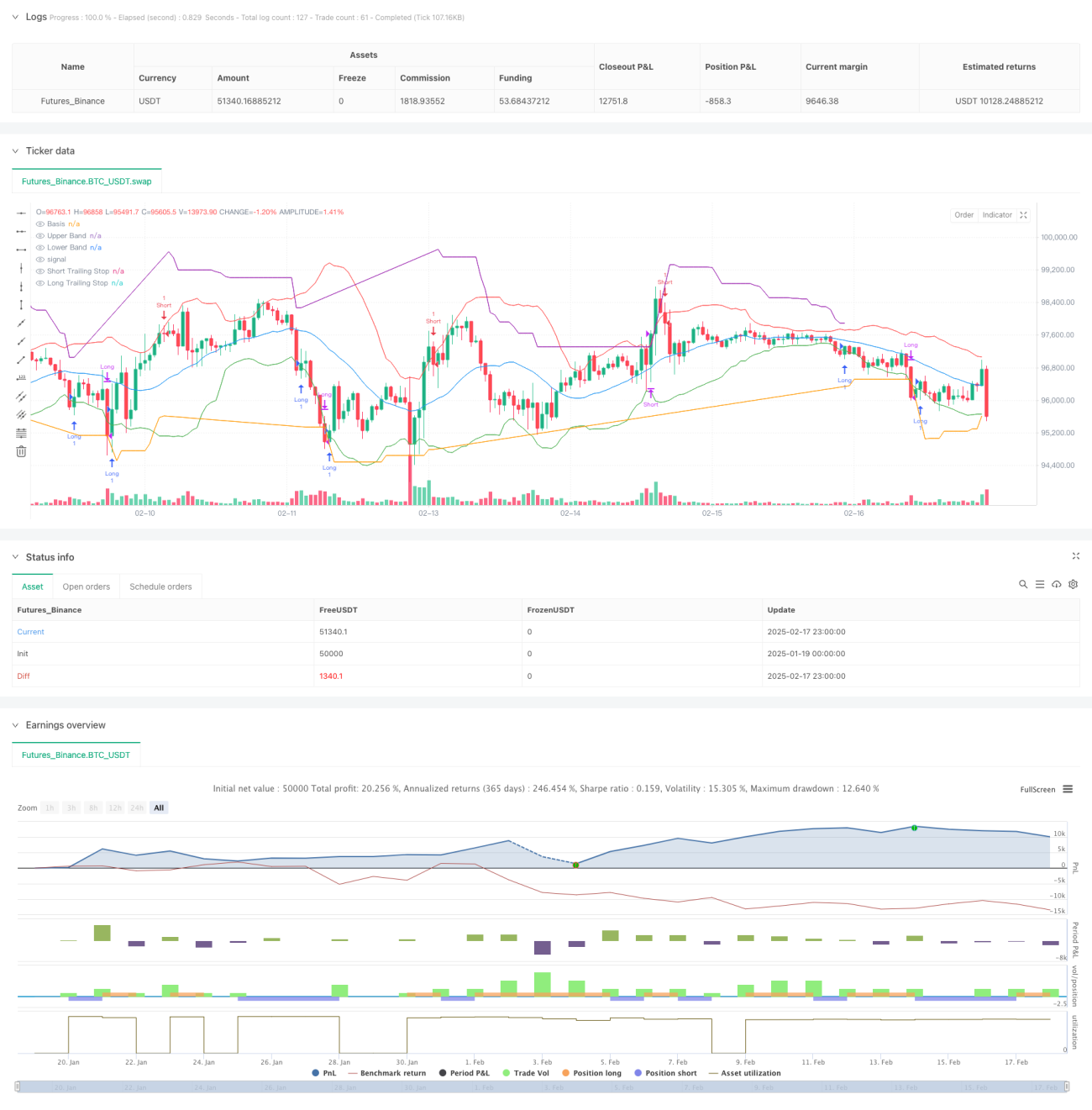

अवलोकन

यह रणनीति एक अनुकूली ट्रेडिंग सिस्टम है जो बॉलिंगर बैंड (Bollinger Bands) और ATR ट्रेलिंग स्टॉप को जोड़ती है। रणनीति बॉलिंगर बैंड के ऊपरी और निचले बैंड के टूटने के माध्यम से प्रवेश संकेत निर्धारित करती है, साथ ही जोखिम प्रबंधन और निकास समय निर्धारित करने के लिए ATR-आधारित गतिशील ट्रेलिंग स्टॉप का उपयोग करती है। यह रणनीति बाजार में स्पष्ट प्रवृत्ति होने पर प्रवृत्ति के अवसरों को पकड़ने में सक्षम है, साथ ही साइडवे बाजार में सुरक्षा प्रदान करती है।

रणनीति का सिद्धांत

रणनीति का मुख्य तर्क दो मुख्य भागों से बना है:

- प्रवेश संकेत प्रणाली: मुख्य संकेतक के रूप में बॉलिंगर बैंड (BB) का उपयोग करती है। जब कीमत निचले बैंड को तोड़ती है तो लंबा (लॉन्ग) सिग्नल उत्पन्न होता है, और जब ऊपरी बैंड को तोड़ती है तो छोटा (शॉर्ट) सिग्नल उत्पन्न होता है। बॉलिंगर बैंड के पैरामीटर मध्य बैंड के रूप में 20-अवधि चलती औसत और मानक विचलन गुणक 2.0 के रूप में सेट किए गए हैं।

- स्टॉप लॉस प्रबंधन प्रणाली: 14-अवधि ATR को अस्थिरता संदर्भ के रूप में उपयोग करता है, जिसमें गुणक 3.0 है। लंबी पोजीशन रखते समय, स्टॉप लॉस लाइन कीमत बढ़ने पर ऊपर की ओर बढ़ती है, और इसके विपरीत। यह गतिशील स्टॉप तंत्र लाभ को स्वाभाविक रूप से बढ़ने देता है, साथ ही प्रभावी ढंग से गिरावट को नियंत्रित करता है।

रणनीति के लाभ

- उच्च अनुकूलनशीलता: बॉलिंगर बैंड और ATR दोनों बाजार की वास्तविक अस्थिरता के आधार पर गणना किए गए संकेतक हैं, जो स्वचालित रूप से विभिन्न बाजार स्थितियों के अनुकूल हो सकते हैं।

- मजबूत जोखिम नियंत्रण: ATR गतिशील स्टॉप के माध्यम से, न केवल समय पर स्टॉप लॉस लगाया जा सकता है, बल्कि मजबूत प्रवृत्ति से जल्दी बाहर भी नहीं निकलना पड़ता।

- स्पष्ट संकेत: प्रवेश और निकास संकेत स्पष्ट मूल्य टूटने पर आधारित हैं, जिनमें व्यक्तिपरक निर्णय की आवश्यकता नहीं है।

- उच्च विज़ुअलाइज़ेशन: रणनीति चार्ट पर सभी सिग्नल बिंदुओं को स्पष्ट रूप से चिह्नित करती है, जिससे विश्लेषण और अनुकूलन आसान होता है।

रणनीति के जोखिम

- साइडवे बाजार जोखिम: स्पष्ट प्रवृत्ति के बिना बाजार में, बार-बार झूठे ब्रेकआउट संकेत उत्पन्न हो सकते हैं, जिससे लगातार स्टॉप लॉस लग सकता है।

- स्लिपेज जोखिम: उच्च बाजार अस्थिरता के दौरान, वास्तविक निष्पादन मूल्य सैद्धांतिक संकेत मूल्य से बड़े अंतर पर हो सकता है।

- पैरामीटर संवेदनशीलता: रणनीति का प्रभाव बॉलिंगर बैंड और ATR के पैरामीटर सेटिंग्स के प्रति संवेदनशील होता है, और विभिन्न बाजार स्थितियों के लिए अनुकूलन की आवश्यकता होती है।

रणनीति के अनुकूलन की दिशाएँ

- ट्रेंड फ़िल्टर जोड़ना: अतिरिक्त प्रवृत्ति निर्धारण संकेतक जोड़े जा सकते हैं, केवल स्पष्ट प्रवृत्ति होने पर ही पोजीशन खोलें, जिससे साइडवे बाजार में झूठे संकेत कम हों।

- स्टॉप लॉस पैरामीटर को अनुकूलित करना: विभिन्न बाजार स्थितियों के अनुसार ATR गुणक को गतिशील रूप से समायोजित किया जा सकता है, उच्च अस्थिरता पर ढीले स्टॉप लॉस का उपयोग करें।

- पोजीशन प्रबंधन शामिल करना: ATR के आधार पर गतिशील पोजीशन सिस्टम डिज़ाइन किया जा सकता है, जो विभिन्न अस्थिरता स्थितियों में स्वचालित रूप से ओपनिंग आकार को समायोजित करे।

- समय फ़िल्टर जोड़ना: महत्वपूर्ण आर्थिक डेटा जारी होने जैसे उच्च अस्थिरता अवधियों के दौरान ट्रेडिंग से बचा जा सकता है।

सारांश

यह रणनीति बॉलिंगर बैंड और ATR ट्रेलिंग स्टॉप को जोड़कर एक ट्रेडिंग सिस्टम बनाती है जिसमें प्रवृत्ति को पकड़ने और जोखिम नियंत्रण दोनों की क्षमता होती है। रणनीति की अनुकूली प्रकृति इसे विभिन्न बाजार स्थितियों में स्थिर बनाए रखती है, जबकि स्पष्ट संकेत प्रणाली वस्तुनिष्ठ ट्रेडिंग आधार प्रदान करती है। सुझाए गए अनुकूलन दिशाओं के माध्यम से, रणनीति में और सुधार की गुंजाइश है। वास्तविक उपयोग में, निवेशकों को अपनी जोखिम सहनशीलता और ट्रेडिंग उत्पाद की विशेषताओं के अनुसार पैरामीटर को लक्षित रूप से समायोजित करने की सलाह दी जाती है।

- 1