बहु-संकेतक प्रवृत्ति गति ATR लक्ष्य मूल्य व्यापार रणनीति

अवलोकन

यह रणनीति एक बहु-तकनीकी संकेतक आधारित ट्रेंड फॉलोइंग और मोमेंटम ट्रेडिंग सिस्टम है। यह मुख्य रूप से औसत दिशात्मक सूचकांक (ADX), सापेक्ष शक्ति सूचकांक (RSI) और ट्रू रेंज (ATR) को मिलाकर संभावित लॉन्ग (खरीद) के अवसरों की पहचान करता है, और गतिशील लाभ और स्टॉप-लॉस स्तर निर्धारित करने के लिए ATR का उपयोग करता है। यह रणनीति विशेष रूप से 1 मिनट की समय सीमा के ऑप्शन ट्रेडिंग के लिए उपयुक्त है, जो सख्त प्रवेश शर्तों और जोखिम प्रबंधन के माध्यम से ट्रेडिंग की सफलता दर को बढ़ाती है।

रणनीति का सिद्धांत

रणनीति के मुख्य तर्क में निम्नलिखित प्रमुख घटक शामिल हैं:

- प्रवृत्ति पुष्टि: ADX > 18 और +DI > -DI का उपयोग करके बाजार में बढ़ती प्रवृत्ति की पुष्टि की जाती है।

- मोमेंटम सत्यापन: RSI के 60 से ऊपर पहुंचने और इसके 20-अवधि के मूविंग एवरेज से ऊपर रहने की आवश्यकता होती है, जिससे मूल्य गति की पुष्टि होती है।

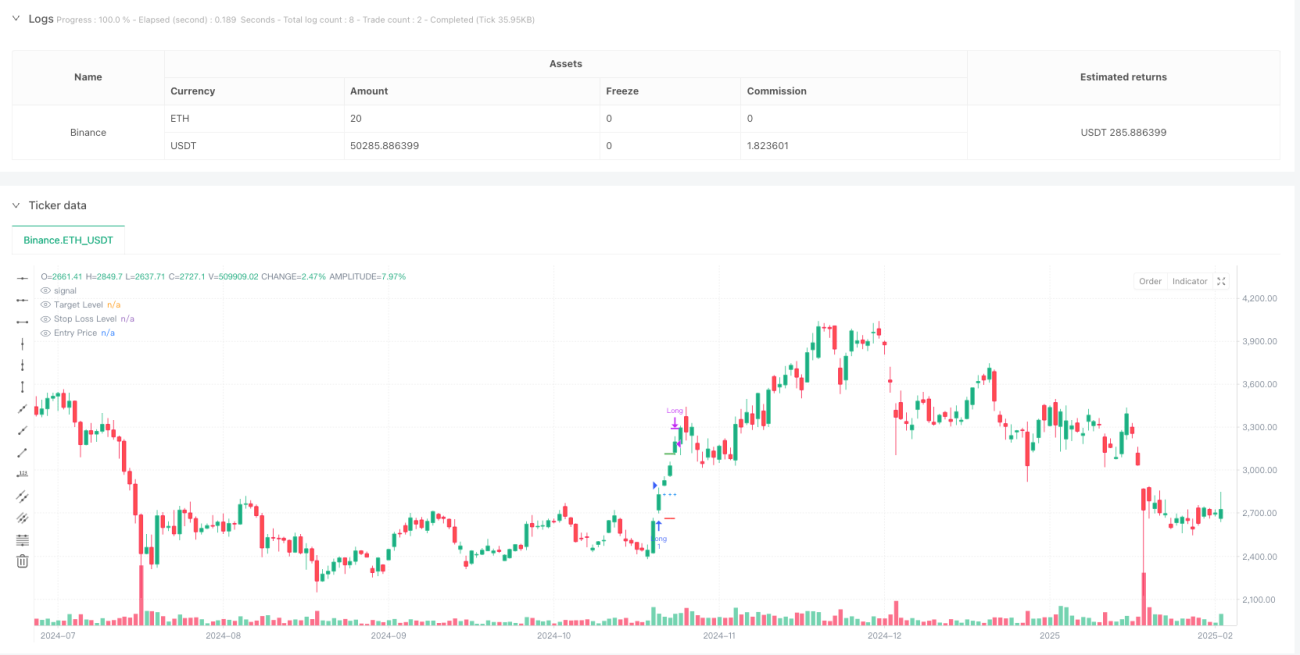

- प्रवेश का समय: जब प्रवृत्ति और मोमेंटम की शर्तें एक साथ पूरी होती हैं, तो सिस्टम वर्तमान बंद कीमत पर लॉन्ग (खरीद) पोजीशन बनाता है।

- लक्ष्य प्रबंधन: प्रवेश के समय ATR मान के आधार पर गतिशील लाभ लक्ष्य (2.5 गुना ATR) और स्टॉप-लॉस (1.5 गुना ATR) निर्धारित किए जाते हैं।

रणनीति के लाभ

- बहु-आयामी पुष्टि: प्रवृत्ति और मोमेंटम संकेतकों को जोड़कर अधिक विश्वसनीय ट्रेडिंग संकेत प्रदान करता है।

- गतिशील जोखिम प्रबंधन: ATR का उपयोग करके स्टॉप-लॉस और टेक-प्रॉफिट स्तरों को गतिशील रूप से समायोजित करता है, जो बाजार की अस्थिरता के अनुकूल होता है।

- स्पष्ट ट्रेडिंग नियम: प्रवेश और निकास की शर्तें स्पष्ट हैं, जिससे व्यक्तिपरक निर्णय का हस्तक्षेप कम होता है।

- अनुकूलनशीलता: रणनीति के मापदंडों को विभिन्न बाजार स्थितियों और ट्रेडिंग उपकरणों के अनुसार अनुकूलित किया जा सकता है।

रणनीति के जोखिम

- झूठी ब्रेकआउट का जोखिम: RSI का 60 से ऊपर जाना झूठा संकेत हो सकता है, जिसे अन्य संकेतकों से सत्यापित करने की आवश्यकता है।

- स्लिपेज का प्रभाव: 1 मिनट के तेजी से चलने वाले बाजार में बड़े स्लिपेज का जोखिम हो सकता है।

- बाजार के माहौल पर निर्भरता: रणनीति स्पष्ट प्रवृत्ति वाले बाजार में बेहतर प्रदर्शन करती है, जबकि बिना दिशा वाले बाजार में बार-बार स्टॉप-लॉस ट्रिगर हो सकता है।

- पैरामीटर संवेदनशीलता: कई संकेतक मापदंडों की सेटिंग में संतुलन की आवश्यकता होती है; गलत पैरामीटर संयोजन रणनीति के प्रदर्शन को प्रभावित कर सकते हैं।

रणनीति अनुकूलन की दिशाएँ

- प्रवेश अनुकूलन: संकेत की विश्वसनीयता बढ़ाने के लिए वॉल्यूम पुष्टि तंत्र जोड़ा जा सकता है।

- पोजीशन प्रबंधन: बाजार की अस्थिरता के अनुसार पोजीशन के आकार को समायोजित करने के लिए गतिशील पोजीशन प्रबंधन प्रणाली शामिल की जा सकती है।

- निकास तंत्र: लाभ को बेहतर ढंग से सुरक्षित करने के लिए ट्रेलिंग स्टॉप-लॉस फीचर जोड़ा जा सकता है।

- समय फ़िल्टर: अत्यधिक अस्थिरता या तरलता की कमी वाले समय से बचने के लिए ट्रेडिंग समय विंडो फ़िल्टर जोड़ा जा सकता है।

सारांश

यह रणनीति कई तकनीकी संकेतकों के व्यापक उपयोग के माध्यम से एक पूर्ण ट्रेडिंग सिस्टम का निर्माण करती है। इसका लाभ प्रवृत्ति और मोमेंटम विश्लेषण के संयोजन तथा गतिशील जोखिम प्रबंधन पद्धति में निहित है। हालांकि कुछ जोखिम हैं, उचित पैरामीटर अनुकूलन और जोखिम नियंत्रण उपायों के साथ, यह वास्तविक ट्रेडिंग में स्थिर प्रदर्शन प्राप्त कर सकता है। सुझाव दिया जाता है कि व्यापारी वास्तविक खाते में उपयोग करने से पहले रणनीति का पर्याप्त बैकटेस्ट और पैरामीटर अनुकूलन करें, और विशिष्ट ट्रेडिंग उपकरणों की विशेषताओं के अनुसार उचित समायोजन करें।

- 1