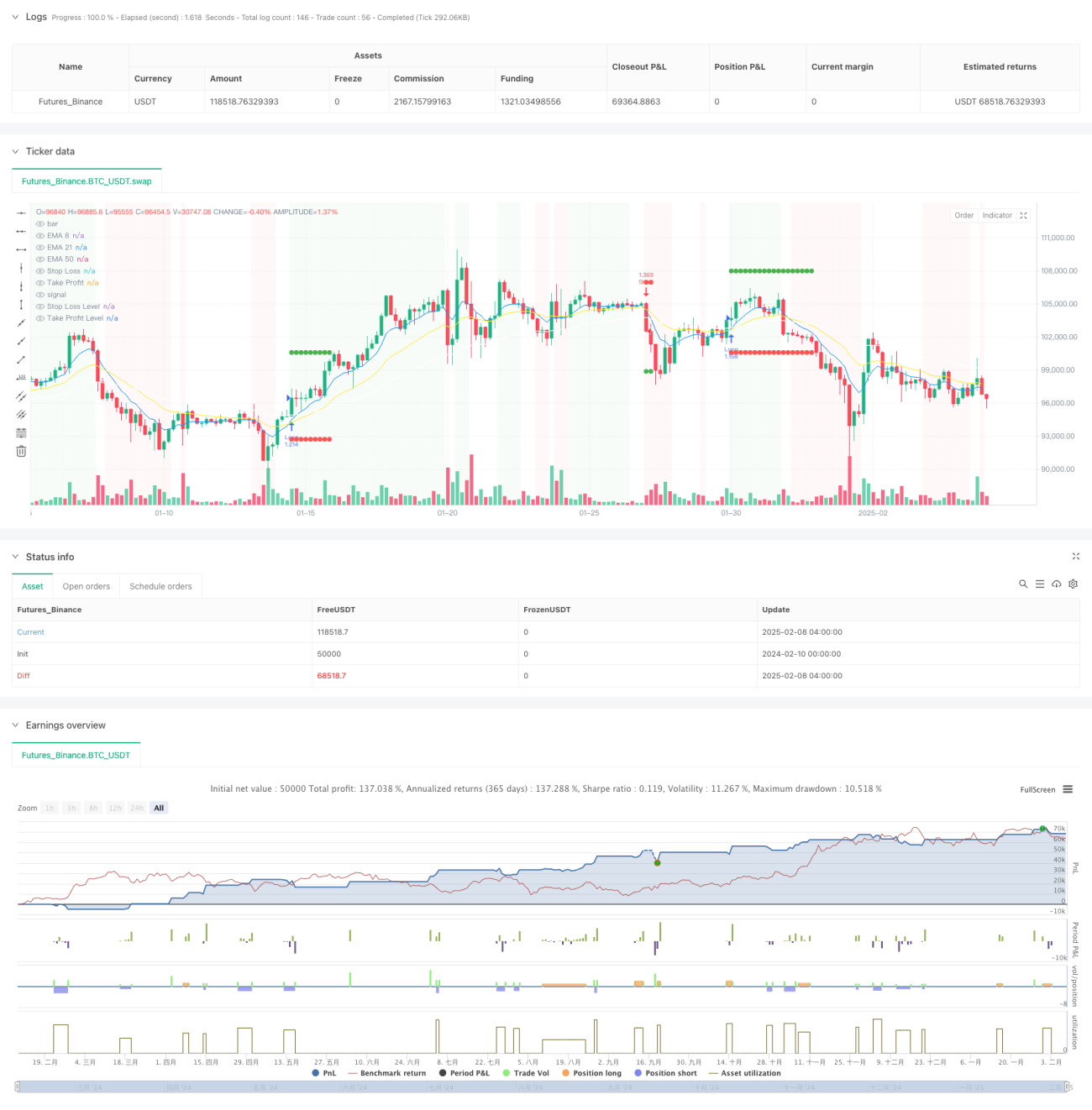

अवलोकन

यह एक बहु-तकनीकी संकेतक और जोखिम प्रबंधन पर आधारित प्रवृत्ति अनुसरण रणनीति है। यह रणनीति बाजार की प्रवृत्ति की पहचान करने के लिए मूविंग एवरेज, सापेक्ष शक्ति सूचकांक (RSI), दिशात्मक गति सूचकांक (DMI) जैसे कई तकनीकी संकेतकों का संयोजन करती है, और गतिशील स्टॉप लॉस, स्थिति प्रबंधन और मासिक अधिकतम ड्रॉडाउन सीमा जैसे जोखिम नियंत्रण उपायों के माध्यम से पूंजी की सुरक्षा करती है। रणनीति का मूल बहु-आयामी तकनीकी संकेतकों के माध्यम से प्रवृत्ति की वैधता की पुष्टि करना और साथ ही जोखिम जोखिम को सख्ती से नियंत्रित करना है।

रणनीति सिद्धांत

रणनीति बहु-स्तरीय प्रवृत्ति पुष्टि तंत्र अपनाती है:

- 8/21/50 अवधि के एक्सपोनेंशियल मूविंग एवरेज (EMA) के माध्यम से प्रवृत्ति की दिशा का निर्धारण

- मूल्य चैनल की मध्य रेखा को प्रवृत्ति फिल्टर के रूप में उपयोग करना

- RSI मूविंग एवरेज (5 अवधि) के 35-65 सीमा में चलने के साथ झूठे ब्रेकआउट को फ़िल्टर करना

- DMI संकेतक (14 अवधि) के माध्यम से प्रवृत्ति की ताकत की पुष्टि करना

- गति संकेतक (8 अवधि) और वॉल्यूम में वृद्धि का उपयोग करके प्रवृत्ति की निरंतरता को सत्यापित करना

- ATR-आधारित गतिशील स्टॉप लॉस का उपयोग करके जोखिम को नियंत्रित करना

- निश्चित जोखिम मॉडल का स्थिति प्रबंधन लागू करना, प्रति ट्रेड जोखिम राशि प्रारंभिक पूंजी का 5% है

- अत्यधिक नुकसान से बचने के लिए 10% की मासिक अधिकतम ड्रॉडाउन सीमा निर्धारित करना

रणनीति के लाभ

- एकाधिक तकनीकी संकेतकों का क्रॉस-सत्यापन, प्रवृत्ति निर्धारण की सटीकता में सुधार

- गतिशील स्टॉप लॉस तंत्र प्रति ट्रेड जोखिम को प्रभावी ढंग से नियंत्रित करता है

- निश्चित जोखिम का स्थिति प्रबंधन तरीका पूंजी उपयोग को अधिक उचित बनाता है

- मासिक अधिकतम ड्रॉडाउन सीमा प्रणालीगत जोखिम सुरक्षा प्रदान करती है

- वॉल्यूम संकेतक के साथ संयोजन, प्रवृत्ति पुष्टि की विश्वसनीयता को बढ़ाता है

- 2:1 का लाभ-हानि अनुपात सेटिंग दीर्घकालिक लाभप्रदता में सुधार करता है

रणनीति जोखिम

- एकाधिक संकेतकों के उपयोग से संकेत विलंब हो सकता है

- सीमा-बद्ध बाजार में बार-बार झूठे संकेत उत्पन्न हो सकते हैं

- निश्चित जोखिम मॉडल अस्थिरता में तीव्र परिवर्तन के समय पर्याप्त लचीला नहीं हो सकता है

- मासिक ड्रॉडाउन सीमा महत्वपूर्ण ट्रेडिंग अवसरों को खोने का कारण बन सकती है

- प्रवृत्ति उलटफेर के समय बड़ा ड्रॉडाउन सहना पड़ सकता है

रणनीति अनुकूलन दिशा

- विभिन्न बाजार वातावरणों के अनुकूल होने के लिए अनुकूली संकेतक पैरामीटर पेश करना

- बाजार की अस्थिरता में बदलाव को ध्यान में रखते हुए अधिक लचीली स्थिति प्रबंधन योजना विकसित करना

- प्रवृत्ति की ताकत का मात्रात्मक मूल्यांकन जोड़ना, प्रवेश समय को अनुकूलित करना

- अधिक बुद्धिमान मासिक जोखिम सीमा तंत्र डिज़ाइन करना

- बाजार वातावरण पहचान मॉड्यूल जोड़ना, विभिन्न बाजार स्थितियों में रणनीति पैरामीटर समायोजित करना

सारांश

यह रणनीति बहु-आयामी तकनीकी संकेतकों के व्यापक उपयोग के माध्यम से एक अपेक्षाकृत पूर्ण प्रवृत्ति अनुसरण ट्रेडिंग सिस्टम स्थापित करती है। रणनीति का लाभ इसके व्यापक जोखिम प्रबंधन ढांचे में निहित है, जिसमें गतिशील स्टॉप लॉस, स्थिति प्रबंधन और ड्रॉडाउन नियंत्रण शामिल हैं। हालांकि कुछ विलंब जोखिम है, अनुकूलन और सुधार के माध्यम से, रणनीति विभिन्न बाजार वातावरणों में स्थिर प्रदर्शन बनाए रखने की उम्मीद है। कुंजी रणनीति के मुख्य तर्क को बनाए रखते हुए बाजार वातावरण के अनुकूल इसकी क्षमता को बढ़ाना है।

/*backtest

start: 2024-02-10 00:00:00

end: 2025-02-08 08:00:00

period: 4h

basePeriod: 4h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("High Win-Rate Crypto Strategy with Drawdown Limit", overlay=true, initial_capital=10000, default_qty_type=strategy.fixed, process_orders_on_close=true)

// Moving Averages- 1