ATR गतिशील ट्रेलिंग स्टॉप-लॉस प्रवृत्ति अनुसरण ट्रेडिंग सिस्टम

सिंहावलोकन

यह रणनीति एटीआर (औसत सत्य रेंज) पर आधारित एक गतिशील ट्रेलिंग स्टॉप ट्रेंड फॉलोइंग सिस्टम है। यह ट्रेंड फिल्टर के रूप में ईएमए मूविंग एवरेज का उपयोग करती है और संवेदनशीलता पैरामीटर और एटीआर अवधि को समायोजित करके सिग्नल उत्पादन को नियंत्रित करती है। सिस्टम न केवल लॉन्ग ट्रेडिंग बल्कि शॉर्ट ट्रेडिंग का भी समर्थन करता है और इसमें एक संपूर्ण लाभ प्रबंधन तंत्र है।

रणनीति का सिद्धांत

- एटीआर संकेतक का उपयोग करके मूल्य में उतार-चढ़ाव की सीमा की गणना करना और निर्धारित संवेदनशीलता गुणांक (की वैल्यू) के अनुसार ट्रेलिंग स्टॉप दूरी निर्धारित करना।

- ईएमए मूविंग एवरेज के माध्यम से बाजार की प्रवृत्ति की दिशा का निर्धारण करना, केवल तभी लॉन्ग पोजीशन खोलना जब कीमत मूविंग एवरेज के ऊपर हो, और केवल तभी शॉर्ट पोजीशन खोलना जब कीमत मूविंग एवरेज के नीचे हो।

- जब कीमत ट्रेलिंग स्टॉप लाइन को तोड़ती है और प्रवृत्ति की दिशा के अनुरूप होती है, तब ट्रेडिंग सिग्नल ट्रिगर होता है।

- सिस्टम पोजीशन को प्रबंधित करने के लिए चरणबद्ध लाभ-अर्जन विधि का उपयोग करता है:

- 20%-50% लाभ होने पर, स्टॉप लॉस को लागत मूल्य तक बढ़ाकर ब्रेक-ईवन सुनिश्चित करना।

- 50%-80% लाभ होने पर, आंशिक लाभ बुक करना और स्टॉप लॉस को कड़ा करना।

- 80%-100% लाभ होने पर, लाभ की रक्षा के लिए स्टॉप लॉस को और कड़ा करना।

- 100% से अधिक लाभ होने पर, सभी पोजीशन बंद करके लाभ बुक करना।

रणनीति के लाभ

- गतिशील ट्रेलिंग स्टॉप प्रवृत्ति का प्रभावी ढंग से पालन कर सकता है, लाभ की रक्षा करते हुए समय से पहले बाहर नहीं निकलता।

- ईएमए ट्रेंड फिल्टर झूठे ब्रेकआउट से होने वाले जोखिम को प्रभावी ढंग से कम करता है।

- चरणबद्ध लाभ-अर्जन तंत्र लाभ की प्राप्ति सुनिश्चित करता है, साथ ही प्रवृत्ति को पूरी तरह विकसित होने का स्थान देता है।

- लॉन्ग और शॉर्ट दोनों दिशाओं में ट्रेडिंग का समर्थन करता है, जिससे बाजार के अवसरों का पूरा लाभ उठाया जा सकता है।

- पैरामीटर अत्यधिक समायोज्य हैं, जो विभिन्न बाजार स्थितियों के अनुकूल होते हैं।

रणनीति के जोखिम

- साइडवेज़ बाजार में बार-बार ट्रेडिंग से नुकसान हो सकता है।

- प्रवृत्ति के प्रारंभिक उलटफेर में बड़ी ड्रॉडाउन हो सकती है।

- गलत पैरामीटर सेटिंग रणनीति के प्रदर्शन को प्रभावित कर सकती है।

जोखिम नियंत्रण सुझाव:

- स्पष्ट प्रवृत्ति वाले बाजार में उपयोग करने की सलाह दी जाती है।

- पैरामीटर सावधानी से चुनें, बैकटेस्टिंग के माध्यम से अनुकूलन किया जा सकता है।

- अधिकतम ड्रॉडाउन सीमा निर्धारित करें।

- बाजार पर्यावरण फिल्टरिंग शर्तों को जोड़ने पर विचार करें।

रणनीति अनुकूलन की दिशाएँ

- बाजार पर्यावरण पहचान तंत्र जोड़ना, विभिन्न बाजार स्थितियों में विभिन्न पैरामीटर का उपयोग करना।

- सिग्नल विश्वसनीयता बढ़ाने के लिए वॉल्यूम जैसे सहायक संकेतक शामिल करना।

- लाभ प्रबंधन तंत्र को अनुकूलित करना, अस्थिरता के अनुसार लाभ लक्ष्यों को गतिशील रूप से समायोजित करना।

- प्रतिकूल समय में ट्रेडिंग से बचने के लिए समय फिल्टर जोड़ना।

- अत्यधिक अस्थिरता में ट्रेडिंग आवृत्ति कम करने के लिए अस्थिरता फिल्टर जोड़ने पर विचार करना।

निष्कर्ष

यह एक संरचनात्मक रूप से पूर्ण और तार्किक रूप से स्पष्ट ट्रेंड फॉलोइंग सिस्टम है। एटीआर गतिशील ट्रैकिंग और ईएमए ट्रेंड फिल्टर के संयोजन के माध्यम से, यह प्रवृत्ति को पकड़ने के साथ-साथ जोखिम को अच्छी तरह से नियंत्रित करता है। चरणबद्ध लाभ-अर्जन तंत्र का डिज़ाइन भी परिपक्व ट्रेडिंग सोच को दर्शाता है। रणनीति में मजबूत व्यावहारिकता और विस्तारशीलता है, और निरंतर अनुकूलन और सुधार के माध्यम से बेहतर ट्रेडिंग परिणाम प्राप्त करने की उम्मीद है।

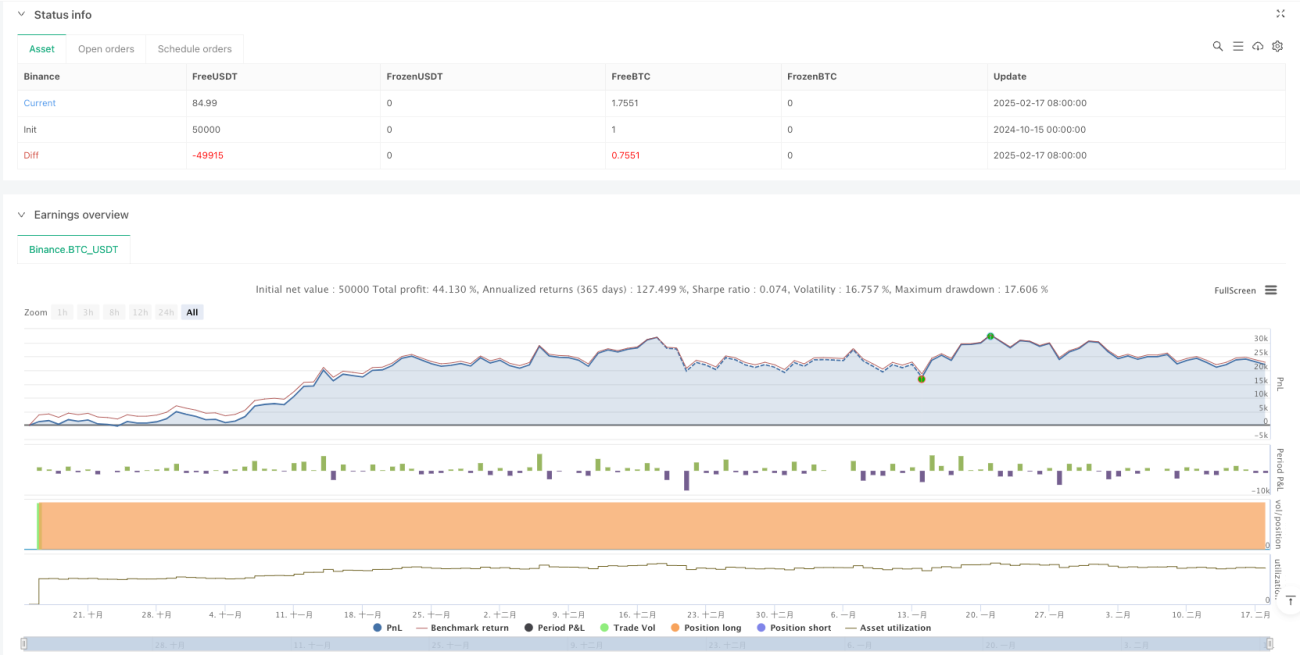

/*backtest

start: 2024-10-15 00:00:00

end: 2025-02-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Enhanced UT Bot with Long & Short Trades", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// Input Parameters- 1